Вам также может понравиться

- SME FinanceДокумент13 страницSME FinanceDaren WayneОценок пока нет

- Research Journal of Finance and Accounting ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online) DOI: 10.7176/RJFA Vol.10, No.3, 2019Документ12 страницResearch Journal of Finance and Accounting ISSN 2222-1697 (Paper) ISSN 2222-2847 (Online) DOI: 10.7176/RJFA Vol.10, No.3, 2019daniel nugusieОценок пока нет

- Credit Rationing and Risk Management For Smes: The Way Forward For South AfricaДокумент11 страницCredit Rationing and Risk Management For Smes: The Way Forward For South AfricaShehroz ShyziОценок пока нет

- Section 4 GroupsДокумент9 страницSection 4 GroupsAnokye AdamОценок пока нет

- Bank Financing for SMEs: Business Models and Lending PracticesДокумент43 страницыBank Financing for SMEs: Business Models and Lending PracticesBim NguyenОценок пока нет

- Determinants Predicting Credit Accessibility of Sme Evidence From BangladeshДокумент9 страницDeterminants Predicting Credit Accessibility of Sme Evidence From BangladeshËstėllę Christiānę Bissā ZambøОценок пока нет

- The Impact of Smes' Lending and Credit Guarantee On Bank Efficiency in South KoreaДокумент8 страницThe Impact of Smes' Lending and Credit Guarantee On Bank Efficiency in South KoreaLucky PrasetyoОценок пока нет

- The Causes of Loan DefaultДокумент9 страницThe Causes of Loan DefaultLazarus AmaniОценок пока нет

- Problems and Prospects of Smes Loan Management: A Study On Mercantile Bank Limited, Khulna BranchДокумент15 страницProblems and Prospects of Smes Loan Management: A Study On Mercantile Bank Limited, Khulna BranchKuntal GhoshОценок пока нет

- Non Performing Loan ThesisДокумент4 страницыNon Performing Loan ThesisPaperWritingServiceSuperiorpapersSpringfield100% (2)

- Collateral in Smes' Lending: Banks' Requirements Vs Customers' ExpectationsДокумент9 страницCollateral in Smes' Lending: Banks' Requirements Vs Customers' ExpectationsTrina GoswamiОценок пока нет

- Provisioning Behavior of Microfinance InstitutionsДокумент44 страницыProvisioning Behavior of Microfinance InstitutionsngaОценок пока нет

- Dissertation On Non Performing LoansДокумент4 страницыDissertation On Non Performing Loansriteampvendell1979100% (1)

- Talent Ngombe ProposalДокумент14 страницTalent Ngombe ProposalSamson NdhlovuОценок пока нет

- PROPOSALДокумент39 страницPROPOSALAdedeji OluwasamiОценок пока нет

- Thesis On Credit Risk Management in Commercial Banks of NepalДокумент6 страницThesis On Credit Risk Management in Commercial Banks of Nepalabbyjohnsonmanchester100% (2)

- Impact of Borrower Characteristic On Loan Repayment in TanzaniaДокумент30 страницImpact of Borrower Characteristic On Loan Repayment in TanzaniaGift GeorgeОценок пока нет

- 1 s2.0 S187704281500405X Main PDFДокумент8 страниц1 s2.0 S187704281500405X Main PDFafifahfauziyahОценок пока нет

- Sme Credit Risk Modelling in South Africa-A Case StudyДокумент22 страницыSme Credit Risk Modelling in South Africa-A Case StudykatlehoОценок пока нет

- Assessment of Credit Risk Management System (In Case of Dashen Bank Samara Logia Branch)Документ35 страницAssessment of Credit Risk Management System (In Case of Dashen Bank Samara Logia Branch)adinew abey100% (1)

- An Evaluation of Credit Risks Management and PerfoДокумент27 страницAn Evaluation of Credit Risks Management and PerfoOGUNBULE OPEYEMIОценок пока нет

- Impact of Loan by National Commercial Bank On Amwal International Investment CompanyДокумент23 страницыImpact of Loan by National Commercial Bank On Amwal International Investment CompanyJo Anne MirandaОценок пока нет

