Вам также может понравиться

- Accepted For Value Tutorial 2018Документ7 страницAccepted For Value Tutorial 2018Pratus Williams100% (17)

- Consignment Sales 2Документ22 страницыConsignment Sales 2Mhelka Tiodianco33% (3)

- Afar QuestionsДокумент16 страницAfar QuestionsJessarene Fauni Depante50% (18)

- A. THEORY. Letter Choices On The Date Column of Your WorksheetДокумент7 страницA. THEORY. Letter Choices On The Date Column of Your WorksheetAngel Alejo Acoba0% (2)

- Module 10 Accounting For Build-Operate-TransferДокумент3 страницыModule 10 Accounting For Build-Operate-TransferSunshine Khuletz0% (1)

- Andrix Asterix Co. Statement of Financial Position As of December 31, 20x0Документ8 страницAndrix Asterix Co. Statement of Financial Position As of December 31, 20x0aleachon100% (3)

- This Study Resource WasДокумент3 страницыThis Study Resource WasQueeny Mae Cantre ReutaОценок пока нет

- Joint Arrangement Quiz AnswersДокумент7 страницJoint Arrangement Quiz AnswersAlexandrite100% (1)

- LTCC and Franchise Long Exam PDFДокумент9 страницLTCC and Franchise Long Exam PDFChristine Joy Original50% (2)

- Chapter 10 - Teacher's Manual - Afar Part 1Документ20 страницChapter 10 - Teacher's Manual - Afar Part 1Angelic67% (3)

- OrДокумент10 страницOrasdf100% (1)

- AFAR Questions With AnswersДокумент11 страницAFAR Questions With AnswersAngelica CerioОценок пока нет

- Quiz 7: Use The Following Information For Questions 4 To 6Документ9 страницQuiz 7: Use The Following Information For Questions 4 To 6Tricia Mae Fernandez100% (2)

- QUIZ - CHAPTER 8 - ACCOUNTING FOR FRANCHISE OPERATIONS FRANCHISOR NoaДокумент3 страницыQUIZ - CHAPTER 8 - ACCOUNTING FOR FRANCHISE OPERATIONS FRANCHISOR NoaNeirish fainsan43% (7)

- Module 8 - Home Office, Branch and Agency AccountingДокумент8 страницModule 8 - Home Office, Branch and Agency AccountingSunshine Khuletz67% (3)

- Millan ConsignmentДокумент5 страницMillan Consignmenttonyalmon0% (1)

- Midterm Exam-Advacctgii 2Nd Sem 2011-2012Документ18 страницMidterm Exam-Advacctgii 2Nd Sem 2011-2012Allie LinОценок пока нет

- Activity For Finals TermДокумент6 страницActivity For Finals TermRhegee Irene RosarioОценок пока нет

- MSQ-02 - Variable & Absorption Costing (Final)Документ11 страницMSQ-02 - Variable & Absorption Costing (Final)Kevin James Sedurifa OledanОценок пока нет

- BBAA - Shareholders AgreementДокумент43 страницыBBAA - Shareholders AgreementArvel DomingoОценок пока нет

- LTCCДокумент7 страницLTCCGenesis Dizon67% (6)

- Cebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsДокумент13 страницCebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsPrima Facie50% (2)

- Notes For Advanced AccountingДокумент5 страницNotes For Advanced AccountingSoleil Sierra0% (1)

- AFAR - Revenue Recognition 2019Документ4 страницыAFAR - Revenue Recognition 2019Joanna Rose DeciarОценок пока нет

- Buss. Combi PrelimДокумент8 страницBuss. Combi PrelimPhia TeoОценок пока нет

- Consignment Sales: Name: Date: Professor: Section: Score: QuizДокумент3 страницыConsignment Sales: Name: Date: Professor: Section: Score: QuizAndrea Florence Guy VidalОценок пока нет

- LTCCДокумент7 страницLTCCgenevieve sicatОценок пока нет

- Grace-AST Module 10Документ5 страницGrace-AST Module 10Devine Grace A. MaghinayОценок пока нет

- Business Combination ExerciseДокумент5 страницBusiness Combination Exercise수지Оценок пока нет

- 07 Installment SalesДокумент1 страница07 Installment SalesGem Yiel33% (3)

- Quiz 2 Joint ArrangementsДокумент4 страницыQuiz 2 Joint ArrangementsJane Gavino100% (2)

