Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- L Rexx PDFДокумент9 страницL Rexx PDFborisg3Оценок пока нет

- Angelina JolieДокумент14 страницAngelina Joliemaria joannah guanteroОценок пока нет

- Registration Form - Synergies in Communication - 6th Edition - 2017-Drobot AnaДокумент3 страницыRegistration Form - Synergies in Communication - 6th Edition - 2017-Drobot AnaAna IrinaОценок пока нет

- KV4BBSR Notice ContractuaL Interview 2023-24Документ9 страницKV4BBSR Notice ContractuaL Interview 2023-24SuchitaОценок пока нет

- Successful School LeadershipДокумент132 страницыSuccessful School LeadershipDabney90100% (2)

- Stellite 6 FinalДокумент2 страницыStellite 6 FinalGumersindo MelambesОценок пока нет

- Video Course NotesДокумент18 страницVideo Course NotesSiyeon YeungОценок пока нет

- BS EN 50483-6-2009 EnglishДокумент27 страницBS EN 50483-6-2009 EnglishДмитро Денис100% (2)

- Starex Is BTSДокумент24 страницыStarex Is BTSKLОценок пока нет

- 10CS 33 LOGIC DESIGN UNIT - 2 Combinational Logic CircuitsДокумент10 страниц10CS 33 LOGIC DESIGN UNIT - 2 Combinational Logic CircuitsMallikarjunBhiradeОценок пока нет

- Sample TRM All Series 2020v1 - ShortseДокумент40 страницSample TRM All Series 2020v1 - ShortseSuhail AhmadОценок пока нет

- AM-FM Reception TipsДокумент3 страницыAM-FM Reception TipsKrishna Ghimire100% (1)

- " Suratgarh Super Thermal Power Station": Submitted ToДокумент58 страниц" Suratgarh Super Thermal Power Station": Submitted ToSahuManishОценок пока нет

- Approximate AnalysisДокумент35 страницApproximate AnalysisSyahir HamidonОценок пока нет

- Denial of LOI & LOP For Ayurveda Colleges Under 13A For AY-2021-22 As On 18.02.2022Документ1 страницаDenial of LOI & LOP For Ayurveda Colleges Under 13A For AY-2021-22 As On 18.02.2022Gbp GbpОценок пока нет

- Chapter 4 Seepage TheoriesДокумент60 страницChapter 4 Seepage Theoriesmimahmoud100% (1)

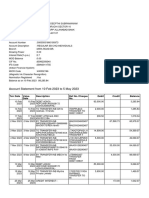

- Feb-May SBI StatementДокумент2 страницыFeb-May SBI StatementAshutosh PandeyОценок пока нет

- Philippine Rural Development Project: South Luzon Cluster C Ommunication Resourc ES Management WorkshopДокумент45 страницPhilippine Rural Development Project: South Luzon Cluster C Ommunication Resourc ES Management WorkshopAlorn CatibogОценок пока нет

- Clevite Bearing Book EB-40-07Документ104 страницыClevite Bearing Book EB-40-07lowelowelОценок пока нет

- TMA GuideДокумент3 страницыTMA GuideHamshavathini YohoratnamОценок пока нет

- CYPE 2021 + CYPE ArchitectureДокумент15 страницCYPE 2021 + CYPE ArchitectureHajar CypeMarocОценок пока нет

- Nc4 Student BookДокумент128 страницNc4 Student Book178798156Оценок пока нет

- Calculus of Finite Differences: Andreas KlappeneckerДокумент30 страницCalculus of Finite Differences: Andreas KlappeneckerSouvik RoyОценок пока нет

- Dashrath Nandan JAVA (Unit2) NotesДокумент18 страницDashrath Nandan JAVA (Unit2) NotesAbhinandan Singh RanaОценок пока нет

- 5 Teacher Induction Program - Module 5Документ27 страниц5 Teacher Induction Program - Module 5LAZABELLE BAGALLON0% (1)

- WKS 8 & 9 - Industrial Dryer 2T 2020-2021Документ26 страницWKS 8 & 9 - Industrial Dryer 2T 2020-2021Mei Lamfao100% (1)

- End Points SubrogadosДокумент3 страницыEnd Points SubrogadosAgustina AndradeОценок пока нет

- RESUME1Документ2 страницыRESUME1sagar09100% (5)

- SQL TestДокумент10 страницSQL TestGautam KatlaОценок пока нет

- New Cisco Certification Path (From Feb2020) PDFДокумент1 страницаNew Cisco Certification Path (From Feb2020) PDFkingОценок пока нет