Вам также может понравиться

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Common Agreement FINALДокумент113 страницCommon Agreement FINALIndependence InstituteОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Cruz AДокумент5 страницCruz AIndependence InstituteОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Abound Solar Term Sheet - Redacted - MarkedДокумент37 страницAbound Solar Term Sheet - Redacted - MarkedIndependence InstituteОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Abound Email WatermarkedДокумент1 страницаAbound Email WatermarkedIndependence InstituteОценок пока нет

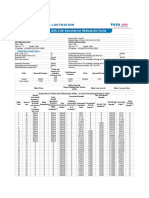

- Pinnacol Extraction1Документ12 страницPinnacol Extraction1Independence InstituteОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Exhibits To Common Agreement FINAL - MarkedДокумент172 страницыExhibits To Common Agreement FINAL - MarkedIndependence InstituteОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Cruz AДокумент5 страницCruz AIndependence InstituteОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Cruz AДокумент5 страницCruz AIndependence InstituteОценок пока нет

- Cruz AДокумент5 страницCruz AIndependence InstituteОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- DOR Email To CDOTДокумент1 страницаDOR Email To CDOTIndependence InstituteОценок пока нет

- User Based FeeДокумент1 страницаUser Based FeeIndependence InstituteОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Quota by Any Other Name-The Cost of Affirmative Action Programs in The Construction of DIAДокумент11 страницA Quota by Any Other Name-The Cost of Affirmative Action Programs in The Construction of DIAIndependence InstituteОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Proposed Gas TaxesДокумент1 страницаProposed Gas TaxesIndependence InstituteОценок пока нет

- CDOT Gas Tax AssumptionsДокумент4 страницыCDOT Gas Tax AssumptionsIndependence InstituteОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Better Living Through ElectricityДокумент2 страницыBetter Living Through ElectricityIndependence InstituteОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- 36th Quebec Red Light CamДокумент51 страница36th Quebec Red Light CamAnonymous kprzCiZ0% (1)

- Cruz AДокумент5 страницCruz AIndependence InstituteОценок пока нет

- Asset Forfeiture Reform Is Long OverdueДокумент15 страницAsset Forfeiture Reform Is Long OverdueIndependence InstituteОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Colorado's Anti-Transportation PolicyДокумент3 страницыColorado's Anti-Transportation PolicyIndependence InstituteОценок пока нет

- "Concerning Issuance of Civil Restraining Orders" - Good Intentions Are Not EnoughДокумент2 страницы"Concerning Issuance of Civil Restraining Orders" - Good Intentions Are Not EnoughIndependence Institute100% (1)

- "Prohibition On The Requirement of Donation of Professional Services" - Keeping Voluntary, VoluntaryДокумент2 страницы"Prohibition On The Requirement of Donation of Professional Services" - Keeping Voluntary, VoluntaryIndependence InstituteОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Access To The Internet - Regulation or MarketsДокумент4 страницыAccess To The Internet - Regulation or MarketsIndependence InstituteОценок пока нет

- Sotomayor Testimony (IP-6-2009)Документ6 страницSotomayor Testimony (IP-6-2009)Independence InstituteОценок пока нет

- Privatizing and Eliminating The Monopoly of The United States Postal ServiceДокумент18 страницPrivatizing and Eliminating The Monopoly of The United States Postal ServiceIndependence InstituteОценок пока нет

- Issue Backgrounder: Debt DetectiveДокумент4 страницыIssue Backgrounder: Debt DetectiveIndependence InstituteОценок пока нет

- How To Save A Billion Dollars in Other Post-Employment Benefit CostsДокумент10 страницHow To Save A Billion Dollars in Other Post-Employment Benefit CostsIndependence InstituteОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Coloradans Can't Afford The 'Prescription Drug Fair Pricing Act'Документ9 страницColoradans Can't Afford The 'Prescription Drug Fair Pricing Act'Independence InstituteОценок пока нет

- How Colorado Has Raised $300 Million in Debt WithoutДокумент5 страницHow Colorado Has Raised $300 Million in Debt WithoutIndependence InstituteОценок пока нет

- Colorado Bridge EnterpriseДокумент4 страницыColorado Bridge EnterpriseIndependence InstituteОценок пока нет

- Senate Bill 11-200: The Colorado Health Benefit ExchangeДокумент2 страницыSenate Bill 11-200: The Colorado Health Benefit ExchangeIndependence InstituteОценок пока нет

- CLC and Fund ConventionДокумент58 страницCLC and Fund ConventionSelva SelvarajОценок пока нет

- Repair of Buildings at LantapДокумент10 страницRepair of Buildings at Lantapjuncos0729Оценок пока нет

- 0853 Aig Guide To TrustsДокумент8 страниц0853 Aig Guide To Trustsmails4vipsОценок пока нет

- The Classification of Fire Code Revenues and Rates Are Prescribed in The Following ScheduleДокумент4 страницыThe Classification of Fire Code Revenues and Rates Are Prescribed in The Following Scheduledarius mercadoОценок пока нет

