Вам также может понравиться

- An Internship Report On Askari Bank Limited: The University of Azad Jammu & Kashmir MuzaffarabadДокумент37 страницAn Internship Report On Askari Bank Limited: The University of Azad Jammu & Kashmir Muzaffarabadmuhammad azharОценок пока нет

- University of Central Punjab: Askari Bank - Internship ReportДокумент38 страницUniversity of Central Punjab: Askari Bank - Internship ReportHammad ImranОценок пока нет

- Internship Report NBPДокумент46 страницInternship Report NBPHusnain AwanОценок пока нет

- Viden Io Summer Internship Report HDFC Bank Summer Internship Final End Report PDFДокумент66 страницViden Io Summer Internship Report HDFC Bank Summer Internship Final End Report PDFrupaliОценок пока нет

- Report On Trade Operating and Client Management Process of UCB Stock Brokerage LimitedДокумент33 страницыReport On Trade Operating and Client Management Process of UCB Stock Brokerage LimitedSelim KhanОценок пока нет

- A Study On Ratio Analysis On EFU: Master of Business Administration (Finance)Документ63 страницыA Study On Ratio Analysis On EFU: Master of Business Administration (Finance)Usman MalikОценок пока нет

- Check PlagiarismДокумент54 страницыCheck PlagiarismtaimoorОценок пока нет

- Vipul FinalДокумент142 страницыVipul FinalMaster RajharshОценок пока нет

- Internship Report On An In-Depth Analysis of The Consumer Division & Performance Evaluation: IDLCДокумент44 страницыInternship Report On An In-Depth Analysis of The Consumer Division & Performance Evaluation: IDLCNazia NusratОценок пока нет

- Mba PDFДокумент48 страницMba PDFMinhajul Islam MimОценок пока нет

- Ahsan Internship ReportДокумент53 страницыAhsan Internship ReportShakeeb Aslam RajputОценок пока нет

- V Guard 5.25Документ68 страницV Guard 5.25Alex JosephОценок пока нет

- An Analysis of Customer Demography and Perception About Agent Banking To Start Agent Banking Business by Prime Bank LimitedДокумент48 страницAn Analysis of Customer Demography and Perception About Agent Banking To Start Agent Banking Business by Prime Bank LimitedTasfia HaqueОценок пока нет

- Sajid Final Zong ReportДокумент37 страницSajid Final Zong ReportKhurram Warriach0% (1)

- Internshipreport 170311083309Документ33 страницыInternshipreport 170311083309RahulОценок пока нет

- Abdur Rehman Report 17 05 202Документ40 страницAbdur Rehman Report 17 05 202Malik RohailОценок пока нет

- Internship Report On The Bank of Azad Jammu and Kashmir Main Branch MuzaffarabadДокумент48 страницInternship Report On The Bank of Azad Jammu and Kashmir Main Branch Muzaffarabadsam abbasОценок пока нет

- Internship Report On The National Bank of Pakistan SwabiДокумент50 страницInternship Report On The National Bank of Pakistan SwabiZain Ul AbideenОценок пока нет

- Internship Report MCB Bank LTDДокумент53 страницыInternship Report MCB Bank LTDShakeeb Aslam RajputОценок пока нет

- Max Retail Syed YusufДокумент69 страницMax Retail Syed Yusufabhinov prakashОценок пока нет

- Audit Practice ManualДокумент456 страницAudit Practice ManualzainniprinceОценок пока нет

- Internship Report On: Weatherford International PakistanДокумент32 страницыInternship Report On: Weatherford International Pakistanayub shahОценок пока нет

- Business PlanДокумент103 страницыBusiness PlanRishabh SarawagiОценок пока нет

- Intership Report On SWOT Analysis of Saic GroupДокумент39 страницIntership Report On SWOT Analysis of Saic GroupMohammad Rakibul IslamОценок пока нет

- Final Draft of Healthy BiteДокумент24 страницыFinal Draft of Healthy Bitemaleeha sajjadОценок пока нет

- Ephrem Tilahun ResearchДокумент34 страницыEphrem Tilahun Researchwudineh debebeОценок пока нет

- Capital Structure On Idbi Federal Life Insurance Co. LTD.: Research Project Report ONДокумент74 страницыCapital Structure On Idbi Federal Life Insurance Co. LTD.: Research Project Report ONDeep ChoudharyОценок пока нет

- ABR Final Report Himanshu EA19DXB005 SignedДокумент90 страницABR Final Report Himanshu EA19DXB005 SignedPayal BОценок пока нет

