Вам также может понравиться

- Financial System in India and ChinaДокумент12 страницFinancial System in India and ChinaNavdeep KhokharОценок пока нет

- China Microfinance Industry Assessment ReportДокумент72 страницыChina Microfinance Industry Assessment Reportapi-17447836Оценок пока нет

- Role of Commercial Bank in The Economic Development of INDIAДокумент5 страницRole of Commercial Bank in The Economic Development of INDIAVaibhavRanjankar0% (1)

- Money and BankingДокумент15 страницMoney and BankingNaina SobtiОценок пока нет

- Banking LawДокумент18 страницBanking LawMunesh PandeyОценок пока нет

- Changing Scenario of Indian Banking SectorДокумент14 страницChanging Scenario of Indian Banking Sectorrupeshdahake8586100% (2)

- Chapter 1,2,3 PDFДокумент36 страницChapter 1,2,3 PDFprapoorna chintaОценок пока нет

- Pakistans PostReforms Banking SectorДокумент5 страницPakistans PostReforms Banking SectorAyeshaJangdaОценок пока нет

- Access to Finance: Microfinance Innovations in the People's Republic of ChinaОт EverandAccess to Finance: Microfinance Innovations in the People's Republic of ChinaОценок пока нет

- Comparative Analysis of MSME Financial Institutions in Select CountriesДокумент75 страницComparative Analysis of MSME Financial Institutions in Select CountriesGogol SarinОценок пока нет

- Evolution of Indian Financial System: A Critical Review: Saraswathi Chandrashekhar DR Yogesh MaheshwariДокумент12 страницEvolution of Indian Financial System: A Critical Review: Saraswathi Chandrashekhar DR Yogesh Maheshwarividhyashekar93Оценок пока нет

- Financial InclusionДокумент90 страницFinancial InclusionRohan Mehra0% (1)

- Role of Commercial Banks in Economic Development: Indian PerspectiveДокумент6 страницRole of Commercial Banks in Economic Development: Indian PerspectivekapuОценок пока нет

- Banking in India - Reforms and Reorganization: Rajesh - Chakrabarti@mgt - Gatech.eduДокумент27 страницBanking in India - Reforms and Reorganization: Rajesh - Chakrabarti@mgt - Gatech.eduilusonaОценок пока нет

- Emerging Issues in Finance Sector Inclusion, Deepening, and Development in the People's Republic of ChinaОт EverandEmerging Issues in Finance Sector Inclusion, Deepening, and Development in the People's Republic of ChinaОценок пока нет

- Introduction and Design of The Study: NBFCS: A Historical BackgroundДокумент51 страницаIntroduction and Design of The Study: NBFCS: A Historical BackgroundSWATHIKRISHNA RОценок пока нет

- The Impact of Deregulation On Commercial Banks and Their CustomersДокумент14 страницThe Impact of Deregulation On Commercial Banks and Their Customersshoaib_shebi6022Оценок пока нет

- Biased Lending and Non-Performing Loans in ChinasДокумент24 страницыBiased Lending and Non-Performing Loans in ChinasmeronОценок пока нет

- Full Report On Al Barakah Islamic BankingДокумент60 страницFull Report On Al Barakah Islamic BankingDil NawazОценок пока нет

- Role of Financial Institutions in Economic Development of Pakistan Essay Sample - Papers and Articles On Bla Bla WritingДокумент5 страницRole of Financial Institutions in Economic Development of Pakistan Essay Sample - Papers and Articles On Bla Bla WritingMuhammad Shahid Saddique33% (3)

- Chapter 3 The Role of Financial Institutions in The Economic Development of Malawi: Commercial Banks PerspectiveДокумент27 страницChapter 3 The Role of Financial Institutions in The Economic Development of Malawi: Commercial Banks PerspectiveBasilio MaliwangaОценок пока нет

- Privatisation in BankДокумент9 страницPrivatisation in BankGaurav TripathiОценок пока нет

- Project Report 4th Sem 1Документ51 страницаProject Report 4th Sem 1Neha SachdevaОценок пока нет

- Turnell On BankingReformInMyanmar-1Документ17 страницTurnell On BankingReformInMyanmar-1Su Wai MОценок пока нет

- Indian Banking: in Age of Hi-Tech EraДокумент16 страницIndian Banking: in Age of Hi-Tech Eraagrawal uditОценок пока нет

- Assessment of Corporate Governance Challenges Problems of MFIs in Ethiopia and The Way ForwardДокумент28 страницAssessment of Corporate Governance Challenges Problems of MFIs in Ethiopia and The Way ForwardhanyimwdmОценок пока нет