- An Assessment On Financial Gap of Small and Medium Enterprises of Brunei DarussalamДокумент9 страницAn Assessment On Financial Gap of Small and Medium Enterprises of Brunei DarussalamDanial OthmanОценок пока нет

- Research ProposalДокумент18 страницResearch ProposalSematimba AndrewОценок пока нет

- A Thesis About Analysis of Credit Risk Management in Commercial BanksДокумент8 страницA Thesis About Analysis of Credit Risk Management in Commercial Banksjilllyonstulsa100% (2)

- SSRN Id2704708 PDFДокумент22 страницыSSRN Id2704708 PDFJessica PoligОценок пока нет

- Assignment ArticleДокумент9 страницAssignment Articlemastermind_asia9389Оценок пока нет

- Determinants of Credit Default Risk of Microfinance InstitutionsДокумент9 страницDeterminants of Credit Default Risk of Microfinance InstitutionsgudataaОценок пока нет

- Impact of Credit Management on Liquidity and ProfitabilityДокумент49 страницImpact of Credit Management on Liquidity and ProfitabilityMr. Lawal YusufОценок пока нет

- World Bank SME FinanceДокумент8 страницWorld Bank SME Financepaynow580Оценок пока нет

- Bank Finance For Small and Medium-Sized Enterprises in Sri LankaДокумент12 страницBank Finance For Small and Medium-Sized Enterprises in Sri LankaYuresh NadishanОценок пока нет

- Effect of Credit Risk Management On The Performance of Commercial Banks in Nigeria 1 To 3Документ57 страницEffect of Credit Risk Management On The Performance of Commercial Banks in Nigeria 1 To 3MajestyОценок пока нет

- Thematic Evaluation: Adb Support For SmesДокумент47 страницThematic Evaluation: Adb Support For Smesyuta nakamotoОценок пока нет

- Credit Management PolicyДокумент83 страницыCredit Management PolicyVallabh Utpat100% (1)

- Credit Rationing and Repayment Performance (Problems) in The Case of Ambo Woreda Eshet Microfinance InstitutionДокумент18 страницCredit Rationing and Repayment Performance (Problems) in The Case of Ambo Woreda Eshet Microfinance InstitutionImpact JournalsОценок пока нет

- Bank Loans, Grants & SME PerformanceДокумент13 страницBank Loans, Grants & SME PerformanceAdedeji OluwasamiОценок пока нет

- Empirical Model For Predicting Financial FailureДокумент13 страницEmpirical Model For Predicting Financial FailureMohammed JuveОценок пока нет

- CREDIT RISK AND COMMERCIAL BANKS' PERFORMANCE IN NIGERIA: A PANEL Model APPROACHДокумент8 страницCREDIT RISK AND COMMERCIAL BANKS' PERFORMANCE IN NIGERIA: A PANEL Model APPROACHdarkniightОценок пока нет

- InterpretationNote SME 2012 PDFДокумент6 страницInterpretationNote SME 2012 PDFReza Maulana ArdlyОценок пока нет

- MPRA Paper 72113Документ26 страницMPRA Paper 72113brendan lanzaОценок пока нет

- The Effects of Deposits Mobilization On Financial Performance in Commercial Banks in Rwanda. A Case of Equity Bank Rwanda Limited PDFДокумент28 страницThe Effects of Deposits Mobilization On Financial Performance in Commercial Banks in Rwanda. A Case of Equity Bank Rwanda Limited PDFJohn FrancisОценок пока нет

- Yildirim2013 230529 082700Документ14 страницYildirim2013 230529 082700Vijay ShanigarapuОценок пока нет

- Impact of Credit Risk Management On Bank Performance of Nepalese Commercial BankДокумент8 страницImpact of Credit Risk Management On Bank Performance of Nepalese Commercial BankVivi OktaviaОценок пока нет

- The Small Medium-Free Trade Zone That Able To Acquire DebtДокумент10 страницThe Small Medium-Free Trade Zone That Able To Acquire DebtTest AccountОценок пока нет

- 1 Background To The StudyДокумент4 страницы1 Background To The StudyNagabhushanaОценок пока нет

