Вам также может понравиться

- Chapter 3 DiscussionsДокумент22 страницыChapter 3 Discussionsの変化 ナザレОценок пока нет

- Assignment 2Документ14 страницAssignment 2Bryent GawОценок пока нет

- Lesson Guide 2.2 Beware of Banking FeesДокумент4 страницыLesson Guide 2.2 Beware of Banking FeesKent TiclavilcaОценок пока нет

- Mayes 8e CH03 Problem SetДокумент8 страницMayes 8e CH03 Problem SetBunga Mega WangiОценок пока нет

- Chapter 03 Ratio AnalysisДокумент46 страницChapter 03 Ratio AnalysisMustakim Bin Aziz 1610534630Оценок пока нет

- Financial Ratio AnalysisДокумент34 страницыFinancial Ratio AnalysisamahaktОценок пока нет

- Facc 099 Content SheetДокумент14 страницFacc 099 Content SheetUfuoma OkwuraiweОценок пока нет

- Chapter 2 NotesДокумент6 страницChapter 2 NotesSurelis AcostaОценок пока нет

- Financial Statement AnalysisДокумент48 страницFinancial Statement AnalysisCheryl LowОценок пока нет

- Use The Following Information To Answer Items 5 - 7Документ4 страницыUse The Following Information To Answer Items 5 - 7acctg2012Оценок пока нет

- Creating A Successful Financial Plan Chapter 11Документ39 страницCreating A Successful Financial Plan Chapter 11Taseen AhmeedОценок пока нет

- Assignment NO 1 POFДокумент15 страницAssignment NO 1 POFMuhammad AsimОценок пока нет

- Tutorial 6 With Solutions-Long-Term Debt-Paying Ability and ProfitabilityДокумент5 страницTutorial 6 With Solutions-Long-Term Debt-Paying Ability and ProfitabilityGing freexОценок пока нет

- C5B Profitability AnalysisДокумент6 страницC5B Profitability AnalysisSteeeeeeeephОценок пока нет

- Financial Statement AnalysisДокумент31 страницаFinancial Statement AnalysisbilalahmedbhuttoОценок пока нет

- Fundamentals of Accounting: Interpretation of Financial StatementsДокумент44 страницыFundamentals of Accounting: Interpretation of Financial Statementscons theОценок пока нет

- Chapter 1 NotesДокумент7 страницChapter 1 NotesSurelis AcostaОценок пока нет

- CHAPTER TWO FM Mgt-1Документ18 страницCHAPTER TWO FM Mgt-1Belex Man100% (1)

- Lecture Practice QuestionsДокумент5 страницLecture Practice QuestionsMariøn Lemonnier BruelОценок пока нет

- Financial StatementsДокумент23 страницыFinancial StatementsShin Shan JeonОценок пока нет

- Handout 7 - Business FinanceДокумент3 страницыHandout 7 - Business FinanceCeage SJОценок пока нет

- Problem Set 6 BS CS 6Документ3 страницыProblem Set 6 BS CS 6Rubab MirzaОценок пока нет

- RATIO Practice QuestionsДокумент14 страницRATIO Practice Questionspranay raj rathoreОценок пока нет

- CHAPTER II - Financial Analysis and PlanningДокумент84 страницыCHAPTER II - Financial Analysis and PlanningTamiratОценок пока нет

- Brewer Chapter 14 Alt ProbДокумент8 страницBrewer Chapter 14 Alt ProbAtif RehmanОценок пока нет

- Chapter TwoДокумент16 страницChapter TwoHananОценок пока нет

- Financial Statements and Ratio AnalysisДокумент26 страницFinancial Statements and Ratio Analysismary jean giananОценок пока нет

- Ratio Analysis Chapter 9Документ5 страницRatio Analysis Chapter 9natefir719Оценок пока нет

- Chapter 6 (CF)Документ51 страницаChapter 6 (CF)Hossain BelalОценок пока нет

- CH03 ProblemДокумент3 страницыCH03 Problemtrangtran01010Оценок пока нет

- Finance Assignment File 1 SolvedДокумент5 страницFinance Assignment File 1 SolvedIQRAsummers 2021Оценок пока нет

- FM AssignmentДокумент7 страницFM Assignmentkartika tamara maharaniОценок пока нет

- Tutorial Solutions ACCT1501Документ24 страницыTutorial Solutions ACCT1501Samuēl BeedhamОценок пока нет