- College Magazine Latest KrishnanДокумент6 страницCollege Magazine Latest KrishnanChalil KrishnanОценок пока нет

- 03 - Review of LiteretureДокумент7 страниц03 - Review of LitereturePratham GadaОценок пока нет

- The Role of Regional Rural Banks (RRBS) in Financial Inclusion: An Empirical Study On West Bengal State in IndiaДокумент12 страницThe Role of Regional Rural Banks (RRBS) in Financial Inclusion: An Empirical Study On West Bengal State in IndiaKaran JainОценок пока нет

- From Stress To Growth: Strengthening Asia's Financial Systems in a Post-Crisis WorldОт EverandFrom Stress To Growth: Strengthening Asia's Financial Systems in a Post-Crisis WorldОценок пока нет

- Microfinance in VietnamДокумент11 страницMicrofinance in VietnamHoang Nang ThangОценок пока нет

- Group Assignment - Research FinalllyaДокумент10 страницGroup Assignment - Research FinalllyaMusurmonqul ChorievОценок пока нет

- Assignment On Role of Financial Institution: Rukmini Devi Institute OF Advanced StudiesДокумент12 страницAssignment On Role of Financial Institution: Rukmini Devi Institute OF Advanced StudiesHarshita ShekhawatОценок пока нет

- Chapter On Banking SectorДокумент19 страницChapter On Banking Sectorvikas jainОценок пока нет

- Performance and Financial Ratios of Commercial Banks in Malaysia and ChinaДокумент12 страницPerformance and Financial Ratios of Commercial Banks in Malaysia and Chinatedy hermawanОценок пока нет

- The Present and Future of China's New Rural Financial InstitutionsДокумент4 страницыThe Present and Future of China's New Rural Financial InstitutionsaijbmОценок пока нет

- The Role of Financial Institutions in Long Run Economic GrowthДокумент12 страницThe Role of Financial Institutions in Long Run Economic GrowthPrateek GaurОценок пока нет

- Sustainability 10 01194 v2 PDFДокумент20 страницSustainability 10 01194 v2 PDFRajendra LamsalОценок пока нет

- Case 2 Uas IC COSO Bank ChinaДокумент9 страницCase 2 Uas IC COSO Bank ChinaAndreas NainggolanОценок пока нет

- Chinese Financial SystemДокумент5 страницChinese Financial Systemsanjana sureshОценок пока нет

- Role of Nationalised Banks in The EconomyДокумент5 страницRole of Nationalised Banks in The EconomyAshis karmakar100% (1)

- CHAPTER 1: Introduction: 1.1 Definition of BanksДокумент99 страницCHAPTER 1: Introduction: 1.1 Definition of BanksTushar KhandelwalОценок пока нет

- Banking Sector Reforms Lesson From PakistanДокумент15 страницBanking Sector Reforms Lesson From Pakistanzainahmedrajput224Оценок пока нет

- The Impact of Macro Factors On The Profitability of China's Commercial Banks in The Decade After WTO AccessionДокумент6 страницThe Impact of Macro Factors On The Profitability of China's Commercial Banks in The Decade After WTO AccessiondinandaОценок пока нет

- Institutii de Credit Articol 10Документ10 страницInstitutii de Credit Articol 10Liliana DОценок пока нет

- Banking Law NotesДокумент49 страницBanking Law NotesABINASH NRUSINGHAОценок пока нет

- Banking SectorДокумент8 страницBanking SectorSupreet KaurОценок пока нет

- Term Paper On Development of Banking Sector in EthiopiaДокумент13 страницTerm Paper On Development of Banking Sector in EthiopiaSHALAMA DESTA TUSAОценок пока нет

- Analysis of Growth Prospects of Non BankДокумент7 страницAnalysis of Growth Prospects of Non Bankmahesh toshniwalОценок пока нет

- SMFISF270412 - Strengthening Governance in Micro Finance Institutions (MFIs) - Some Random ThoughtsДокумент17 страницSMFISF270412 - Strengthening Governance in Micro Finance Institutions (MFIs) - Some Random ThoughtsKhushboo KarnОценок пока нет

- Emmanuel Ngaga - ProposalДокумент26 страницEmmanuel Ngaga - Proposalhamzasadick99Оценок пока нет

- A Study On Financial Statement Analysis of HDFCДокумент63 страницыA Study On Financial Statement Analysis of HDFCKeleti SanthoshОценок пока нет

