Вам также может понравиться

- Answer KeyДокумент19 страницAnswer KeyRenОценок пока нет

- Future Scenarios Implications Industry Report 2018 PDFДокумент32 страницыFuture Scenarios Implications Industry Report 2018 PDFSerapioCazanaCanchisОценок пока нет

- Introduction To Management Accounting: Asst Prof. Jonlen DesaДокумент22 страницыIntroduction To Management Accounting: Asst Prof. Jonlen DesaAryanSainiОценок пока нет

- Chapter 2 - Auditing IT Governance Controls: True/FalseДокумент9 страницChapter 2 - Auditing IT Governance Controls: True/FalseShanygane Delos SantosОценок пока нет

- Management Accounting 1Документ11 страницManagement Accounting 1Parminder BajajОценок пока нет

- Reviewer - Responsibility AccountingДокумент12 страницReviewer - Responsibility AccountingRen EyОценок пока нет

- M D L 8: Financial: LiteracyДокумент15 страницM D L 8: Financial: LiteracyAngela Casimero SuspeneОценок пока нет

- HUMAN ACTS-action That Is Considered To Be ACTS OF MAN - Acts That Indeliberately or WithoutДокумент1 страницаHUMAN ACTS-action That Is Considered To Be ACTS OF MAN - Acts That Indeliberately or WithoutjparОценок пока нет

- Precalculus ReviewerДокумент6 страницPrecalculus ReviewerIna Louise MagnoОценок пока нет

- BA 328 - Ch5 - Process Selection, Design, and AnalysisДокумент16 страницBA 328 - Ch5 - Process Selection, Design, and AnalysisBeboy TorregosaОценок пока нет

- Pricing MethodsДокумент3 страницыPricing MethodsAkanksha VermaОценок пока нет

- Christianity Love AffairДокумент3 страницыChristianity Love AffairimmortalmasoОценок пока нет

- Balanced Scorecard and Responsibility AccountingДокумент7 страницBalanced Scorecard and Responsibility AccountingMonica GarciaОценок пока нет

- Research and Report Writing GuideДокумент8 страницResearch and Report Writing GuideAhmed HajiОценок пока нет

- Youth League SpeechДокумент3 страницыYouth League Speechsmiggle89Оценок пока нет

- QuizДокумент10 страницQuizRen100% (4)

- OT Notes OverviewДокумент8 страницOT Notes OverviewKayla ReeseОценок пока нет

- Memorable Family Trip to Gensan and TupiДокумент2 страницыMemorable Family Trip to Gensan and TupiDaille Ace llОценок пока нет

- This Study Resource Was: Value Chain Analysis: Southwest AirlinesДокумент2 страницыThis Study Resource Was: Value Chain Analysis: Southwest AirlinesJeffОценок пока нет

- Principles of MarketingДокумент15 страницPrinciples of MarketingAzael May PenaroyoОценок пока нет

- Acctg 320 Risk Management SummaryДокумент14 страницAcctg 320 Risk Management SummaryMeroz JunditОценок пока нет

- Automotive Value Chain Transformation to 2025Документ64 страницыAutomotive Value Chain Transformation to 2025MadhurimaОценок пока нет

- Cost Concepts and ClassificationsДокумент15 страницCost Concepts and ClassificationsMae Ann KongОценок пока нет

- ACC51112 Balanced ScorecardДокумент6 страницACC51112 Balanced ScorecardjasОценок пока нет

- Cap 1Документ19 страницCap 1Tina CRОценок пока нет

- Value Chain and Baseline AnalysisДокумент23 страницыValue Chain and Baseline AnalysisVikram Singh TomarОценок пока нет

- Ecco AДокумент5 страницEcco Aouzun852Оценок пока нет

- Basic Notes For Borrowing CostДокумент5 страницBasic Notes For Borrowing CostIqra HasanОценок пока нет

- H& B Final at 4 AmДокумент21 страницаH& B Final at 4 AmHarsh King Mehta83% (6)

- Strategic Management Term Paper On ACMEДокумент27 страницStrategic Management Term Paper On ACMESayed Abu SufyanОценок пока нет