- p1 Quiz With TheoryДокумент15 страницp1 Quiz With TheoryGrace CorpoОценок пока нет

- Chapter 9 Teachers Manual Afar Part 1Документ9 страницChapter 9 Teachers Manual Afar Part 1Aimee Diaz100% (3)

- Name: Date: Professor: Section: Score: Assynchronous Activity-Final TermДокумент14 страницName: Date: Professor: Section: Score: Assynchronous Activity-Final TermkmarisseeОценок пока нет

- Afar 2 Module CH 4 PDFДокумент20 страницAfar 2 Module CH 4 PDFRazmen Ramirez PintoОценок пока нет

- Chapter 7 - Teacher's Manual - Afar Part 1Документ24 страницыChapter 7 - Teacher's Manual - Afar Part 1Angelic100% (3)

- Enabling Assessment: (Note: Several Ted Suavillo Cases)Документ2 страницыEnabling Assessment: (Note: Several Ted Suavillo Cases)Von Andrei MedinaОценок пока нет

- AFAR - Installment, Customer, ConsignmentДокумент3 страницыAFAR - Installment, Customer, ConsignmentJoanna Rose DeciarОценок пока нет

- PDF Valle Quiz ABC CompressДокумент6 страницPDF Valle Quiz ABC CompressPotie RhymeszОценок пока нет

- Use The Following Information For The Next Two QuestionsДокумент59 страницUse The Following Information For The Next Two QuestionsAllecks Juel LuchanaОценок пока нет

- Chapter 5 - Teacher's Manual - Afar Part 1Документ15 страницChapter 5 - Teacher's Manual - Afar Part 1Mayeth BotinОценок пока нет

- Use The Following Information For The Next Two Questions:: Practice Set # 6: Joint ArrangementsДокумент4 страницыUse The Following Information For The Next Two Questions:: Practice Set # 6: Joint ArrangementsRey Joyce Abuel0% (1)

- MODULE 5: Accounting For Franchise Operations - Franchisor: RequirementsДокумент2 страницыMODULE 5: Accounting For Franchise Operations - Franchisor: RequirementsDevine Grace A. Maghinay67% (3)

- HO, B & A AcctgДокумент15 страницHO, B & A AcctgCarolina Fortez Dacanay71% (7)

- Activity 1Документ4 страницыActivity 1Fernando III PerezОценок пока нет

- Sample ProblemsДокумент3 страницыSample ProblemsGracias100% (1)

- This Study Resource Was: Chapter 13 Multiple ChoicesДокумент6 страницThis Study Resource Was: Chapter 13 Multiple ChoicesChris Jay LatibanОценок пока нет

- The Joint Arrangement Provided For The Division of Gains and Losses Among AДокумент1 страницаThe Joint Arrangement Provided For The Division of Gains and Losses Among Aelsana philip100% (1)

- Corporate Liquidation Quiz 5docxДокумент5 страницCorporate Liquidation Quiz 5docxAngelica Duarte33% (6)

- Chapter 7Документ18 страницChapter 7Yenelyn Apistar CambarijanОценок пока нет

- Corporation LiquidationДокумент2 страницыCorporation LiquidationPatrishaОценок пока нет

- Quiz 3 Construction ContractsДокумент7 страницQuiz 3 Construction ContractsMarinel Mae Chica100% (2)

- Accounting For Special Transaction Final ReviewerДокумент73 страницыAccounting For Special Transaction Final ReviewerLunaОценок пока нет

- Accounting For Special Transactions - Franchise AccountingДокумент18 страницAccounting For Special Transactions - Franchise AccountingDewdrop Mae RafananОценок пока нет

- MODAUD2 Unit 10 Audit of Revenues T31516Документ6 страницMODAUD2 Unit 10 Audit of Revenues T31516mimi96Оценок пока нет

- Franchise IFRS 15 2020Документ13 страницFranchise IFRS 15 2020Divine Victoria100% (1)

- Prelec Post TestДокумент3 страницыPrelec Post TestPrince PierreОценок пока нет

- Quiz No. 3Документ4 страницыQuiz No. 3abbyОценок пока нет

- Advance Financial Accounting and Reporting: Franchise IAS 18Документ4 страницыAdvance Financial Accounting and Reporting: Franchise IAS 18Roxell CaibogОценок пока нет

- Auction: SampleДокумент6 страницAuction: SampleOctavian CiceuОценок пока нет

- Reviewer in Revenue and Expense RecognitionДокумент7 страницReviewer in Revenue and Expense RecognitionPaupauОценок пока нет

