Вам также может понравиться

- Enron Corporation and AndersonДокумент14 страницEnron Corporation and AndersonAzizki WanieОценок пока нет

- Creative Accounting - SatyamДокумент21 страницаCreative Accounting - SatyamAkshat JainОценок пока нет

- Forensic AccountingДокумент12 страницForensic Accountingrazali mohammed0% (1)

- Enron Case History and Major Issues SummaryДокумент6 страницEnron Case History and Major Issues Summaryshanker23scribd100% (1)

- Ca Firm Exam Question AnswerДокумент17 страницCa Firm Exam Question AnswerSihinta AzraaОценок пока нет

- I) Short Term Solvency or Liquidity Ratios: Net IncomeДокумент2 страницыI) Short Term Solvency or Liquidity Ratios: Net Incomedude devilОценок пока нет

- An Analysis of Fraud Triangle and Responsibilities of AuditorsДокумент8 страницAn Analysis of Fraud Triangle and Responsibilities of AuditorsPrihandani AntonОценок пока нет

- Fraud Chapter 14Документ11 страницFraud Chapter 14Ann Yuheng DuОценок пока нет

- Research Paper (Comparative Analysis of Global Financial Laws)Документ17 страницResearch Paper (Comparative Analysis of Global Financial Laws)Soumya SaranjiОценок пока нет

- Analysis of Financial Statement of Corporation BankДокумент12 страницAnalysis of Financial Statement of Corporation Bankmathurankit100% (2)

- Case 2.3 HanauerДокумент10 страницCase 2.3 HanauerAlexa RodriguezОценок пока нет

- Case 4.6 Phar-MorДокумент2 страницыCase 4.6 Phar-MorMichele Thornton Santarsiero100% (2)

- Introduction, Conceptual Framework of The Study & Research DesignДокумент16 страницIntroduction, Conceptual Framework of The Study & Research DesignSтυριd・ 3尺ㄖ尺Оценок пока нет

- The Rise and Fall of Enron: A Guide to the ScandalДокумент28 страницThe Rise and Fall of Enron: A Guide to the ScandalJohn Philip De GuzmanОценок пока нет

- Fraud Theories PropertiesДокумент17 страницFraud Theories PropertiesJohn Adel100% (1)

- Parma Lat Case Study PDFДокумент3 страницыParma Lat Case Study PDFSaurav Singh0% (1)

- Leslie Fay Companies Audit RisksДокумент7 страницLeslie Fay Companies Audit Riskslumiradut70100% (2)

- Top Management FraudДокумент26 страницTop Management FraudBabelHardyОценок пока нет

- The Quality of Accruals and EarningsДокумент50 страницThe Quality of Accruals and Earningswil danОценок пока нет

- Case 3Документ4 страницыCase 3Bradley Warren100% (1)

- Auditing Sols To Homework Tute Qs - S2 2016 (WK 4 CH 8)Документ6 страницAuditing Sols To Homework Tute Qs - S2 2016 (WK 4 CH 8)sonima aroraОценок пока нет

- Internal Control: A Tool For The Audit CommitteeДокумент7 страницInternal Control: A Tool For The Audit CommitteeSakshi BansalОценок пока нет

- Chapter 2 Forensic Auditing and Fraud InvestigationДокумент92 страницыChapter 2 Forensic Auditing and Fraud Investigationabel habtamuОценок пока нет

- Accountants Perceptions Fraud Detection Prevention MethodsДокумент18 страницAccountants Perceptions Fraud Detection Prevention MethodsSeptyy Ningtyas100% (1)

- Misappropriation of AssetsДокумент2 страницыMisappropriation of AssetsElliot RichardОценок пока нет

- Audit Failure Case Studies Presentation For Online PortfolioДокумент19 страницAudit Failure Case Studies Presentation For Online Portfolioapi-282483815100% (1)

- CH 2 Accounting TransactionsДокумент52 страницыCH 2 Accounting TransactionsGizachew100% (1)

- Ethical Conflicts Enron PDFДокумент2 страницыEthical Conflicts Enron PDFJackieОценок пока нет

- Quiz 1Документ4 страницыQuiz 1justine reine cornicoОценок пока нет

- Cadbury Committee ReportДокумент3 страницыCadbury Committee ReportJitendra ChauhanОценок пока нет