- A Review of Role and Challenges of Non-Banking Financial Companies in Economic Development of IndiaДокумент9 страницA Review of Role and Challenges of Non-Banking Financial Companies in Economic Development of IndiaSushm GiriОценок пока нет

- Fin 301Документ6 страницFin 301Mostafa ZubaerОценок пока нет

- Performance Appraisal of Urban Cooperative Banks: A Case StudyДокумент15 страницPerformance Appraisal of Urban Cooperative Banks: A Case StudyChethan KumarОценок пока нет

- Role of Commercial Banks in Development Financing in BangladeshДокумент31 страницаRole of Commercial Banks in Development Financing in Bangladeshfind4mohsinОценок пока нет

- Financial Inclusion in IndiaДокумент7 страницFinancial Inclusion in IndiaAsim MahatoОценок пока нет

- Role of Finacial Institution in Industrial DevelopmentДокумент56 страницRole of Finacial Institution in Industrial DevelopmentTasmay EnterprisesОценок пока нет

- 15 - Chapter 6 PDFДокумент30 страниц15 - Chapter 6 PDFRukminiОценок пока нет

- 2WPSN140313Документ29 страниц2WPSN140313Rakesh BetiwarОценок пока нет

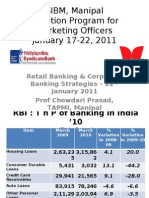

- 10 International Conference On Problem and Possibilities in Online Education in ManagementДокумент39 страниц10 International Conference On Problem and Possibilities in Online Education in ManagementProf Dr Chowdari PrasadОценок пока нет

- Prof Chowdari Prasad CV 26112018Документ11 страницProf Chowdari Prasad CV 26112018Prof Dr Chowdari PrasadОценок пока нет

- A Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsДокумент15 страницA Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsProf Dr Chowdari PrasadОценок пока нет

- Second Innings September 2019Документ52 страницыSecond Innings September 2019Prof Dr Chowdari PrasadОценок пока нет

- Performance of Crowd Funding in India: Issues and ChallengesДокумент19 страницPerformance of Crowd Funding in India: Issues and ChallengesProf Dr Chowdari Prasad100% (1)

- Consumer Protection Act 1986Документ41 страницаConsumer Protection Act 1986Prof Dr Chowdari Prasad100% (1)

- Digital Banking in India 2016Документ21 страницаDigital Banking in India 2016Prof Dr Chowdari Prasad100% (3)

- Recent Trends of PE Funding in IndiaДокумент38 страницRecent Trends of PE Funding in IndiaProf Dr Chowdari PrasadОценок пока нет

- Tapmi Update 2013Документ120 страницTapmi Update 2013Prof Dr Chowdari PrasadОценок пока нет

- HR As A Strategic Business PartnerДокумент36 страницHR As A Strategic Business PartnerProf Dr Chowdari PrasadОценок пока нет

- MFI National ConferenceДокумент12 страницMFI National ConferenceProf Dr Chowdari PrasadОценок пока нет

- Social Entrepreneurship2015Документ45 страницSocial Entrepreneurship2015Prof Dr Chowdari PrasadОценок пока нет

- Lean and Green Banking in India 2012Документ20 страницLean and Green Banking in India 2012Prof Dr Chowdari Prasad100% (2)

- Women Achievers Ebook2Документ95 страницWomen Achievers Ebook2Prof Dr Chowdari PrasadОценок пока нет

- Profile of Banks 2010-11Документ99 страницProfile of Banks 2010-11Vishesh KumarОценок пока нет

- Sibm, RBCBДокумент20 страницSibm, RBCBProf Dr Chowdari PrasadОценок пока нет

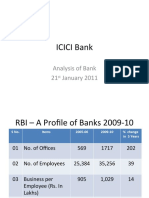

- Icici Bank: Analysis of Bank 21 January 2011Документ6 страницIcici Bank: Analysis of Bank 21 January 2011Prof Dr Chowdari PrasadОценок пока нет

- List of Books On Micro FinanceДокумент32 страницыList of Books On Micro FinanceProf Dr Chowdari Prasad71% (7)

- Myths of Microfinance - Global South Development Magazine JAN 2011Документ42 страницыMyths of Microfinance - Global South Development Magazine JAN 2011Silver Lining CreationОценок пока нет

- TAPMI ManipalДокумент18 страницTAPMI ManipalProf Dr Chowdari Prasad100% (1)