- BCG Matrix of Nestle PDFДокумент34 страницыBCG Matrix of Nestle PDFVishakha RathodОценок пока нет

- Revision Class Bac1034Документ8 страницRevision Class Bac1034Brian JoshiОценок пока нет

- FIMDDA Debt Module1Документ7 страницFIMDDA Debt Module1Kirti SahniОценок пока нет

- FRM 5 Market Risk Related RisksДокумент38 страницFRM 5 Market Risk Related RisksLoraОценок пока нет

- M1 - Introduction To Valuation HandoutДокумент6 страницM1 - Introduction To Valuation HandoutPrince LeeОценок пока нет

- Research ProjectДокумент56 страницResearch Projectabuka.felixОценок пока нет

- Responsibility and Segment Accounting CRДокумент24 страницыResponsibility and Segment Accounting CRAshy LeeОценок пока нет

- Accounting For IntangiblesДокумент14 страницAccounting For Intangiblesmanoj17188100% (2)

- Business Studies - Finance Study NotesДокумент29 страницBusiness Studies - Finance Study NotesSamina Haider0% (1)

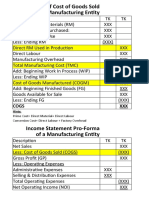

- Statement of Cost of Goods Sold of A Manufacturing Entity: Cogs XXXДокумент1 страницаStatement of Cost of Goods Sold of A Manufacturing Entity: Cogs XXXCasanovicОценок пока нет

- Chapter 3 Valuation and Cost of CapitalДокумент92 страницыChapter 3 Valuation and Cost of Capitalyemisrach fikiruОценок пока нет

- SEM-II-Cost & Management Accounting-I Overhead CostingДокумент8 страницSEM-II-Cost & Management Accounting-I Overhead CostingTanishq KambojОценок пока нет

- CONFIDENTIAL Corporate Finance ExamДокумент3 страницыCONFIDENTIAL Corporate Finance ExamAssignment HelperОценок пока нет

- Advanced Accounting Part 2 Business Combinations (Ifrs 3)Документ10 страницAdvanced Accounting Part 2 Business Combinations (Ifrs 3)ClarkОценок пока нет

- Fs HahahahahaДокумент26 страницFs HahahahahaDoreen Jean MabasoОценок пока нет

- Cost Accounting and Management AccountingДокумент11 страницCost Accounting and Management AccountingCollins AbereОценок пока нет

- ReviewerДокумент14 страницReviewerLenard TaberdoОценок пока нет

- AFAR 1 Partnership Accounting (Installment Liquidation)Документ3 страницыAFAR 1 Partnership Accounting (Installment Liquidation)Jeepee JohnОценок пока нет

- UL CPA REVIEW CENTER MAS 1.1 MANAGEMENT ACCOUNTINGДокумент8 страницUL CPA REVIEW CENTER MAS 1.1 MANAGEMENT ACCOUNTINGNhicoleChoiОценок пока нет

- Why Auditor Cannot Provide Absolute Level of Assurance in Audit EngagementДокумент2 страницыWhy Auditor Cannot Provide Absolute Level of Assurance in Audit EngagementAkif AlamОценок пока нет

- Script Financial LiteracyДокумент6 страницScript Financial LiteracyAngelica AruyalОценок пока нет

- Letter of Credit: Give Assurance To Your Sellers With ICICI Bank's Letter of CreditДокумент2 страницыLetter of Credit: Give Assurance To Your Sellers With ICICI Bank's Letter of CreditSanjay ShingalaОценок пока нет

- A Letter To GodДокумент2 страницыA Letter To Godnitisha mehrotraОценок пока нет

- Case Study FRMДокумент9 страницCase Study FRMSwati ChoudharyОценок пока нет

- Kuratko 9 e CH 01Документ36 страницKuratko 9 e CH 01lobna_qassem7176Оценок пока нет

- FM 415 - Chapter 2A PDFДокумент14 страницFM 415 - Chapter 2A PDFMarc Charles UsonОценок пока нет

- 1 - PRELIMINARY-Q - As - AFTER SESSION 4Документ6 страниц1 - PRELIMINARY-Q - As - AFTER SESSION 4Mighty SinghОценок пока нет

