Вам также может понравиться

- University of Cambridge International Examinations General Certificate of Education Ordinary LevelДокумент12 страницUniversity of Cambridge International Examinations General Certificate of Education Ordinary LevelAbdul Fayad MajidОценок пока нет

- University of Cambridge International Examinations General Certificate of Education Ordinary LevelДокумент12 страницUniversity of Cambridge International Examinations General Certificate of Education Ordinary LevelAbdul Fayad MajidОценок пока нет

- 0455 m18 Ms 12 PDFДокумент2 страницы0455 m18 Ms 12 PDFNiОценок пока нет

- 0455 m17 Ms 12Документ3 страницы0455 m17 Ms 12eco2dayОценок пока нет

- 0625 w14 Ms 11Документ2 страницы0625 w14 Ms 11Haider AliОценок пока нет

- Economics: Cambridge International General Certificate of Secondary EducationДокумент1 страницаEconomics: Cambridge International General Certificate of Secondary EducationDhoni KhanОценок пока нет

- 0455 w14 Ms 23 PDFДокумент16 страниц0455 w14 Ms 23 PDFDhoni KhanОценок пока нет

- Grade Thresholds - November 2018: Cambridge O Level Second Language Urdu (3248)Документ1 страницаGrade Thresholds - November 2018: Cambridge O Level Second Language Urdu (3248)Uzair KhanОценок пока нет

- 0455 m18 Ms 12 PDFДокумент2 страницы0455 m18 Ms 12 PDFNiОценок пока нет

- 0455 m18 Ms 12 PDFДокумент2 страницы0455 m18 Ms 12 PDFNiОценок пока нет

- 0455 m18 Ms 12 PDFДокумент2 страницы0455 m18 Ms 12 PDFNiОценок пока нет

- 0455 m18 Ms 12 PDFДокумент2 страницы0455 m18 Ms 12 PDFNiОценок пока нет

- Cambridge IGCSE Economics March 2016 Multiple Choice Mark SchemeДокумент2 страницыCambridge IGCSE Economics March 2016 Multiple Choice Mark SchemeBalrajSinghBatthОценок пока нет

- Economics: Cambridge International General Certificate of Secondary EducationДокумент1 страницаEconomics: Cambridge International General Certificate of Secondary EducationDhoni KhanОценок пока нет

- Economics: University of Cambridge International Examinations International General Certificate of Secondary EducationДокумент4 страницыEconomics: University of Cambridge International Examinations International General Certificate of Secondary EducationDhoni KhanОценок пока нет

- EconomicsДокумент7 страницEconomicsDhoni KhanОценок пока нет

- MARK SCHEME For The May/June 2006 Question Paper: University of Cambridge International ExaminationsДокумент2 страницыMARK SCHEME For The May/June 2006 Question Paper: University of Cambridge International ExaminationsDhoni KhanОценок пока нет

- Cambridge IGCSE Economics March 2016 Multiple Choice Mark SchemeДокумент2 страницыCambridge IGCSE Economics March 2016 Multiple Choice Mark SchemeBalrajSinghBatthОценок пока нет

- Economics: University of Cambridge International Examinations International General Certificate of Secondary EducationДокумент2 страницыEconomics: University of Cambridge International Examinations International General Certificate of Secondary EducationDhoni KhanОценок пока нет

- Members of The NSU Syndicate-18062019Документ1 страницаMembers of The NSU Syndicate-18062019Dhoni KhanОценок пока нет

- 1906 Ial Grade Boundaries v3Документ10 страниц1906 Ial Grade Boundaries v3Dhoni KhanОценок пока нет

- Edexcel IGCSE Business Studies Student Book and ActiveBook CDДокумент1 страницаEdexcel IGCSE Business Studies Student Book and ActiveBook CDDhoni KhanОценок пока нет

- HypothesisДокумент1 страницаHypothesisDhoni KhanОценок пока нет

- 2281 s06 QP 2Документ4 страницы2281 s06 QP 2Mohammad HussainОценок пока нет

- Why CVs Are RejectedДокумент1 страницаWhy CVs Are RejectedDhoni KhanОценок пока нет

- Pearson Edexcel 2018 Examination Start TimesДокумент3 страницыPearson Edexcel 2018 Examination Start TimesDhoni KhanОценок пока нет

- Step Guide For IGCSE, O Level and A Level Exam Registration BangladeshДокумент5 страницStep Guide For IGCSE, O Level and A Level Exam Registration BangladeshDhoni KhanОценок пока нет

