Вам также может понравиться

- Module 2 Smart Task 2Документ3 страницыModule 2 Smart Task 2YASHASVI SHARMAОценок пока нет

- Internship - Vce1Документ2 страницыInternship - Vce1YASHASVI SHARMAОценок пока нет

- Module 2Документ3 страницыModule 2YASHASVI SHARMAОценок пока нет

- Ratio Analysis: Powered and Customised by Equitylevers World Private LimitedДокумент2 страницыRatio Analysis: Powered and Customised by Equitylevers World Private LimitedYASHASVI SHARMAОценок пока нет

- InternshipДокумент3 страницыInternshipYASHASVI SHARMAОценок пока нет

- The Latest: How To Leave On A Good Note When You've Been Laid OffДокумент2 страницыThe Latest: How To Leave On A Good Note When You've Been Laid OffYASHASVI SHARMAОценок пока нет

- Ca Project FileДокумент59 страницCa Project FileYASHASVI SHARMAОценок пока нет

- PW-Ratios Comp-1 Demo QДокумент1 страницаPW-Ratios Comp-1 Demo QYASHASVI SHARMAОценок пока нет

- Mail 1Документ1 страницаMail 1YASHASVI SHARMAОценок пока нет

- VCE Summer Internship Program 2020: Final Project Selection ListДокумент2 страницыVCE Summer Internship Program 2020: Final Project Selection ListYASHASVI SHARMAОценок пока нет

- Udemy Project AnalysisДокумент23 страницыUdemy Project AnalysisYASHASVI SHARMAОценок пока нет

- Porter 5 Force Model BankДокумент9 страницPorter 5 Force Model BankYASHASVI SHARMAОценок пока нет

- Pestle Analysis Banking IndustryДокумент17 страницPestle Analysis Banking IndustryYASHASVI SHARMA50% (4)

- New Microsoft Excel WorksheetДокумент1 страницаNew Microsoft Excel WorksheetYASHASVI SHARMAОценок пока нет

- Project Finance Smart TaskДокумент5 страницProject Finance Smart TaskYASHASVI SHARMAОценок пока нет

- Report For Corporate Skill Development-I: Title Table of ContentsДокумент2 страницыReport For Corporate Skill Development-I: Title Table of ContentsYASHASVI SHARMAОценок пока нет

- For Engineering and Management Students: Ardhan Onsulting Ngineers Internships - Training - CounselingДокумент6 страницFor Engineering and Management Students: Ardhan Onsulting Ngineers Internships - Training - CounselingYASHASVI SHARMAОценок пока нет

- Marking Scheme Subject: Science Term I Class: Vi Q. No. Mark To Awarded For Each Answer MarksДокумент6 страницMarking Scheme Subject: Science Term I Class: Vi Q. No. Mark To Awarded For Each Answer MarksYASHASVI SHARMAОценок пока нет

- Major Project 2018-19Документ10 страницMajor Project 2018-19YASHASVI SHARMAОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Sales - Breach of Contract, Extinguishment of SaleДокумент26 страницSales - Breach of Contract, Extinguishment of SaleErika WijangcoОценок пока нет

- The Capital Budgeting Decision: Mcgraw-Hill/IrwinДокумент44 страницыThe Capital Budgeting Decision: Mcgraw-Hill/IrwinLAMOUCHI RIMОценок пока нет

- Documentary Stamp Tax - Bureau of Internal RevenueДокумент12 страницDocumentary Stamp Tax - Bureau of Internal Revenueroy rebosuraОценок пока нет

- Class 11 - Business StudiesДокумент26 страницClass 11 - Business StudiesSri RaghulОценок пока нет

- T778 Child Care Expenses DeductionДокумент4 страницыT778 Child Care Expenses DeductionbatmanbittuОценок пока нет

- Employee Details: Old PPO NumberДокумент2 страницыEmployee Details: Old PPO NumberShubham ShakyaОценок пока нет

- Structure of Indian Capital Market With DiagramДокумент2 страницыStructure of Indian Capital Market With DiagramGinu George75% (4)

- WAPO 2019 Final Draft XXXДокумент229 страницWAPO 2019 Final Draft XXXRenatus shijaОценок пока нет

- Tottenham CaseДокумент19 страницTottenham Casekranilrai75% (8)

- Chapter 12 Solutions 2241Документ18 страницChapter 12 Solutions 2241JamesОценок пока нет

- Internship Report On NBPДокумент64 страницыInternship Report On NBPbbaahmad89Оценок пока нет

- FIAT and Cristler Case Study.Документ6 страницFIAT and Cristler Case Study.mbiradar85Оценок пока нет

- A Credit Rating Evaluates The Credit Worthiness of An Issuer of Specific Types of DebtДокумент17 страницA Credit Rating Evaluates The Credit Worthiness of An Issuer of Specific Types of Debtlucaciu_ale6517Оценок пока нет

- Verdun Commercial Paper OutlineДокумент63 страницыVerdun Commercial Paper Outlinetherunningman55Оценок пока нет

- Finance & CreditДокумент3 страницыFinance & Creditel khaiat mohamed amineОценок пока нет

- March 2010 Part 1 InsightДокумент63 страницыMarch 2010 Part 1 InsightSony AxleОценок пока нет

- Fintech FinalДокумент34 страницыFintech FinalanilОценок пока нет

- A Ratio Analysis Report On FINALДокумент36 страницA Ratio Analysis Report On FINALPrachi Dalal96% (27)

- China Construction BankДокумент10 страницChina Construction BankFRANCIS JOSEPHОценок пока нет

- 2019-12 PDFДокумент6 страниц2019-12 PDFNur DanielОценок пока нет

- 13.1 Exchange Rates and International TransactionsДокумент27 страниц13.1 Exchange Rates and International Transactionsjandihuyen83% (6)

- DEC 2016 AnswersДокумент37 страницDEC 2016 AnswersBKS SannyasiОценок пока нет

- In Fs Fintech India Ready For Breakout Noexp PDFДокумент44 страницыIn Fs Fintech India Ready For Breakout Noexp PDFRajyaLakshmiОценок пока нет

- Impact of Corona Virus On Mutual Fund by Sadanand IbitwarДокумент14 страницImpact of Corona Virus On Mutual Fund by Sadanand Ibitwarjai shree ramОценок пока нет

- Week3. CHAPTER 34 - SHARE-BASED PAYMENTS PART 1Документ17 страницWeek3. CHAPTER 34 - SHARE-BASED PAYMENTS PART 1Loi KkimakimОценок пока нет

- Financial Statements For Jollibee Foods CorporationДокумент7 страницFinancial Statements For Jollibee Foods CorporationFretelle Rimafranca75% (4)

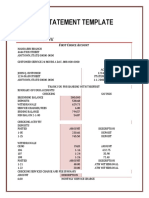

- Bank Statement Template 16 PDFДокумент2 страницыBank Statement Template 16 PDFBara Creatives50% (2)

- Share MarketДокумент14 страницShare Marketbholu436100% (6)

- Derivatives Financial Market in India: Perspective and FutureДокумент26 страницDerivatives Financial Market in India: Perspective and Futuregaganhungama007Оценок пока нет

- PGS AP100080 AP Withholding Tax PMNT RPTДокумент16 страницPGS AP100080 AP Withholding Tax PMNT RPTSarwar GolamОценок пока нет