- Adbi wp583 PDFДокумент29 страницAdbi wp583 PDFArton XheladiniОценок пока нет

- Abstract The Objective of This Study Was To Examine The Factors Influence Credit Rationing by Commercial Banks in KenyaДокумент8 страницAbstract The Objective of This Study Was To Examine The Factors Influence Credit Rationing by Commercial Banks in KenyaMrxОценок пока нет

- Comparative Study of Indian Public, Private and International Banks Project ReportДокумент141 страницаComparative Study of Indian Public, Private and International Banks Project Reportrahulsogani123Оценок пока нет

- Bank Lending and Small and Medium Sized Enterprises - 2022 - Journal of InternatДокумент27 страницBank Lending and Small and Medium Sized Enterprises - 2022 - Journal of InternatM Silahul Mu'minОценок пока нет

- Thesis On Loan DelinquencyДокумент8 страницThesis On Loan Delinquencysjfgexgig100% (2)

- Can Pure Play Internet Banking Survive The Credit CrisisДокумент11 страницCan Pure Play Internet Banking Survive The Credit Crisisngkafai.nkfОценок пока нет

- Credit ManagementДокумент36 страницCredit ManagementMd Kawsar0% (1)

- Capital Buffer, Credit Standards and Financial Performance of Commercial Banks in KenyaДокумент11 страницCapital Buffer, Credit Standards and Financial Performance of Commercial Banks in KenyaInternational Journal of Innovative Science and Research TechnologyОценок пока нет

- Wollo University Final 2014Документ26 страницWollo University Final 2014yonas getachewОценок пока нет

- 1st JournalДокумент15 страниц1st JournalOffiaОценок пока нет

- 7 Factors Affecting Loan RepaymentДокумент10 страниц7 Factors Affecting Loan Repaymentendeshaw yibetalОценок пока нет

- The Total Number of Smes in Bangladesh Is Estimated To Be 79,00,000 Establishments. of Them, 93.6 Percent Are Small and 6.4 Percent Are MediumДокумент23 страницыThe Total Number of Smes in Bangladesh Is Estimated To Be 79,00,000 Establishments. of Them, 93.6 Percent Are Small and 6.4 Percent Are MediumSamia AkterОценок пока нет

- Determinants of Loan Repayment The CaseДокумент16 страницDeterminants of Loan Repayment The Casebisrat.redaОценок пока нет

- EIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptОт EverandEIB Working Papers 2019/10 - Structural and cyclical determinants of access to finance: Evidence from EgyptОценок пока нет

- EIB Working Papers 2019/07 - What firms don't like about bank loans: New evidence from survey dataОт EverandEIB Working Papers 2019/07 - What firms don't like about bank loans: New evidence from survey dataОценок пока нет

- Lord Shivas Paradise - Ace Paint Service AgreementДокумент7 страницLord Shivas Paradise - Ace Paint Service Agreementkkundan52Оценок пока нет

- Role of Coopertives in Infrastructure DevelopmentДокумент51 страницаRole of Coopertives in Infrastructure Developmentkkundan52Оценок пока нет

- Handbook On Cooperative Society - CCONPOДокумент15 страницHandbook On Cooperative Society - CCONPOkkundan52Оценок пока нет

- Lord Shivas Paradise - Ace Paint Service AgreementДокумент7 страницLord Shivas Paradise - Ace Paint Service Agreementkkundan52Оценок пока нет

- Cooperative Society Procedures Checklists in EnglishДокумент5 страницCooperative Society Procedures Checklists in Englishkkundan52Оценок пока нет

- Co-operative Societies Regulations SummaryДокумент31 страницаCo-operative Societies Regulations Summarykkundan52Оценок пока нет

- Application Form Cooperative Society For PrintoutДокумент8 страницApplication Form Cooperative Society For Printoutkkundan52Оценок пока нет

- PAINT WORKS Pornima Society-1Документ3 страницыPAINT WORKS Pornima Society-1kkundan52Оценок пока нет

- Vitthal Plaza Phase 2 Revised APДокумент5 страницVitthal Plaza Phase 2 Revised APkkundan52Оценок пока нет