- Syndicate Institute of Bank Management, ManipalДокумент67 страницSyndicate Institute of Bank Management, ManipalProf Dr Chowdari PrasadОценок пока нет

- Forms Checklist From Pub 559Документ1 страницаForms Checklist From Pub 559FredОценок пока нет

- A-EduAchieve 2 Brochure Final 07052019Документ14 страницA-EduAchieve 2 Brochure Final 07052019Navinkumar G.KunarathinamОценок пока нет

- Last Minute Tax TipsДокумент2 страницыLast Minute Tax TipsIncome Solutions Wealth ManagementОценок пока нет

- Madoff's American Express Corporate Card StatementДокумент30 страницMadoff's American Express Corporate Card StatementInvestor Protection100% (3)

- Extended Stay America St. Petersburg Clearwater Executive DRДокумент2 страницыExtended Stay America St. Petersburg Clearwater Executive DRSiva AllaОценок пока нет

- Retail Loan Rates Comparision Chart PDFДокумент3 страницыRetail Loan Rates Comparision Chart PDF9778486995Оценок пока нет

- Interview Questions of FinanceДокумент126 страницInterview Questions of FinanceAnand KumarОценок пока нет

- A Study of Customer Satisfaction For Services Provided by KCC BankДокумент72 страницыA Study of Customer Satisfaction For Services Provided by KCC BankANKITОценок пока нет

- Vendor Registration Form - VRF 3 0Документ1 страницаVendor Registration Form - VRF 3 0Suraj Sankar Mukherjee100% (1)

- Table 1 - Recommended Etfs: Financial Products ResearchДокумент3 страницыTable 1 - Recommended Etfs: Financial Products ResearchBobОценок пока нет

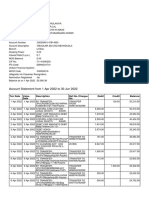

- Account Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент10 страницAccount Statement From 1 Apr 2022 To 30 Jun 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceParveen SainiОценок пока нет

- 3-1-Notice of Correction For FraudДокумент2 страницы3-1-Notice of Correction For FraudJohn DownsОценок пока нет

- Axis Bank ProjectДокумент19 страницAxis Bank ProjectNikky NamdeoОценок пока нет

- Docs 101Документ3 страницыDocs 101Kristine B. MaestreОценок пока нет

- Intellectual Property Rights As Security For LoansДокумент2 страницыIntellectual Property Rights As Security For LoansReshma Balagopal100% (1)

- Digit Two Wheeler Package Policy - Long TermДокумент9 страницDigit Two Wheeler Package Policy - Long TermDeleter DoraОценок пока нет

- Analysis On Financial Health of HDFC Bank and Icici BankДокумент11 страницAnalysis On Financial Health of HDFC Bank and Icici Banksaket agarwalОценок пока нет

- Gregorio Araneta vs. Tuazon de PaternoДокумент16 страницGregorio Araneta vs. Tuazon de PaternoSherwin Anoba CabutijaОценок пока нет

- Application Letter For Transfer Bank AccountДокумент7 страницApplication Letter For Transfer Bank Accountjxaeizhfg100% (2)

- Accounts Project FinalДокумент18 страницAccounts Project FinalPulakОценок пока нет

- Shwethacoffee11 PDFДокумент6 страницShwethacoffee11 PDFabhilash eshwarappaОценок пока нет

- Downloads-Examination Centre List For Aug Sep 2012Документ7 страницDownloads-Examination Centre List For Aug Sep 2012Patrick AdamsОценок пока нет

- Chapter 13 The Human Resources Management and Payroll CycleДокумент67 страницChapter 13 The Human Resources Management and Payroll CycleislamelshahatОценок пока нет

- Customer StatementДокумент6 страницCustomer StatementEMEKA SAMSONОценок пока нет

- MCB BANK Internship ReportДокумент68 страницMCB BANK Internship Reportbbaahmad89100% (1)

- Top 15 Logistics Companies in IndiaДокумент8 страницTop 15 Logistics Companies in IndiaAnonymous WtjVcZCgОценок пока нет

- Uniform Loan Delivery Data - Set FaqsДокумент4 страницыUniform Loan Delivery Data - Set FaqsraghuОценок пока нет

- Petron Corporation V CIRДокумент2 страницыPetron Corporation V CIRiciamadarangОценок пока нет

- Anmol JeevanДокумент13 страницAnmol JeevanUtkarshОценок пока нет

- TK BAI2Документ23 страницыTK BAI2saurabh_565Оценок пока нет