Вам также может понравиться

- Solvents: Northwest EuropeДокумент9 страницSolvents: Northwest EuropegeorgevarsasОценок пока нет

- Solventswire 310718Документ10 страницSolventswire 310718Mohammed BabatinОценок пока нет

- Chemical Business Focus: A Monthly Roundup and Analysis of The Key Factors Shaping World Chemical MarketsДокумент27 страницChemical Business Focus: A Monthly Roundup and Analysis of The Key Factors Shaping World Chemical Marketssanjayshah99Оценок пока нет

- Solvents WireДокумент9 страницSolvents Wirerbrijeshgbiresearch100% (1)

- PPДокумент9 страницPPEmmylouCasanovaОценок пока нет

- Chemical Business FocusДокумент34 страницыChemical Business FocusAtikah Abu BakarОценок пока нет

- Fertecon Ammonia Report: 4 September 2008Документ8 страницFertecon Ammonia Report: 4 September 2008Mike MureyaniОценок пока нет

- Lpgas: Northwest Europe Daily Assessments $/MTДокумент6 страницLpgas: Northwest Europe Daily Assessments $/MTMilkiss SweetОценок пока нет

- Argus Biofuels (2023!08!08)Документ11 страницArgus Biofuels (2023!08!08)Pitipat LeeОценок пока нет

- Argus Propylene and DerivativesДокумент11 страницArgus Propylene and Derivativesagarwalashwin32Оценок пока нет

- AsiaNaphtha SampleДокумент14 страницAsiaNaphtha SamplefajaradityadarmaОценок пока нет

- Lpgas: Northwest Europe Daily Assessments $/MTДокумент5 страницLpgas: Northwest Europe Daily Assessments $/MTMilkiss SweetОценок пока нет

- Euromktscan11072013 PDFДокумент8 страницEuromktscan11072013 PDFMelody CottonОценок пока нет

- Sample: Global BiodieselДокумент5 страницSample: Global BiodieselWiriyan JordyОценок пока нет

- Argus BiomassДокумент14 страницArgus BiomassVijendranArumugamОценок пока нет

- Platts 04 Janv 2013 PDFДокумент9 страницPlatts 04 Janv 2013 PDFWallace YankotyОценок пока нет

- Ryan Notes-October - 2014 - Avg1 PDFДокумент2 страницыRyan Notes-October - 2014 - Avg1 PDFAnyeliОценок пока нет

- Global Steel Price ReportДокумент21 страницаGlobal Steel Price ReportHùng DuyОценок пока нет

- European Marketscan: European Products ($/MT) ICE FuturesДокумент9 страницEuropean Marketscan: European Products ($/MT) ICE FuturesWallace YankotyОценок пока нет

- EuropeLPGReport Sample02082013Документ5 страницEuropeLPGReport Sample02082013Melody CottonОценок пока нет

- Rate Report 03.12.19Документ13 страницRate Report 03.12.19PP PolymerBazaarОценок пока нет

- Eac 13 11Документ1 страницаEac 13 11Elham DrsОценок пока нет

- European Marketscan: Expert PDF EvaluationДокумент10 страницEuropean Marketscan: Expert PDF EvaluationWallace YankotyОценок пока нет

- Lpgas: Northwest Europe Daily Assessments $/MTДокумент5 страницLpgas: Northwest Europe Daily Assessments $/MTMilkiss SweetОценок пока нет

- Chemicals BenzeneДокумент3 страницыChemicals BenzeneTrizEugheneSilesОценок пока нет

- European Marketscan: European Products ($/MT) ICE FuturesДокумент9 страницEuropean Marketscan: European Products ($/MT) ICE FuturesWallace YankotyОценок пока нет

- Chemicals Dimethyl TerephthalateДокумент3 страницыChemicals Dimethyl TerephthalateHafiz Rama DevaraОценок пока нет

- Eum 20231110Документ27 страницEum 20231110Imperium InvestasОценок пока нет

- European Marketscan: European Products ($/MT) ICE FuturesДокумент9 страницEuropean Marketscan: European Products ($/MT) ICE FuturesWallace YankotyОценок пока нет

- Trends and DataДокумент1 страницаTrends and DataelainejournalistОценок пока нет

- SPR 20180221Документ16 страницSPR 20180221VivekОценок пока нет

- Facts About Diesel Prices and The Australian Fuel MarketДокумент5 страницFacts About Diesel Prices and The Australian Fuel MarketTimОценок пока нет

- Argus International LPGДокумент11 страницArgus International LPGAnonymous R0VFaZQ100% (1)

- Precios Del Benceno y Otros Aromaticos en El MercadoДокумент24 страницыPrecios Del Benceno y Otros Aromaticos en El MercadoRodrigo Alejo0% (1)

- Chemicals PricesДокумент16 страницChemicals PricesMrityunjay KumarОценок пока нет

- Greenea Market Watch April 2019Документ6 страницGreenea Market Watch April 2019Kerr JavierОценок пока нет

- European Marketscan: European Products ($/MT) ICE FuturesДокумент9 страницEuropean Marketscan: European Products ($/MT) ICE FuturesWallace YankotyОценок пока нет