- Final Project Financial Statement Analysis of Bank Al Falah: Fasco - BukДокумент88 страницFinal Project Financial Statement Analysis of Bank Al Falah: Fasco - BukTahir SahabОценок пока нет

- MRK - Spring 2023 - COMI619 - 5 - MC210401667Документ28 страницMRK - Spring 2023 - COMI619 - 5 - MC210401667MuhammadSaadAhmadОценок пока нет

- Internship Report On MCB Lari Adda Mansehra Branch (1671) : Department of Management Sciences Hazara University MansehraДокумент55 страницInternship Report On MCB Lari Adda Mansehra Branch (1671) : Department of Management Sciences Hazara University MansehraarsalanОценок пока нет

- The Implementation of Goods and Service TaxДокумент10 страницThe Implementation of Goods and Service TaxAffifah GhazaliОценок пока нет

- Adnan ThesisДокумент51 страницаAdnan ThesisMohammad Naveed Hashmi100% (1)

- Ads669 Nor Suriyani Shafei 2015466266Документ32 страницыAds669 Nor Suriyani Shafei 2015466266NOR SURIYANI BINTI SHAFEIОценок пока нет

- Brand Audit PIA - GRP 3Документ68 страницBrand Audit PIA - GRP 3Muhammad HasanОценок пока нет

- Effects of Corporate Governance On The Performance of Commercial Banks, KenyaДокумент58 страницEffects of Corporate Governance On The Performance of Commercial Banks, KenyaHugo Fernando Ceballos GomezОценок пока нет

- Institute of Finance Management: Chuo Cha Usimamizi Wa FedhaДокумент3 страницыInstitute of Finance Management: Chuo Cha Usimamizi Wa FedhaDaud M EmmanuelОценок пока нет

- Intern Report KhairulДокумент60 страницIntern Report KhairulgmosОценок пока нет

- Post-Sanction Monitoring of Industrial Advances in Indian BankДокумент127 страницPost-Sanction Monitoring of Industrial Advances in Indian BankChiranjit Basu100% (4)

- Internship Report On ZTBL Title PagesДокумент19 страницInternship Report On ZTBL Title PagesWasimOrakzaiОценок пока нет

- Swathi 1ki16mba47front PageДокумент12 страницSwathi 1ki16mba47front PageShivu MkОценок пока нет

- Marketing Thesis 24-02-2020Документ52 страницыMarketing Thesis 24-02-2020SSPL ReportsОценок пока нет

- Profitability Analysis of Sanima Bank Limited: A Project ReportДокумент40 страницProfitability Analysis of Sanima Bank Limited: A Project ReportSurya Satore0% (1)

- FIN619 Project VUДокумент88 страницFIN619 Project VUSyed Faisal Bukhari67% (3)

- Sajja Intern Report Final Draft SajjaaДокумент44 страницыSajja Intern Report Final Draft SajjaaAmar YonjanОценок пока нет

- Series 79 Outline 0Документ28 страницSeries 79 Outline 0Michael Luna100% (1)

- Fini619-Internship Report Format (NEW)Документ8 страницFini619-Internship Report Format (NEW)Zeeshan JunejoОценок пока нет

- Mba 7099 20146381Документ75 страницMba 7099 20146381Maheshika LamahewageОценок пока нет

- Internship Report On Nundhyar Engineering & Construction BattagramДокумент65 страницInternship Report On Nundhyar Engineering & Construction BattagramFaisal AwanОценок пока нет

- SamrajДокумент62 страницыSamrajmanisha singhОценок пока нет

- 7 0 - OSH Professional Entity Registration v3.0 EnglishДокумент40 страниц7 0 - OSH Professional Entity Registration v3.0 Englishumesh kumarОценок пока нет

- A Comparative Financial Analysis of Glaxosmithkline Bangladesh LimitedДокумент43 страницыA Comparative Financial Analysis of Glaxosmithkline Bangladesh LimitedMd ShohanОценок пока нет

- Foreign Exchange Risk Management in Commercial Banks in PakistanДокумент65 страницForeign Exchange Risk Management in Commercial Banks in PakistanMaroof Hussain Sabri100% (5)

- Tanzim Rafiq - ID# 13304149 - Internship Report - Robi Axiata LimitedДокумент48 страницTanzim Rafiq - ID# 13304149 - Internship Report - Robi Axiata LimitedLeroy SaneОценок пока нет

- Special Audit in Manufacturing Company: Internship ReportДокумент44 страницыSpecial Audit in Manufacturing Company: Internship ReportAdnanОценок пока нет