- Introduction-Business LawДокумент12 страницIntroduction-Business LawAmirul Hakim Nor AzmanОценок пока нет

- BCG Matrix: A Guide to Classifying Products and ServicesДокумент3 страницыBCG Matrix: A Guide to Classifying Products and ServicesPriya AshokОценок пока нет

- Strategic ManagementДокумент172 страницыStrategic ManagementAnil Reddy100% (1)

- Cost Terminology and Classification ExplainedДокумент8 страницCost Terminology and Classification ExplainedKanbiro Orkaido100% (1)

- LEASE ACCOUNTING ESSENTIALSДокумент6 страницLEASE ACCOUNTING ESSENTIALSIts meh SushiОценок пока нет

- Strategic ManagementДокумент12 страницStrategic ManagementDinesh DubariyaОценок пока нет

- Jollibee Food Corp - Group 5-1Документ14 страницJollibee Food Corp - Group 5-1Joan Perolino MadejaОценок пока нет

- Unit 2 Capital Budgeting Decisions: IllustrationsДокумент4 страницыUnit 2 Capital Budgeting Decisions: IllustrationsJaya SwethaОценок пока нет

- Accounting For Groups of CompaniesДокумент9 страницAccounting For Groups of CompaniesEmmanuel MwapeОценок пока нет

- Al Financial Management May Jun 2017Документ4 страницыAl Financial Management May Jun 2017Akash79Оценок пока нет

- FM ReportДокумент14 страницFM ReportyanaОценок пока нет

- NotesДокумент13 страницNotes4220019Оценок пока нет

- Holy Angel University Management AssignmentДокумент4 страницыHoly Angel University Management AssignmentDianne de JesusОценок пока нет

- 5Документ3 страницы5RenОценок пока нет

- 4Документ3 страницы4RenОценок пока нет

- Responsibility Accounting Concepts and CalculationsДокумент5 страницResponsibility Accounting Concepts and CalculationsRenОценок пока нет

- 2Документ3 страницы2RenОценок пока нет

- 2Документ3 страницы2RenОценок пока нет

- Assignment Beef Patty RecipeДокумент1 страницаAssignment Beef Patty RecipeRenОценок пока нет

- 1Документ4 страницы1RenОценок пока нет

- 3Документ5 страниц3RenОценок пока нет

- CAD ROI and Residual IncomeДокумент7 страницCAD ROI and Residual IncomeRen100% (1)

- 1 PointДокумент4 страницы1 PointRenОценок пока нет

- Activity 1 - Fundamentals To Auditing and Assurance ServicesДокумент14 страницActivity 1 - Fundamentals To Auditing and Assurance ServicesRen100% (1)

- (CITATION Uni12 /L 1033) (CITATION Var07 /L 1033)Документ2 страницы(CITATION Uni12 /L 1033) (CITATION Var07 /L 1033)RenОценок пока нет

- CAD ROI and Residual IncomeДокумент7 страницCAD ROI and Residual IncomeRen100% (1)

- COST Center (COST SBU) - Exercise 5 P. 507 Problem 4 p.512Документ5 страницCOST Center (COST SBU) - Exercise 5 P. 507 Problem 4 p.512RenОценок пока нет

- ExamДокумент6 страницExamRenОценок пока нет

- A. B. C. D. A. B. C. D.: ANSWER: Review Prior-Year Audit Documentation and The Permanent File For The ClientДокумент7 страницA. B. C. D. A. B. C. D.: ANSWER: Review Prior-Year Audit Documentation and The Permanent File For The ClientRenОценок пока нет

- AuditingДокумент9 страницAuditingRenОценок пока нет

- MANAGEMENT ACCOUNTING SOLUTIONS CHAPTER 14 RESPONSIBILITY ACCOUNTING TRANSFER PRICINGДокумент18 страницMANAGEMENT ACCOUNTING SOLUTIONS CHAPTER 14 RESPONSIBILITY ACCOUNTING TRANSFER PRICINGRenОценок пока нет