- Iocl Haldia ReportДокумент99 страницIocl Haldia ReportArkadev GhoshОценок пока нет

- Chlor-Alkali Market ReportДокумент38 страницChlor-Alkali Market Reportshine2ricaОценок пока нет

- Petrochemicalscan Oct 05 2011Документ3 страницыPetrochemicalscan Oct 05 2011spdhebar3280Оценок пока нет

- Availability of Naphtha in AsiaДокумент5 страницAvailability of Naphtha in AsiaMoosa NaseerОценок пока нет

- Eum 20221125 221126 102827Документ32 страницыEum 20221125 221126 102827capttariqОценок пока нет

- Vam PricesДокумент28 страницVam PricesMandar J DeshpandeОценок пока нет

- Platts 02 Janv 2013 PDFДокумент9 страницPlatts 02 Janv 2013 PDFWallace YankotyОценок пока нет

- Argus Sulphur (2018-07-12)Документ14 страницArgus Sulphur (2018-07-12)SaurabhОценок пока нет

- European Marketscan: European Products ($/MT) ICE FuturesДокумент10 страницEuropean Marketscan: European Products ($/MT) ICE FuturesWallace YankotyОценок пока нет

- Ch21 - MBДокумент41 страницаCh21 - MBannasitОценок пока нет

- Bunker FuelДокумент5 страницBunker Fuelmathew miteОценок пока нет

- LPG 20140106Документ5 страницLPG 20140106Milkiss SweetОценок пока нет

- Polypropylene (Asia-Pacific) : by Jackie Wong, Lucy ShuaiДокумент7 страницPolypropylene (Asia-Pacific) : by Jackie Wong, Lucy ShuaingocanhОценок пока нет

- Daily Global Polyolefins Report - Friday - September 01st - 2023Документ19 страницDaily Global Polyolefins Report - Friday - September 01st - 2023Vaibhav Sunil PatilОценок пока нет

- OPIS Asia Naphtha Report 20180212Документ15 страницOPIS Asia Naphtha Report 20180212Sunil NagarОценок пока нет

- Petrosil Base Oil Report - March 15, 2010 - 0Документ20 страницPetrosil Base Oil Report - March 15, 2010 - 0Divik TanwarОценок пока нет

- ICIS Propylene Asia - Pricing & Insight-29-Oct-2021Документ6 страницICIS Propylene Asia - Pricing & Insight-29-Oct-2021limsyuyinОценок пока нет

- ICIS Propylene Asia - Pricing & Insight-29-Oct-2021Документ6 страницICIS Propylene Asia - Pricing & Insight-29-Oct-2021limsyuyinОценок пока нет

- Argus FMB Ammonia Precios Amoniaco PDFДокумент7 страницArgus FMB Ammonia Precios Amoniaco PDFCarlos Manuel Castillo SalasОценок пока нет

- Argus PolymersДокумент11 страницArgus PolymersIvan PavlovОценок пока нет

- Coal Trader: InternationalДокумент4 страницыCoal Trader: InternationalandreasОценок пока нет

- Foundations of Natural Gas Price Formation: Misunderstandings Jeopardizing the Future of the IndustryОт EverandFoundations of Natural Gas Price Formation: Misunderstandings Jeopardizing the Future of the IndustryРейтинг: 5 из 5 звезд5/5 (1)

- KBF (E5.2) : Service ManualДокумент140 страницKBF (E5.2) : Service ManualgeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 14.02.15 PDFДокумент19 страницAthenian Shipbrokers - Monthy Report - 14.02.15 PDFgeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 14.01.15 PDFДокумент18 страницAthenian Shipbrokers - Monthy Report - 14.01.15 PDFgeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 13.12.15 PDFДокумент18 страницAthenian Shipbrokers - Monthy Report - 13.12.15 PDFgeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 13.11.15 PDFДокумент20 страницAthenian Shipbrokers - Monthy Report - 13.11.15 PDFgeorgevarsas0% (1)

- C H S&P W B: Larkson Ellas Eekly UlletinДокумент2 страницыC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 14.08.15Документ17 страницAthenian Shipbrokers - Monthy Report - 14.08.15georgevarsasОценок пока нет

- C H S&P W B: Larkson Ellas Eekly UlletinДокумент3 страницыC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasОценок пока нет

- C H S&P W B: Larkson Ellas Eekly UlletinДокумент2 страницыC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasОценок пока нет

- Advanced - Week 24 - 16.06.10Документ11 страницAdvanced - Week 24 - 16.06.10georgevarsasОценок пока нет

- C H S&P W B: Larkson Ellas Eekly UlletinДокумент2 страницыC H S&P W B: Larkson Ellas Eekly UlletingeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 14.07.15 PDFДокумент18 страницAthenian Shipbrokers - Monthy Report - 14.07.15 PDFgeorgevarsasОценок пока нет

- Athenian Shipbrokers - Monthy Report - 13.11.15 PDFДокумент20 страницAthenian Shipbrokers - Monthy Report - 13.11.15 PDFgeorgevarsas0% (1)