- Tax Invoice: "Natural Aqua 250 ML" "Natural Aqua 500 ML" "Natural Aqua 1 LIT" "Natural Aqua 2 LIT"Документ9 страницTax Invoice: "Natural Aqua 250 ML" "Natural Aqua 500 ML" "Natural Aqua 1 LIT" "Natural Aqua 2 LIT"kkundan52Оценок пока нет

- Quotation of CCTV Work CP Plus - With CasingДокумент1 страницаQuotation of CCTV Work CP Plus - With Casingkkundan52Оценок пока нет

- Seven Forty Six Solutions: Interiors & Everything in BetweenДокумент1 страницаSeven Forty Six Solutions: Interiors & Everything in Betweenkkundan52Оценок пока нет

- Adhivas Homes: 202, Vaibhav Apartment, Opposite Kasturi Plaza, Dombivli EastДокумент1 страницаAdhivas Homes: 202, Vaibhav Apartment, Opposite Kasturi Plaza, Dombivli Eastkkundan52Оценок пока нет

- Home painting service quotation from NoBroker TechnologiesДокумент1 страницаHome painting service quotation from NoBroker Technologieskkundan52Оценок пока нет

- Tileup Sidharth JadhavДокумент2 страницыTileup Sidharth Jadhavkkundan52Оценок пока нет

- Patel Retial Margin On MRP in % Patel Retail Landing RateДокумент1 страницаPatel Retial Margin On MRP in % Patel Retail Landing Ratekkundan52Оценок пока нет

- Seven Forty Six Solutions: Interiors & Everything in BetweenДокумент1 страницаSeven Forty Six Solutions: Interiors & Everything in Betweenkkundan52Оценок пока нет

- The Arch Panchanand CHSДокумент5 страницThe Arch Panchanand CHSkkundan52Оценок пока нет

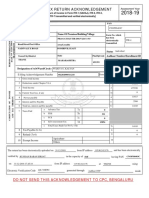

- Indian Income Tax Return Acknowledgement: Name of Premises/Building/VillageДокумент1 страницаIndian Income Tax Return Acknowledgement: Name of Premises/Building/Villagekkundan52Оценок пока нет

- BOQ For Electrical WorksДокумент2 страницыBOQ For Electrical Workskkundan52Оценок пока нет

- Dr. Fixit Flexicoat PU: Single Component, Cold Applied, Elastomeric Waterproofing Membrane CoatingДокумент4 страницыDr. Fixit Flexicoat PU: Single Component, Cold Applied, Elastomeric Waterproofing Membrane Coatingkkundan52Оценок пока нет

- Oriental Insurance Motor Insurance CertificateДокумент3 страницыOriental Insurance Motor Insurance Certificatekkundan52Оценок пока нет

- To, Mr. Sanghpal Baban SirsatДокумент1 страницаTo, Mr. Sanghpal Baban Sirsatkkundan52Оценок пока нет

- Reassurance at Every Step: Keeps Giving You More!Документ6 страницReassurance at Every Step: Keeps Giving You More!Anonymous RRTE5WbОценок пока нет

- GST 18 % Plan Details HathwayДокумент5 страницGST 18 % Plan Details Hathwaykkundan52Оценок пока нет

- Adhivas Ravi RautДокумент2 страницыAdhivas Ravi Rautkkundan52Оценок пока нет

- LOD - BajajДокумент2 страницыLOD - Bajajkkundan52Оценок пока нет

- Aishwarya Food Production - 274Документ1 страницаAishwarya Food Production - 274kkundan52Оценок пока нет

- 604 Dr. Fixit PrimesealДокумент2 страницы604 Dr. Fixit Primesealkkundan52Оценок пока нет

- Adhivas Homes: All Types of Civil Works, Waterproofing & Painting WorksДокумент6 страницAdhivas Homes: All Types of Civil Works, Waterproofing & Painting Workskkundan52Оценок пока нет

- Grade 7 Week 3 Las 2Документ2 страницыGrade 7 Week 3 Las 2MONHANNAH RAMADEAH LIMBUTUNGANОценок пока нет

- Reviewing ArticlesДокумент15 страницReviewing ArticlesZebene HaileselassieОценок пока нет

