Вам также может понравиться

- Construction Industry Intrnal AuditДокумент129 страницConstruction Industry Intrnal AuditAlexandros Mavratsas100% (2)

- How to Raise Capital: Techniques and Strategies for Financing and Valuing your Small BusinessОт EverandHow to Raise Capital: Techniques and Strategies for Financing and Valuing your Small BusinessРейтинг: 3.5 из 5 звезд3.5/5 (2)

- Current Month April To Date Entitlement Amount Deductions Amount DeductionsДокумент1 страницаCurrent Month April To Date Entitlement Amount Deductions Amount DeductionsBIPINОценок пока нет

- Brand Elements Lead To Brand Equity Diff PDFДокумент11 страницBrand Elements Lead To Brand Equity Diff PDFsugandhaОценок пока нет

- All Slides - Delhi Algo Traders ConferenceДокумент129 страницAll Slides - Delhi Algo Traders ConferencenithyaprasathОценок пока нет

- Real Estate Asset Manager in Washington DC Resume Meaghen MurrayДокумент2 страницыReal Estate Asset Manager in Washington DC Resume Meaghen MurrayMeaghenMurrayОценок пока нет

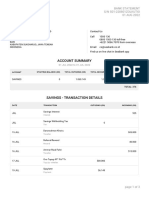

- Salman Khoirudin: Account SummaryДокумент3 страницыSalman Khoirudin: Account SummarySalman KhoirudinОценок пока нет

- Bank Statement Big ConamsaДокумент79 страницBank Statement Big ConamsaSIN24horasОценок пока нет

- (Hoff) Novel Ways of Implementing Carry Alpha in CommoditiesДокумент13 страниц(Hoff) Novel Ways of Implementing Carry Alpha in CommoditiesrlindseyОценок пока нет

- Cerezo-Amv BookstoreДокумент47 страницCerezo-Amv BookstoreMark Jayson Gonzaga Cerezo100% (3)

- MR - Money: Welcomes You AllДокумент22 страницыMR - Money: Welcomes You Allramya100% (1)

- The Insider's Guide to Tax-Free Real Estate Investments: Retire Rich Using Your IRAОт EverandThe Insider's Guide to Tax-Free Real Estate Investments: Retire Rich Using Your IRAОценок пока нет

- COL Technical Analysis (Part 2)Документ36 страницCOL Technical Analysis (Part 2)Olegario S. Sumaya IIIОценок пока нет

- Production of Sterile Water For Injection. WFI (Water For Injection) Manufacturing. Water For Pharmaceutical Purposes.-792178 PDFДокумент64 страницыProduction of Sterile Water For Injection. WFI (Water For Injection) Manufacturing. Water For Pharmaceutical Purposes.-792178 PDFGajjkОценок пока нет

- Monthly Transaction With Holding Statement BR9287 1208160055511358Документ2 страницыMonthly Transaction With Holding Statement BR9287 1208160055511358shishirОценок пока нет

- Fundamental Analysis by COL FInancialДокумент43 страницыFundamental Analysis by COL FInancialroksimalsОценок пока нет

- PRC Arrears Apr IncrementДокумент33 страницыPRC Arrears Apr IncrementbhavanakrishnaОценок пока нет

- Know More About Passive Income: - : by Tushar R. Ghone (Tstock Mantra Investment)Документ23 страницыKnow More About Passive Income: - : by Tushar R. Ghone (Tstock Mantra Investment)Tushar GhoneОценок пока нет

- Report H12016 Eng FinalДокумент29 страницReport H12016 Eng FinalTy BorjaОценок пока нет

- Tata Small Cap Fund - NFO PresentationДокумент22 страницыTata Small Cap Fund - NFO PresentationRajat GuptaОценок пока нет

- Trial Salary SlipДокумент5 страницTrial Salary SlipTvs12346Оценок пока нет

- Share CalculationДокумент3 страницыShare CalculationNitin RautОценок пока нет

- Kunj BansalДокумент24 страницыKunj Bansaldivya chawlaОценок пока нет

- PRC Arrears Aug IncrementДокумент35 страницPRC Arrears Aug Incrementbaachi_suОценок пока нет