- EY Prepares For Backlash Over Wirecard Scandal - Financial TimesДокумент5 страницEY Prepares For Backlash Over Wirecard Scandal - Financial Timespincer-pincerОценок пока нет

- L5 Case ProblemДокумент2 страницыL5 Case ProblemYassh Shirodkar50% (2)

- Royal AholdДокумент5 страницRoyal AholdRajaSaein0% (1)

- Inherent Risk LakesideДокумент2 страницыInherent Risk LakesideSunny Mae100% (1)

- Labor Review CasesДокумент161 страницаLabor Review CasesShalena Salazar-SangalangОценок пока нет

- Ethics, Fraud, and Internal ControlДокумент22 страницыEthics, Fraud, and Internal ControlsariОценок пока нет

- EnronДокумент12 страницEnronRoha JamilОценок пока нет

- Ifrs 15 BanksДокумент11 страницIfrs 15 BanksElena Panainte PanainteОценок пока нет

- Introduction to Auditing ConceptsДокумент17 страницIntroduction to Auditing ConceptsNayan MaldeОценок пока нет

- Case Study Opportunity FA PDFДокумент39 страницCase Study Opportunity FA PDFDiarany SucahyatiОценок пока нет

- Report 1 Associates and Agri-15022015Документ17 страницReport 1 Associates and Agri-15022015Iceberg Research100% (3)

- Study On Financial Ratio Analysis of Vellore Cooperative Sugar MillsДокумент7 страницStudy On Financial Ratio Analysis of Vellore Cooperative Sugar MillsTim CechiniОценок пока нет

- Enron ScandalДокумент9 страницEnron ScandalSalman JindranОценок пока нет

- Case 21Документ14 страницCase 21Gabriela LueiroОценок пока нет

- Enron ScandalДокумент16 страницEnron ScandalboldfaceaxisОценок пока нет

- Compilation of Accounting ScandalsДокумент7 страницCompilation of Accounting ScandalsYelyah HipolitoОценок пока нет

- Case 4.2 Comptronic CorporationДокумент2 страницыCase 4.2 Comptronic CorporationThao NguyenОценок пока нет

- Order To CashДокумент3 страницыOrder To CashPrashanth ChidambaramОценок пока нет

- Introduction to Auditing Chapter 1Документ8 страницIntroduction to Auditing Chapter 1scribdteaОценок пока нет

- The Rise and Fall of Enron PDFДокумент8 страницThe Rise and Fall of Enron PDFsuriya vasanth bОценок пока нет

- Checklist of Warning Signs Creative AccountingДокумент5 страницChecklist of Warning Signs Creative AccountingakkitheaviatorОценок пока нет

- Beneish M ScoreДокумент3 страницыBeneish M ScoreSudershan ThaibaОценок пока нет

- Louw 7Документ26 страницLouw 7drobinspaperОценок пока нет

- Application Services GovernanceДокумент9 страницApplication Services GovernancejhampiaОценок пока нет

- Case 3 FinalДокумент8 страницCase 3 Finalkyra84Оценок пока нет

- ScandalДокумент83 страницыScandalForeclosure FraudОценок пока нет

- Fraud 101Документ3 страницыFraud 101YesCFOОценок пока нет

- Private Equity Unchained: Strategy Insights for the Institutional InvestorОт EverandPrivate Equity Unchained: Strategy Insights for the Institutional InvestorОценок пока нет

- Enron - Answer 2011Документ7 страницEnron - Answer 2011Firda Azlinda100% (1)

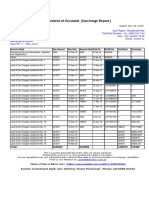

- Surcharge Report BTKSC-P05164Документ1 страницаSurcharge Report BTKSC-P05164Nasir Badshah AfridiОценок пока нет

- Deprival Value and Tobin's Q ExplainedДокумент16 страницDeprival Value and Tobin's Q ExplainedKartik Raj VarshneyОценок пока нет

- Sub-Contract Procedure 201720170424114636109Документ129 страницSub-Contract Procedure 201720170424114636109sanjaydeОценок пока нет

- EVN Jahresfinanzbericht 2011 12 deДокумент95 страницEVN Jahresfinanzbericht 2011 12 deLiv MariaОценок пока нет