- Problem: 1Документ8 страницProblem: 1PRIYA SHARMA EPGDIB (On Campus) 2019-20Оценок пока нет

- CH-2 Advanced Financial MGTДокумент60 страницCH-2 Advanced Financial MGTMusxii TemamОценок пока нет

- Basic Accounting: Concepts, Techniques, Conventions. Read and Interpret The Basic Financial StatementsДокумент42 страницыBasic Accounting: Concepts, Techniques, Conventions. Read and Interpret The Basic Financial StatementsATORNIIIОценок пока нет

- Learning Activity 1 - Analysis of Financial StatementsДокумент3 страницыLearning Activity 1 - Analysis of Financial StatementsAra Joyce PermalinoОценок пока нет

- Financial Statement AnalysisДокумент14 страницFinancial Statement AnalysisMuhammad YasinОценок пока нет

- Financial Statements and Ratio AnalysisДокумент9 страницFinancial Statements and Ratio AnalysisRabie HarounОценок пока нет

- CHAPTER II - Financial Analysis and PlanningДокумент84 страницыCHAPTER II - Financial Analysis and PlanningMan TKОценок пока нет

- For Lecturers - Interpretation of FS - Ratio Analysis - Example, Exercises, SolutionsДокумент13 страницFor Lecturers - Interpretation of FS - Ratio Analysis - Example, Exercises, SolutionsdimniousОценок пока нет

- Financial Statement Analysis - RatioДокумент7 страницFinancial Statement Analysis - RatioJanelle De TorresОценок пока нет

- Chapter 2 - Evaluating A Firm's Financial Performance: 2005, Pearson Prentice HallДокумент47 страницChapter 2 - Evaluating A Firm's Financial Performance: 2005, Pearson Prentice HallNur SyakirahОценок пока нет

- New Financial Management Chapter LastДокумент18 страницNew Financial Management Chapter LastbikilahussenОценок пока нет

- How To Read Financial Statement PDFДокумент31 страницаHow To Read Financial Statement PDFMazen AlbsharaОценок пока нет

- Financial Statement AnalysisДокумент6 страницFinancial Statement AnalysisEmmanuel PenullarОценок пока нет

- Financial Ratio Analysis Case StudyДокумент10 страницFinancial Ratio Analysis Case StudyGracel Joy VicenteОценок пока нет

- Financial Statements Analysis - Ratio AnalysisДокумент44 страницыFinancial Statements Analysis - Ratio AnalysisDipanjan SenguptaОценок пока нет

- Lecture 3 Ratio AnalysisДокумент59 страницLecture 3 Ratio AnalysisJiun Herng LeeОценок пока нет

- FM in Construction 2Документ23 страницыFM in Construction 2YosiОценок пока нет

- 6 - Cash Flow Statement PDFДокумент30 страниц6 - Cash Flow Statement PDFJohn Paul CristobalОценок пока нет

- BBMF2813 Extra Notes Topic 2 RatiosДокумент10 страницBBMF2813 Extra Notes Topic 2 RatiosFred LeletОценок пока нет

- For Students - Interpretation of FS - Ratio Analysis - Example, ExercisesДокумент10 страницFor Students - Interpretation of FS - Ratio Analysis - Example, ExercisesdimniousОценок пока нет

- Week 1 621 NotesДокумент6 страницWeek 1 621 NotesSameera VithanaОценок пока нет

- FM II Ch-3Документ9 страницFM II Ch-3mearghaile4Оценок пока нет

- Unit 2 Financial AnalysisДокумент12 страницUnit 2 Financial AnalysisGizaw BelayОценок пока нет

- FM One - Ch2Документ15 страницFM One - Ch2Tsegay ArayaОценок пока нет

- Financial Statements and AnalysisДокумент48 страницFinancial Statements and AnalysiskEBAY100% (1)

- Financial Accounting Review (Week 1) : Income Statement and Balance Sheet Depreciation Gains and LossesДокумент7 страницFinancial Accounting Review (Week 1) : Income Statement and Balance Sheet Depreciation Gains and LossesAndy MoralesОценок пока нет

- Working Lecture 7Документ17 страницWorking Lecture 7Sara KarenОценок пока нет

- Business Metrics and Tools; Reference for Professionals and StudentsОт EverandBusiness Metrics and Tools; Reference for Professionals and StudentsОценок пока нет

- Accounting Equation Questions For PracticeДокумент3 страницыAccounting Equation Questions For Practiceashishdbg2008Оценок пока нет