- WC FINAL PROJECTДокумент87 страницWC FINAL PROJECTSushmita BarlaОценок пока нет

- Future Lifestyle FashionsДокумент118 страницFuture Lifestyle Fashionssneha mathewОценок пока нет

- Internship Report On Mat Technologies Islamabad, PakistanДокумент79 страницInternship Report On Mat Technologies Islamabad, PakistanWaqasabdullahОценок пока нет

- Evaluation of the International Finance Corporation's Global Trade Finance Program, 2006-12От EverandEvaluation of the International Finance Corporation's Global Trade Finance Program, 2006-12Оценок пока нет

- Putting Higher Education to Work: Skills and Research for Growth in East AsiaОт EverandPutting Higher Education to Work: Skills and Research for Growth in East AsiaОценок пока нет

- Interest Rate Hedging-ExamplesДокумент9 страницInterest Rate Hedging-ExamplesMuneeb AmanОценок пока нет

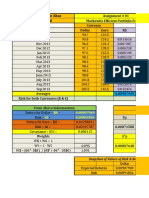

- Mushtaq Hussain Khan MM133038: Assignment # 01 Markowitz Efficient Portfolio Frontier Currency Months Dollar Euro R$Документ6 страницMushtaq Hussain Khan MM133038: Assignment # 01 Markowitz Efficient Portfolio Frontier Currency Months Dollar Euro R$Muneeb AmanОценок пока нет

- Question???: What Are The Determinants of Dividend Policy in Pakistan??Документ5 страницQuestion???: What Are The Determinants of Dividend Policy in Pakistan??Muneeb AmanОценок пока нет

- Summary of Results and Their InterpretationДокумент1 страницаSummary of Results and Their InterpretationMuneeb AmanОценок пока нет

- Interest Rate Hedging-ExamplesДокумент9 страницInterest Rate Hedging-ExamplesMuneeb AmanОценок пока нет

- Question???: What Are The Determinants of Dividend Policy in Pakistan??Документ5 страницQuestion???: What Are The Determinants of Dividend Policy in Pakistan??Muneeb AmanОценок пока нет

- Greeks PutДокумент27 страницGreeks PutMuneeb AmanОценок пока нет

- Final Fall 2012Документ1 страницаFinal Fall 2012Muneeb AmanОценок пока нет

- Venture Capital in PakistanДокумент2 страницыVenture Capital in PakistanMuneeb AmanОценок пока нет

- Assignment FRMДокумент4 страницыAssignment FRMMuneeb AmanОценок пока нет

- Venture Capital in PakistanДокумент2 страницыVenture Capital in PakistanMuneeb AmanОценок пока нет

- Riphah International UniversityДокумент2 страницыRiphah International UniversityMuneeb AmanОценок пока нет

- Investment Analysis-ButtДокумент11 страницInvestment Analysis-ButtMuneeb AmanОценок пока нет

- Formula Sheet: C S N d Xe N d S X r+ σ τ σ τДокумент2 страницыFormula Sheet: C S N d Xe N d S X r+ σ τ σ τMuneeb AmanОценок пока нет

- Assignment FRMДокумент4 страницыAssignment FRMMuneeb AmanОценок пока нет

- ModelsДокумент21 страницаModelsEjaz Ali MaitlaОценок пока нет

- PrintoutДокумент5 страницPrintoutMuneeb AmanОценок пока нет

- 2014 2015 2016 2017 2018 AssetsДокумент6 страниц2014 2015 2016 2017 2018 AssetsMuneeb AmanОценок пока нет

- Chapter No 08 CAMEL Framework: Capital Adequacy-CДокумент10 страницChapter No 08 CAMEL Framework: Capital Adequacy-CMuneeb AmanОценок пока нет

- University of Azad Jammu and Kashmir Muzaffarabad: Muneeb Aman Roll No: 02 Regd. No. 2015-GMDB (B) - 000573Документ37 страницUniversity of Azad Jammu and Kashmir Muzaffarabad: Muneeb Aman Roll No: 02 Regd. No. 2015-GMDB (B) - 000573Muneeb AmanОценок пока нет

- Honor StatementДокумент1 страницаHonor StatementMuneeb AmanОценок пока нет

- Week 6 and Week 7Документ49 страницWeek 6 and Week 7Muneeb AmanОценок пока нет

- Hira 2Документ22 страницыHira 2Muneeb AmanОценок пока нет

- Summary and RecommendationsДокумент4 страницыSummary and RecommendationsMuneeb AmanОценок пока нет