- Baking French Bread at Home: Craft Chewy Loaves With The Crispest Crust Using The Right Flours and Good Shaping TechniqueДокумент5 страницBaking French Bread at Home: Craft Chewy Loaves With The Crispest Crust Using The Right Flours and Good Shaping TechniqueRenОценок пока нет

- Aristotle Athanasius Kircher: Principles of The Science of Colour, LikelyДокумент1 страницаAristotle Athanasius Kircher: Principles of The Science of Colour, LikelyRenОценок пока нет

- Assignment Beef Patty RecipeДокумент1 страницаAssignment Beef Patty RecipeRenОценок пока нет

- Commodity Value Chain Management StrategiesДокумент12 страницCommodity Value Chain Management StrategiesDavid KОценок пока нет

- 20200615144430D3218 - Sesi 1&2Документ61 страница20200615144430D3218 - Sesi 1&2Gho Roberto ZebuaОценок пока нет

- Answers To Question Number 2: Push and Pull Supply ChainДокумент4 страницыAnswers To Question Number 2: Push and Pull Supply ChainMuhammad SaadОценок пока нет

- Reviewer OptqmДокумент18 страницReviewer OptqmIamkitten 00Оценок пока нет

- A Study On Factors Influencing The Consumer Buying Behaviour With Respect To NykaaДокумент22 страницыA Study On Factors Influencing The Consumer Buying Behaviour With Respect To NykaaYashvi RaiОценок пока нет

- Optimize IT service delivery with iterative feedbackДокумент33 страницыOptimize IT service delivery with iterative feedbackyash singadiaОценок пока нет

- Case Analysis of Amul FinalДокумент24 страницыCase Analysis of Amul FinalSarabjit Singh100% (1)

- Strategic Planning and ImplementationДокумент12 страницStrategic Planning and ImplementationShiva LKLОценок пока нет

- WSU manufacturing supply chain guideДокумент18 страницWSU manufacturing supply chain guideMihiretu0% (1)

- Agri Business Value ChainДокумент32 страницыAgri Business Value ChainMohammed Awwal NdayakoОценок пока нет

- A Global Perspective On Industry 4 0 and Development New Gaps or Opportunities To LeapfrogДокумент20 страницA Global Perspective On Industry 4 0 and Development New Gaps or Opportunities To LeapfrogMateo Cuadros HerreraОценок пока нет

- Organizational Strategy, Competitive Advantage, and Information SystemsДокумент60 страницOrganizational Strategy, Competitive Advantage, and Information SystemsJasong0% (1)

- UMKD6Q-15-3 Global Marketing Management Fentimans: Plan To Launch Their Botanically Brewed Soft Drinks Into The Japanese MarketДокумент9 страницUMKD6Q-15-3 Global Marketing Management Fentimans: Plan To Launch Their Botanically Brewed Soft Drinks Into The Japanese MarketNishant GuptaОценок пока нет

- Technology and Competitive AdvantageДокумент25 страницTechnology and Competitive Advantagewahyu artikaОценок пока нет

- S Swetha - Task 1Документ8 страницS Swetha - Task 1Swetha SrikanthОценок пока нет

- Understanding The Human Mind: The Big PictureДокумент11 страницUnderstanding The Human Mind: The Big PictureLawrence James MosqueraОценок пока нет

- Global Operations of KFCДокумент15 страницGlobal Operations of KFCsheikh rafinОценок пока нет

- Smallholder Business Models For Agribusiness-Led DevelopmentДокумент28 страницSmallholder Business Models For Agribusiness-Led Developmentbojik2Оценок пока нет

- Supply Chain Management of RECKEIIT BENKSEIERДокумент6 страницSupply Chain Management of RECKEIIT BENKSEIERFuhad AhmedОценок пока нет

- Knowledge Value Chain Framework for Construction TenderingДокумент157 страницKnowledge Value Chain Framework for Construction TenderingBimsara MalithОценок пока нет

- Dyanmics of Strategy PaperДокумент40 страницDyanmics of Strategy PaperMarianne Sammy100% (1)

- The Manager and Management AccountingДокумент24 страницыThe Manager and Management AccountingsofikhdyОценок пока нет