- Afar302 A - FranchisingДокумент3 страницыAfar302 A - FranchisingNicole TeruelОценок пока нет

- QUIZ #4 (Chapters 5, 7 & 8)Документ10 страницQUIZ #4 (Chapters 5, 7 & 8)Rochelle BuensucesoОценок пока нет

- Week 5. Religious Involvement Question: How Well Did You Participate in The Religious Activities of Your Church This WeekДокумент1 страницаWeek 5. Religious Involvement Question: How Well Did You Participate in The Religious Activities of Your Church This WeekSoleil SierraОценок пока нет

- Question: How Well Did You Participate in The Religious Activities of Your Church This WeekДокумент1 страницаQuestion: How Well Did You Participate in The Religious Activities of Your Church This WeekSoleil SierraОценок пока нет

- Contract of Agency ExercisesДокумент17 страницContract of Agency ExercisesFernando III PerezОценок пока нет

- BL Suarez Pauline S. Munoz Princess Joy G. Talo Jonathan G. GimongalaДокумент330 страницBL Suarez Pauline S. Munoz Princess Joy G. Talo Jonathan G. GimongalaSoleil SierraОценок пока нет

- Law On ObliCon and ParCorДокумент50 страницLaw On ObliCon and ParCorSoleil SierraОценок пока нет

- Question: How Well Did You Participate in The Religious Activities of Your Church This WeekДокумент1 страницаQuestion: How Well Did You Participate in The Religious Activities of Your Church This WeekSoleil SierraОценок пока нет

- Moral ReasoningДокумент1 страницаMoral ReasoningSoleil Sierra0% (2)

- Productions and Operations NotesДокумент1 страницаProductions and Operations NotesSoleil SierraОценок пока нет

- Question: How Well Did You Participate in The Religious Activities of Your Church This WeekДокумент1 страницаQuestion: How Well Did You Participate in The Religious Activities of Your Church This WeekSoleil SierraОценок пока нет

- Bentham or Mill Philo NotesДокумент1 страницаBentham or Mill Philo NotesSoleil SierraОценок пока нет

- Comprehensive Strategic Plan: Proposed byДокумент6 страницComprehensive Strategic Plan: Proposed bySoleil SierraОценок пока нет

- Bentham Notes PhiloДокумент1 страницаBentham Notes PhiloSoleil SierraОценок пока нет

- Subordinate Rules EthicsДокумент1 страницаSubordinate Rules EthicsSoleil SierraОценок пока нет

- Notes AccountingДокумент5 страницNotes AccountingSoleil SierraОценок пока нет

- Utilitarianism NotesДокумент1 страницаUtilitarianism NotesSoleil SierraОценок пока нет

- Productions and Operations NotesДокумент1 страницаProductions and Operations NotesSoleil SierraОценок пока нет

- Bank A and B - Bank XДокумент4 страницыBank A and B - Bank XSoleil SierraОценок пока нет

- Manpower and MachinesДокумент3 страницыManpower and MachinesSoleil SierraОценок пока нет

- Lawrence Kohlberg Moral DevelopmentДокумент3 страницыLawrence Kohlberg Moral DevelopmentSoleil SierraОценок пока нет

- Personal PhilosophyДокумент1 страницаPersonal PhilosophySoleil SierraОценок пока нет

- Time Stamp of VideosДокумент2 страницыTime Stamp of VideosSoleil SierraОценок пока нет

- Essay of Unique CultureДокумент1 страницаEssay of Unique CultureSoleil SierraОценок пока нет

- Category of NeedsДокумент1 страницаCategory of NeedsSoleil SierraОценок пока нет

- Sample Storyboard For Film MakingДокумент3 страницыSample Storyboard For Film MakingSoleil SierraОценок пока нет

- Bad Culture of IlocanoДокумент1 страницаBad Culture of IlocanoSoleil SierraОценок пока нет

- Reflection PaperДокумент2 страницыReflection PaperSoleil SierraОценок пока нет

- Journal For NSTPДокумент1 страницаJournal For NSTPSoleil SierraОценок пока нет

- Econ Quiz 5Документ3 страницыEcon Quiz 5Soleil SierraОценок пока нет

- A Case Study of A 23 Year Old Woman With Ewing's SarcomaДокумент2 страницыA Case Study of A 23 Year Old Woman With Ewing's SarcomaSoleil SierraОценок пока нет