- A Blueprint For Scaling Voluntary Carbon Markets To Meet The Climate ChallengeДокумент7 страницA Blueprint For Scaling Voluntary Carbon Markets To Meet The Climate ChallengeMardanОценок пока нет

- Role of Banking Sector in The Development of The Indian Economy in The Context of (Agriculture and Textile) Industry by Yogesh YadavДокумент40 страницRole of Banking Sector in The Development of The Indian Economy in The Context of (Agriculture and Textile) Industry by Yogesh Yadavyogesh0794Оценок пока нет

- ACTB212F Introduction To Accounting 2. (1) DocxДокумент18 страницACTB212F Introduction To Accounting 2. (1) DocxUsmän MïrżäОценок пока нет

- EPAF Sample Test PapersДокумент4 страницыEPAF Sample Test PapersmsmilansahuОценок пока нет

- Bir Form No. 0605Документ2 страницыBir Form No. 0605Ronald varrie Bautista50% (2)

- Financial Management Assignment (4) : Muhammad Fathy Dr. Sherif Abdel FattahДокумент21 страницаFinancial Management Assignment (4) : Muhammad Fathy Dr. Sherif Abdel FattahNerissa Mendoza RapanutОценок пока нет

- S11 Introdion Taluatioost Ofital EstimationДокумент42 страницыS11 Introdion Taluatioost Ofital Estimationsuhasshinde88Оценок пока нет

- Multitech Business School: Department of Professional StudiesДокумент5 страницMultitech Business School: Department of Professional StudiestubenaweambroseОценок пока нет

- Seoane v. FrancoДокумент3 страницыSeoane v. FrancoMariz RegalaОценок пока нет

- Ar2018 EnglishДокумент435 страницAr2018 Englishgl lugaОценок пока нет

- Free Trade ZoneДокумент3 страницыFree Trade ZoneCatherine JohnsonОценок пока нет

- Workbook For StudentДокумент63 страницыWorkbook For StudentVin PheakdeyОценок пока нет

- PPR 218 Key Steps To Retirement Income PlanningДокумент9 страницPPR 218 Key Steps To Retirement Income PlanningMaria CeciliaОценок пока нет

- 07 PUP Vs Golden HorizonДокумент3 страницы07 PUP Vs Golden HorizonFloyd Mago100% (1)

- Impact On Indian Econmy - Ignou NotesДокумент13 страницImpact On Indian Econmy - Ignou NotesVANSHIKA CHAUDHARYОценок пока нет

- PJSC National Bank Trust and Anor V Boris Mints and OrsДокумент33 страницыPJSC National Bank Trust and Anor V Boris Mints and OrshyenadogОценок пока нет

- Advanced ExcelДокумент6 страницAdvanced ExcelKeith Parker100% (4)

- Three Circle Family ModelДокумент5 страницThree Circle Family ModelAnoosha MazharОценок пока нет

- AICPAДокумент5 страницAICPAMikaela SalvadorОценок пока нет

- BBA Syllabus (Revised - 2010) - KUDДокумент65 страницBBA Syllabus (Revised - 2010) - KUDMALLIKARJUN100% (2)

- Key Terms Introduced or Emphasized in Chapter 4Документ2 страницыKey Terms Introduced or Emphasized in Chapter 4Faryal MughalОценок пока нет

- Presented By:-1.bijayananda Sahoo 2.jibesh Kumar Mohapatra 3.naresh Kumar Sahoo 4.soumya Surajit BiswalДокумент37 страницPresented By:-1.bijayananda Sahoo 2.jibesh Kumar Mohapatra 3.naresh Kumar Sahoo 4.soumya Surajit BiswaljibeshmОценок пока нет

- Annex HДокумент45 страницAnnex HImelda BugasОценок пока нет

- Principles of Office ManagementДокумент21 страницаPrinciples of Office Managementsszma67% (9)

- Jeda ConsДокумент2 страницыJeda ConsNathan ChinhondoОценок пока нет

- Aakriti Mathur: Ugo Panizza Cédric Tille Steven OngenaДокумент2 страницыAakriti Mathur: Ugo Panizza Cédric Tille Steven OngenaSaiganesh RameshОценок пока нет