- Mathematics 8 Analytic Rubric - Statistics and Probability Criteria Excellent 4 Very Good 3 Good 2 Needs Improvement 1Документ2 страницыMathematics 8 Analytic Rubric - Statistics and Probability Criteria Excellent 4 Very Good 3 Good 2 Needs Improvement 1Melissa LouiseОценок пока нет

- Alford - The Craft of InquiryДокумент12 страницAlford - The Craft of InquiryAnonymous 2Dl0cn7Оценок пока нет

- Introduction To Statistical Methods For Financial ModelsДокумент387 страницIntroduction To Statistical Methods For Financial ModelsBrookОценок пока нет

- Random Motors Project Submission: Name - Rohith MuralidharanДокумент10 страницRandom Motors Project Submission: Name - Rohith MuralidharanRohith muralidharanОценок пока нет

- The Relationship Between The Readiness of Knowledge and Teachers' Attitudes Towards Students With Dyslexic Characteristics in Mainstream SchoolsДокумент19 страницThe Relationship Between The Readiness of Knowledge and Teachers' Attitudes Towards Students With Dyslexic Characteristics in Mainstream SchoolsThana Letchumi ThirrajaОценок пока нет

- Mathematics in The Modern WorldДокумент88 страницMathematics in The Modern WorldRanzel Serenio100% (5)

- Quiz 6: CS 436/536: Introduction To Machine LearningДокумент2 страницыQuiz 6: CS 436/536: Introduction To Machine LearningKarishma JaniОценок пока нет

- Positivism and Knowledge Inquiry From Scientific Method To Media and Communication Researc PDFДокумент9 страницPositivism and Knowledge Inquiry From Scientific Method To Media and Communication Researc PDFShubhankar BasuОценок пока нет

- Statistics in Analytical ChemistryДокумент2 страницыStatistics in Analytical ChemistryHelder DuraoОценок пока нет

- Mathematical Modeling Using Linear RegresionДокумент52 страницыMathematical Modeling Using Linear RegresionIrinel IonutОценок пока нет

- Tutorial 7Документ3 страницыTutorial 7Nur Arisya AinaaОценок пока нет

- Reaserch MethodДокумент27 страницReaserch MethodtadesseОценок пока нет

- MpaДокумент2 страницыMpaMCPS Operations BranchОценок пока нет

- The Normal Distribution Estimation CorrelationДокумент16 страницThe Normal Distribution Estimation Correlationjhamlene2528Оценок пока нет

- Unit 1 Quiz ResultsДокумент10 страницUnit 1 Quiz ResultsBelle SaenyeaОценок пока нет

- Probable Error of a MeanДокумент24 страницыProbable Error of a MeanMartin McflinОценок пока нет

- Pembagian tugas menerjemah buku ProbstatДокумент3 страницыPembagian tugas menerjemah buku Probstatega putriОценок пока нет

- SOC CourseDesc WEBДокумент14 страницSOC CourseDesc WEBAlmeda AsuncionОценок пока нет

- Elements of A Research Proposal and ReportДокумент8 страницElements of A Research Proposal and Reportapi-19661801Оценок пока нет

- Output 6 - StatДокумент2 страницыOutput 6 - StatPhebe Lagutao0% (1)

- ICT 726 Research Methods Exam p1 Question PaperДокумент2 страницыICT 726 Research Methods Exam p1 Question Paperkimwatusteve100% (1)

- Chapter 3 ForecastingДокумент87 страницChapter 3 ForecastingTabassum BushraОценок пока нет

- Basic Concepts of The Poisson ProcessДокумент8 страницBasic Concepts of The Poisson ProcessQurban khaton HussainyarОценок пока нет

- Lecture 11 Forecasting Methods QMДокумент7 страницLecture 11 Forecasting Methods QMNella KingОценок пока нет

- Problem Set 8Документ3 страницыProblem Set 8JonahJunior0% (1)

- Probability Modified PDFДокумент23 страницыProbability Modified PDFIMdad HaqueОценок пока нет

- US3 Performance Stability Tips Tricks and UnderscoresДокумент167 страницUS3 Performance Stability Tips Tricks and UnderscoreslocutoОценок пока нет

- Census Income ProjectДокумент4 страницыCensus Income ProjectAmit PhulwaniОценок пока нет