- واقع البدائل الشرعية للمشتقـات الماليـة في ضوء منتجات الهندسة المالية الإسلامية The Reality of Legitimacy Alternatives of financial Derivatives in the Light of the Islamic Financial Engineering ProductsДокумент33 страницыواقع البدائل الشرعية للمشتقـات الماليـة في ضوء منتجات الهندسة المالية الإسلامية The Reality of Legitimacy Alternatives of financial Derivatives in the Light of the Islamic Financial Engineering ProductsČriştä Állin0% (1)

- Pacific Wide Realty and DevДокумент2 страницыPacific Wide Realty and DevJohn Roel VillaruzОценок пока нет

- Puertos - Case Digest Second ExamДокумент14 страницPuertos - Case Digest Second ExamTim PuertosОценок пока нет

- Depository Trust and Clearing CorpДокумент3 страницыDepository Trust and Clearing CorpMarketsWikiОценок пока нет

- Mortgage Lecture NotesДокумент3 страницыMortgage Lecture NotesLuh CheeseОценок пока нет

- Promissory NoteДокумент6 страницPromissory NoteJames HumphreysОценок пока нет

- Bài tập Unit 4Документ8 страницBài tập Unit 4Thắng Trần LêОценок пока нет

- Kinds of Contract of SaleДокумент8 страницKinds of Contract of SaleJoyceОценок пока нет

- Should The Builder Finance Construction - The Mortgage ProfessorДокумент1 страницаShould The Builder Finance Construction - The Mortgage ProfessorJericFuentesОценок пока нет

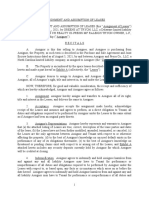

- Form - Assignment and Assumption of LeasesДокумент4 страницыForm - Assignment and Assumption of Leasesholly millsОценок пока нет

- Sap2000 Egitim 2 GKTДокумент32 страницыSap2000 Egitim 2 GKTAlp KuzubasiogluОценок пока нет

- Banking Regulation Act-1949 RBI Act-1934 Negotiable Instrument Act-1881Документ7 страницBanking Regulation Act-1949 RBI Act-1934 Negotiable Instrument Act-1881Ashraf AliОценок пока нет

- Notes On Law On PartnershipДокумент19 страницNotes On Law On PartnershipUlaine Gayle Esnara0% (1)

- Law Bachawat Scanner ICAДокумент100 страницLaw Bachawat Scanner ICAgvramani51233Оценок пока нет

- RFBT Answer Key Drill - 2020 RДокумент4 страницыRFBT Answer Key Drill - 2020 RPhoeza Espinosa VillanuevaОценок пока нет

- The Motor Vehicles Act, 1988 (Contd.) : (Section 140 To 217-A)Документ66 страницThe Motor Vehicles Act, 1988 (Contd.) : (Section 140 To 217-A)Matto MОценок пока нет

- TenancyДокумент3 страницыTenancyEunice Panopio LopezОценок пока нет

- Too Darn Hot!: From: "Kiss Me Kate"Документ8 страницToo Darn Hot!: From: "Kiss Me Kate"Samuel SmallsОценок пока нет

- Hedging, Portfolio Insurance & Cascade TheoryДокумент44 страницыHedging, Portfolio Insurance & Cascade TheorystanОценок пока нет

- Essentials of FraudДокумент6 страницEssentials of FraudShivangi BajpaiОценок пока нет

- Construction ContractДокумент2 страницыConstruction ContractMaria Estrelita EsposoОценок пока нет

- Lady Sarah Bank Guarantee DraftДокумент5 страницLady Sarah Bank Guarantee DraftFirooz JavizianОценок пока нет

- IndemnityДокумент11 страницIndemnityvedant guptaОценок пока нет

- DBB2101 Unit-02Документ24 страницыDBB2101 Unit-02Pooja jhaОценок пока нет

- Bashir-UCP Art1, Trade PaymentДокумент89 страницBashir-UCP Art1, Trade PaymentMasud Khan ShakilОценок пока нет

- 1 - Pearl & Dean v. ShoemartДокумент3 страницы1 - Pearl & Dean v. ShoemartPaulo SalanguitОценок пока нет

- Mercantile Law Q and A 1990 To 2006Документ166 страницMercantile Law Q and A 1990 To 2006Antolin Damasco LaceaОценок пока нет

- Title 3Документ6 страницTitle 3Mark Hiro Nakagawa0% (1)