- Problem 3Документ3 страницыProblem 3Dhoni KhanОценок пока нет

- Session 2-2Документ10 страницSession 2-2Dhoni KhanОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- MEFA 5 UnitДокумент30 страницMEFA 5 UnitSuhasОценок пока нет

- Preview PDFДокумент5 страницPreview PDFGabriel TalosОценок пока нет

- Memorandum of Law in Support of 1099oidДокумент19 страницMemorandum of Law in Support of 1099oidkingtbrown50100% (2)

- Anatomy of A Net Worth AssessmentДокумент36 страницAnatomy of A Net Worth AssessmentSpencer100% (1)

- 2020 Vision11Документ98 страниц2020 Vision11derektennant100% (2)

- Money and BankingДокумент8 страницMoney and BankingMuskan RahimОценок пока нет

- CHP 13 Testbank 2Документ15 страницCHP 13 Testbank 2judyОценок пока нет

- Type of Existing Policy:: Surrendering Company InformationДокумент1 страницаType of Existing Policy:: Surrendering Company InformationEjiroОценок пока нет

- Integ02 A QuestionsДокумент20 страницInteg02 A QuestionsRonald CorunoОценок пока нет

- Bailment and Duties of Bailee and BailerДокумент7 страницBailment and Duties of Bailee and BailerHaider TajОценок пока нет

- Sneha Loan ProjectДокумент63 страницыSneha Loan ProjectRahul GhosaleОценок пока нет

- Request For Taxpayer Identification Number and CertificationДокумент6 страницRequest For Taxpayer Identification Number and CertificationTaj R.100% (1)

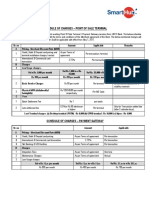

- SCHEDULE - OF - CHARGES - Combined - PoS - PGMarch - 14 PDFДокумент2 страницыSCHEDULE - OF - CHARGES - Combined - PoS - PGMarch - 14 PDFnits_chawlaОценок пока нет

- Credit TransactionsДокумент84 страницыCredit TransactionsMaricris100% (1)

- Delphi's Account of Its Platinum TransactionДокумент26 страницDelphi's Account of Its Platinum TransactionDealBook100% (1)

- Unsecured Loan AgreementДокумент2 страницыUnsecured Loan AgreementSavoir PenОценок пока нет

- Capital Code Consultant Private Limited decoded business valueДокумент2 страницыCapital Code Consultant Private Limited decoded business valueKiran MaliОценок пока нет

- Note 08Документ6 страницNote 08Tharaka IndunilОценок пока нет

- Overseas Project Management RatingДокумент15 страницOverseas Project Management RatingKashish KashyapОценок пока нет

- The Appellant in His Own Behalf. Franco and Reinoso For AppelleeДокумент1 страницаThe Appellant in His Own Behalf. Franco and Reinoso For AppelleeCarlyn Belle de GuzmanОценок пока нет

- Project On NBFCДокумент67 страницProject On NBFCkumar12925359Оценок пока нет

- Sinking Fund and Amortization Review QuestionsДокумент12 страницSinking Fund and Amortization Review QuestionsLeonell Musca ManaloОценок пока нет

- PCI Leasing v. Trojan Metal Industries: Financial Leasing Agreement Deemed Loan Secured by Chattel MortgageДокумент2 страницыPCI Leasing v. Trojan Metal Industries: Financial Leasing Agreement Deemed Loan Secured by Chattel MortgageJay EmОценок пока нет

- Special Long-Term Transition Loan for DISCOMsДокумент4 страницыSpecial Long-Term Transition Loan for DISCOMssenthil031277Оценок пока нет

- Wellspring Capital LawsuitДокумент32 страницыWellspring Capital LawsuitWIS Digital News StaffОценок пока нет

- Loan Policy: Uttar Bihar Gramin BankДокумент27 страницLoan Policy: Uttar Bihar Gramin BankNaim Siddiqui100% (1)

- Memorandum On Behalf of AppelantДокумент13 страницMemorandum On Behalf of Appelantkumar kartikeyaОценок пока нет

- Bond Market in BangladeshДокумент11 страницBond Market in Bangladeshmisopstu100% (26)

- Arts 414-425 Study GuideДокумент108 страницArts 414-425 Study GuidejosefОценок пока нет

- What Is Forfeiture of ShareДокумент3 страницыWhat Is Forfeiture of ShareSathish SmartОценок пока нет