- MAY25 To AUG26 (3 MONTHS G.K. For All Competitive Exam Special Bank's PO - CLERK) AshishДокумент82 страницыMAY25 To AUG26 (3 MONTHS G.K. For All Competitive Exam Special Bank's PO - CLERK) Ashishashishkumar706Оценок пока нет

- Fries Station Business PlanДокумент49 страницFries Station Business PlanRandom StrangerОценок пока нет

- Policy QuotationДокумент1 страницаPolicy QuotationGuruОценок пока нет

- FNTG Welcome October 2015 Final 1 1Документ13 страницFNTG Welcome October 2015 Final 1 1api-231618151Оценок пока нет

- What My Family Should KnowДокумент26 страницWhat My Family Should KnowsivaОценок пока нет

- Mahalife GoldДокумент5 страницMahalife GoldFiniscope - Investment AdvisorsОценок пока нет

- Cir V Phil American DIGESTДокумент3 страницыCir V Phil American DIGESTjannagotgoodОценок пока нет

- Bharti Axa Life Insurance Company LTDДокумент90 страницBharti Axa Life Insurance Company LTDHimanshi AroraОценок пока нет

- Distance Learning Module Advanced Taxation CFM-300 PDFДокумент128 страницDistance Learning Module Advanced Taxation CFM-300 PDFKafonyi John100% (1)

- No IdaДокумент25 страницNo IdaSanjay Maurya0% (1)

- General Conditions of Contract Qatar May 2007Документ58 страницGeneral Conditions of Contract Qatar May 2007Leonidas AnaxandridaОценок пока нет

- Module 5 - Documentation & Healthcare Records Ethical Considerations in Leadership & ManagementДокумент14 страницModule 5 - Documentation & Healthcare Records Ethical Considerations in Leadership & ManagementKatie HolmesОценок пока нет

- Cooperative CodeДокумент20 страницCooperative CodeJason Hail PitosОценок пока нет

- HR Budget PresentationДокумент11 страницHR Budget PresentationMilanie NoriegaОценок пока нет

- Birla Sun Life Century SIP PresentationДокумент42 страницыBirla Sun Life Century SIP PresentationDrashti Investments100% (7)

- Motorcycle Insurance Receipt PDFДокумент1 страницаMotorcycle Insurance Receipt PDFWan RidhwanОценок пока нет

- Annex 9 - Pilot Agencies Covered National Competition PolicyДокумент1 страницаAnnex 9 - Pilot Agencies Covered National Competition PolicyAtdinum EnergyОценок пока нет

- NAIC ClaimFormДокумент4 страницыNAIC ClaimFormVinamra JaiswalОценок пока нет

- CII IF2-General Insurance Business-1Документ276 страницCII IF2-General Insurance Business-1paschalpaul722100% (1)

- Incentive-Based Compensation, Contingent Commissions and Required Broker Disclosures: Is There A Meeting of The Minds?Документ12 страницIncentive-Based Compensation, Contingent Commissions and Required Broker Disclosures: Is There A Meeting of The Minds?ACELitigationWatchОценок пока нет

- Marine InsuranceДокумент3 страницыMarine InsuranceKirtishbose ChowdhuryОценок пока нет

- Tax3211 Estate Tax 220318 130404Документ17 страницTax3211 Estate Tax 220318 130404MOTC INTERNAL AUDIT SECTIONОценок пока нет

- NFIFWI - Circular Details - Print PreviewДокумент2 страницыNFIFWI - Circular Details - Print PreviewVijay KumarОценок пока нет

- Benefit Illustration: (This Shall Form A Part of The Policy Document)Документ2 страницыBenefit Illustration: (This Shall Form A Part of The Policy Document)Pandit Katti NarahariОценок пока нет

- Applying Machine LearningДокумент4 страницыApplying Machine LearningAlexandros PapadopoulosОценок пока нет

- Financial LiteracyДокумент32 страницыFinancial LiteracyJim Boy BumalinОценок пока нет

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsОт EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsОценок пока нет

- Lower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderОт EverandLower Your Taxes - BIG TIME! 2023-2024: Small Business Wealth Building and Tax Reduction Secrets from an IRS InsiderОценок пока нет

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesОт EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesОценок пока нет

- Small Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyОт EverandSmall Business Taxes: The Most Complete and Updated Guide with Tips and Tax Loopholes You Need to Know to Avoid IRS Penalties and Save MoneyОценок пока нет

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProОт EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProРейтинг: 4.5 из 5 звезд4.5/5 (43)

- What Your CPA Isn't Telling You: Life-Changing Tax StrategiesОт EverandWhat Your CPA Isn't Telling You: Life-Changing Tax StrategiesРейтинг: 4 из 5 звезд4/5 (9)

- Taxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCОт EverandTaxes for Small Businesses QuickStart Guide: Understanding Taxes for Your Sole Proprietorship, StartUp & LLCРейтинг: 4 из 5 звезд4/5 (5)

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyОт EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyРейтинг: 4 из 5 звезд4/5 (52)