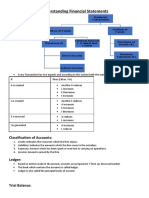

- Understanding Financial Statements: Classification of AccountsДокумент3 страницыUnderstanding Financial Statements: Classification of Accountsashishdbg2008Оценок пока нет

- Cash Flow Statements: Needs of The Enterprise To Utilize Those Cash FlowsДокумент1 страницаCash Flow Statements: Needs of The Enterprise To Utilize Those Cash Flowsashishdbg2008Оценок пока нет

- Basic Cost Concepts: Cost - Volume - Profit (CVP) AnalysisДокумент2 страницыBasic Cost Concepts: Cost - Volume - Profit (CVP) Analysisashishdbg2008Оценок пока нет

- Executive SummaryДокумент3 страницыExecutive SummaryyogeshramachandraОценок пока нет

- English PresentationДокумент6 страницEnglish Presentationberatmete26Оценок пока нет

- Journal 6 (Current Account Deficit) PDFДокумент24 страницыJournal 6 (Current Account Deficit) PDFdaniswara 2Оценок пока нет

- Islam PPT Outline (Script)Документ2 страницыIslam PPT Outline (Script)Paulene MaeОценок пока нет

- 2016-2019 Sip MinutesДокумент2 страницы2016-2019 Sip Minutesloraine mandapОценок пока нет

- Syllabus 2640Документ4 страницыSyllabus 2640api-360768481Оценок пока нет

- Formulating Natural ProductsДокумент56 страницFormulating Natural ProductsRajeswari Raji92% (25)

- Solidcam Glodanje Vjezbe Ivo SladeДокумент118 страницSolidcam Glodanje Vjezbe Ivo SladeGoran BertoОценок пока нет

- Example of Scholarship EssayДокумент4 страницыExample of Scholarship EssayertzyzbafОценок пока нет

- Contemporaries of ChaucerДокумент3 страницыContemporaries of ChaucerGarret RajaОценок пока нет

- Encouragement 101 Per DevДокумент14 страницEncouragement 101 Per DevKaye Ortega Navales Tañales50% (2)

- Shaykh Rabee Advises Before He RefutesДокумент7 страницShaykh Rabee Advises Before He Refuteshttp://AbdurRahman.orgОценок пока нет

- 71english Words of Indian OriginДокумент4 страницы71english Words of Indian Originshyam_naren_1Оценок пока нет

- Journey of The Company:: Carlyle Group Completes 10 % Exit in SBI Card Through IPOДокумент3 страницыJourney of The Company:: Carlyle Group Completes 10 % Exit in SBI Card Through IPOJayash KaushalОценок пока нет

- ASA Basic Initial ConfigurationДокумент3 страницыASA Basic Initial ConfigurationDeepak KardamОценок пока нет

- Final Examinations Labor LawДокумент1 страницаFinal Examinations Labor LawAtty. Kristina de VeraОценок пока нет

- User Manual For State ExciseДокумент29 страницUser Manual For State ExciserotastrainОценок пока нет

- Quo Vadis PhilippinesДокумент26 страницQuo Vadis PhilippineskleomarloОценок пока нет

- YSI Saving 2022Документ2 страницыYSI Saving 2022koamanoОценок пока нет

- Claire Churchwell - rhetORICALДокумент7 страницClaire Churchwell - rhetORICALchurchcpОценок пока нет

- Metaswitch Datasheet Perimeta SBC OverviewДокумент2 страницыMetaswitch Datasheet Perimeta SBC OverviewblitoОценок пока нет

- Court of Appeals Order AffirmingДокумент16 страницCourt of Appeals Order AffirmingLisa AutryОценок пока нет

- Invoice: Issue Date Due DateДокумент2 страницыInvoice: Issue Date Due DateCheikh Ahmed Tidiane GUEYEОценок пока нет

- Panel Hospital ListДокумент4 страницыPanel Hospital ListNoman_Saeed_1520100% (1)

- Globalization DesglobalizationДокумент10 страницGlobalization DesglobalizationFarhadОценок пока нет

- We Wish You A Merry Christmas Harp PDFДокумент4 страницыWe Wish You A Merry Christmas Harp PDFCleiton XavierОценок пока нет

- Jurisprudence Renaissance Law College NotesДокумент49 страницJurisprudence Renaissance Law College Notesdivam jainОценок пока нет

- Additional English - 4th Semester FullДокумент48 страницAdditional English - 4th Semester FullanuОценок пока нет