- Investor Account - Zakat Declaration FormДокумент2 страницыInvestor Account - Zakat Declaration FormMuhammad WasimОценок пока нет

- Cash and Cash Equivalents Sample ProblemsДокумент7 страницCash and Cash Equivalents Sample ProblemsCamille Donaire LimОценок пока нет

- Activities of ": Uttara Finance and Investment LTD"Документ2 страницыActivities of ": Uttara Finance and Investment LTD"FarukIslamОценок пока нет

- FF68 Manual Check Deposit in Sap PDFДокумент8 страницFF68 Manual Check Deposit in Sap PDFShailesh SuranaОценок пока нет

- Bni Bilingual 30 Juni 2020 ReleasedДокумент331 страницаBni Bilingual 30 Juni 2020 ReleasedGiovanno HermawanОценок пока нет

- Risk Management For Banking SectorДокумент46 страницRisk Management For Banking SectorNaeem Uddin88% (17)

- Study On Foreign Exchange Remittances & Interbank DealingsДокумент95 страницStudy On Foreign Exchange Remittances & Interbank DealingsSachin KajaveОценок пока нет

- Banking and FinanceДокумент74 страницыBanking and FinancekimmheanОценок пока нет

- Bank Reconmciliation ProcessДокумент13 страницBank Reconmciliation ProcessRachelleОценок пока нет

- Sibl-Fs 30 June 2018Документ322 страницыSibl-Fs 30 June 2018Faizal KhanОценок пока нет

- AP Handout 01 Audit of Cash PDFДокумент6 страницAP Handout 01 Audit of Cash PDFTherese AlmiraОценок пока нет

- Sarbati Devi v. Usha Devi AnalysisДокумент10 страницSarbati Devi v. Usha Devi AnalysisSameer Khedkar100% (1)

- Account Closure Request Form Yes BankДокумент1 страницаAccount Closure Request Form Yes BankRadheShyam0% (1)

- Scan1 PDFДокумент2 страницыScan1 PDFshaumyaОценок пока нет

- Bank Reconciliation ProcessДокумент6 страницBank Reconciliation ProcessbluephoeОценок пока нет

- Gand Mai Dalo BKLДокумент50 страницGand Mai Dalo BKLbaba baba black sheepОценок пока нет

- Blackbook 2Документ94 страницыBlackbook 2yogesh kumbharОценок пока нет

- 1.1 Organization Overview: 1,105,226,569 During The Year 2009. and in June 2010 Profit After Tax Is 793,726,000Документ94 страницы1.1 Organization Overview: 1,105,226,569 During The Year 2009. and in June 2010 Profit After Tax Is 793,726,000Md. Saiful IslamОценок пока нет

- Describe The Operation of A Petty Cash Fund. Companies Operate A Petty CashДокумент3 страницыDescribe The Operation of A Petty Cash Fund. Companies Operate A Petty CashLê Lý Nhân HậuОценок пока нет

- StudentДокумент34 страницыStudentKevin CheОценок пока нет

- Module 2 Bank Reconciliation Proof of CashДокумент2 страницыModule 2 Bank Reconciliation Proof of CashziОценок пока нет

- Business-Bank-Account MetroДокумент3 страницыBusiness-Bank-Account Metroussef oblivion0% (1)

- Agreements and Disclosures UbsДокумент88 страницAgreements and Disclosures UbsAxeliiNilssonОценок пока нет

- NBFC-2Документ18 страницNBFC-2nishiОценок пока нет

- Key From Unit 6 To Unit 10 Esp PDF FreeДокумент20 страницKey From Unit 6 To Unit 10 Esp PDF FreeTrần Đức TàiОценок пока нет

- BFSI Training Manual - PDF - 20230810 - 164502 - 0000Документ50 страницBFSI Training Manual - PDF - 20230810 - 164502 - 0000deepak643aОценок пока нет

- NCCBLДокумент69 страницNCCBLMd.Azam KhanОценок пока нет

- State Bank of IndiaДокумент33 страницыState Bank of IndiaGeetanjali TyagiОценок пока нет

- Fabm2121 Week 11-19Документ40 страницFabm2121 Week 11-19Jelyn Ramirez60% (5)

- A PROJECT REPORT ON Financial Assistance by The CBS Bank MBA FINANCE PROJECT REPORTДокумент72 страницыA PROJECT REPORT ON Financial Assistance by The CBS Bank MBA FINANCE PROJECT REPORTK Sagar KondollaОценок пока нет