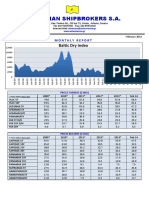

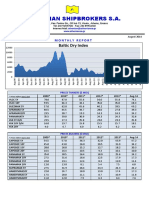

- Athenian Shipbrokers S.A.: Baltic Dry IndexДокумент17 страницAthenian Shipbrokers S.A.: Baltic Dry IndexgeorgevarsasОценок пока нет

- Advanced - Week 52 - 16.12.26 PDFДокумент9 страницAdvanced - Week 52 - 16.12.26 PDFgeorgevarsasОценок пока нет

- Advanced - Week 12 - 16.03.18 PDFДокумент10 страницAdvanced - Week 12 - 16.03.18 PDFgeorgevarsasОценок пока нет

- Advanced - Week 23 - 16.06.03 PDFДокумент11 страницAdvanced - Week 23 - 16.06.03 PDFgeorgevarsasОценок пока нет

- Project AVUДокумент90 страницProject AVUSumit KaushikОценок пока нет

- MethaneДокумент1 страницаMethaneKukurooОценок пока нет

- Filling Station Guide PDFДокумент2 страницыFilling Station Guide PDFKizaHimmlerОценок пока нет

- Modbus Register MappingДокумент564 страницыModbus Register MappingAremu Adetola100% (3)

- Questions For 2nd Mate OralsДокумент10 страницQuestions For 2nd Mate Oralsinkugeorge100% (1)

- Dum Truck Komatsu hd465-7hd605-7 PDFДокумент395 страницDum Truck Komatsu hd465-7hd605-7 PDFamin100% (1)

- Service Manual Roiline Model 570 and 884Документ80 страницService Manual Roiline Model 570 and 884complexcircuit100% (1)

- Passenger Provisions Table 2.3.a DGR 56 enДокумент2 страницыPassenger Provisions Table 2.3.a DGR 56 enbethanyaОценок пока нет

- As 3814-2009 Industrial and Commercial Gas-Fired AppliancesДокумент9 страницAs 3814-2009 Industrial and Commercial Gas-Fired AppliancesSAI Global - APACОценок пока нет

- Buffer and Barrier FluidsДокумент10 страницBuffer and Barrier FluidsFelipeFonckmОценок пока нет

- Fire Protection and PreventionДокумент3 страницыFire Protection and PreventionMikeKenly Guiroy-TungalОценок пока нет

- Polf TheoryДокумент44 страницыPolf TheoryrahmanqasemОценок пока нет

- ITR Daily ReportДокумент1 004 страницыITR Daily Reportsamer8saifОценок пока нет

- Industrial Valves - Legris Parker นิวเมติกДокумент49 страницIndustrial Valves - Legris Parker นิวเมติกParinpa KetarОценок пока нет

- Geophysics - Dim SpotДокумент3 страницыGeophysics - Dim Spotabc_edfОценок пока нет

- Marine Medium D2842 E-17-11Документ4 страницыMarine Medium D2842 E-17-11Joana Natalia PardedeОценок пока нет

- Ykk Training PPT On LocomotiveДокумент17 страницYkk Training PPT On LocomotiverajendraОценок пока нет

- 04 Pen 17529 S17 Model AnswerДокумент18 страниц04 Pen 17529 S17 Model AnswerSachinОценок пока нет

- Operation Aspects & Boiler EmergenciesДокумент54 страницыOperation Aspects & Boiler EmergenciesPravivVivpraОценок пока нет

- Optimization of A Refinery Crude Distillation Unit in The Context of Total Energy RequirementДокумент34 страницыOptimization of A Refinery Crude Distillation Unit in The Context of Total Energy RequirementKhafid Al Na'imОценок пока нет

- World Bioufuels MapДокумент1 страницаWorld Bioufuels MapSugarcaneBlogОценок пока нет

- Zyme-Flow Decon Technology R6 Promo PDFДокумент4 страницыZyme-Flow Decon Technology R6 Promo PDFĐậu BắpОценок пока нет

- Leak Test Procedure of BoilerДокумент3 страницыLeak Test Procedure of BoilerDavid Hoffman100% (3)

- LPG-BUS-HSE-IST-0007 - Safety Data Sheet - Liquefied Petroleum GasДокумент10 страницLPG-BUS-HSE-IST-0007 - Safety Data Sheet - Liquefied Petroleum GasElias Jarjoura100% (1)

- UOP 99-07 Pentane-Insoluble Matter in Petroleum Oils Using A Membrane FilterДокумент10 страницUOP 99-07 Pentane-Insoluble Matter in Petroleum Oils Using A Membrane FilterMorteza SepehranОценок пока нет

- Fire Protection System According To NBC IndiaДокумент30 страницFire Protection System According To NBC IndiaMadhukar Gupta100% (1)

- Manufacture of Casing String: Billet Hot CoilДокумент12 страницManufacture of Casing String: Billet Hot Coilkaelel18Оценок пока нет

- SealingДокумент21 страницаSealingAlexander BowersОценок пока нет

- Electricity Use in Country BurmaДокумент140 страницElectricity Use in Country BurmabwarsaraОценок пока нет