- Stock To Watch Daily 15 Nov 2018Документ8 страницStock To Watch Daily 15 Nov 2018The EquicomОценок пока нет

- PayslipA4Report PDFДокумент1 страницаPayslipA4Report PDFMuhd AlifОценок пока нет

- Heatlh Checkup SampleДокумент2 страницыHeatlh Checkup Samplehariom86Оценок пока нет

- Watchlist NewДокумент5 страницWatchlist NewDhawanОценок пока нет

- Payslip Bob (Sept)Документ1 страницаPayslip Bob (Sept)Muhd AlifОценок пока нет

- I R R (Version 1)Документ13 страницI R R (Version 1)Bhaskar JadhavОценок пока нет

- Cost of Project Particulars Existing Proposed TotalДокумент3 страницыCost of Project Particulars Existing Proposed TotalsanooОценок пока нет

- An Update - Old Bridge CapitalДокумент3 страницыAn Update - Old Bridge CapitalAshwin HasyagarОценок пока нет

- Eih 2020Документ255 страницEih 2020Achirangshu MukhopadhyayОценок пока нет

- Maxime Project ReportДокумент60 страницMaxime Project ReportMOHD GULZARОценок пока нет

- Pallwood SRL: Operational and Investments Plan FinancialsДокумент14 страницPallwood SRL: Operational and Investments Plan Financialsulma andreiОценок пока нет

- CapitalGainLossSummary pcpw055Документ6 страницCapitalGainLossSummary pcpw055Prachi PatwariОценок пока нет

- Extract of All Sales Vouchers 1-Apr-2015 To 31-Dec-2015Документ8 страницExtract of All Sales Vouchers 1-Apr-2015 To 31-Dec-2015taseerОценок пока нет

- Rwesoa Ga91915 20240331Документ1 страницаRwesoa Ga91915 20240331Phil's ChannelОценок пока нет

- L33 10 PDFДокумент1 страницаL33 10 PDF魏釨洋Оценок пока нет

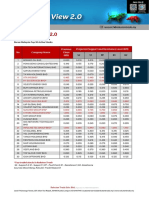

- Technical View 2.0 - 7 February 2023Документ2 страницыTechnical View 2.0 - 7 February 2023Abdul Razak NohОценок пока нет

- Business Proposal For Bulk SMS Gateway KorbaДокумент9 страницBusiness Proposal For Bulk SMS Gateway KorbaSaurabh Gupta33% (3)

- ELITE WORLD NATIONAL EST. LLC - Credit ReportДокумент11 страницELITE WORLD NATIONAL EST. LLC - Credit ReportMirageОценок пока нет

- 1qjul2022tg 684Документ1 страница1qjul2022tg 684Camilo DiazОценок пока нет

- KPM Super Market: Tax InvoiceДокумент1 страницаKPM Super Market: Tax InvoiceKpm SupermarketОценок пока нет

- AC1103A1 - Lesson 7Документ3 страницыAC1103A1 - Lesson 7Mursyidah OmarОценок пока нет

- Inmunization FabozziДокумент17 страницInmunization FabozzijulietacavestrillanoОценок пока нет

- Trial Balance - 31.12.2021Документ2 страницыTrial Balance - 31.12.2021Si HadiОценок пока нет

- Project Report Papad ManufacturingДокумент7 страницProject Report Papad ManufacturingPriyotosh DasОценок пока нет

- Plot Limit Plot Limit: LegendsДокумент1 страницаPlot Limit Plot Limit: LegendsLucky MalihanОценок пока нет

- Golden Hotpot & Grill Partnership Proposal 2023Документ15 страницGolden Hotpot & Grill Partnership Proposal 2023KokoWidhiAtmokoОценок пока нет

- Financial Performance Report General Tyres and Rubber Company-FinalДокумент29 страницFinancial Performance Report General Tyres and Rubber Company-FinalKabeer QureshiОценок пока нет

- GST Invoice Format No. 12 PDFДокумент1 страницаGST Invoice Format No. 12 PDFArindam ChandaОценок пока нет

- RPT Bulk Customer InfoДокумент1 страницаRPT Bulk Customer InfoHarry JackОценок пока нет

- Stock Valuation SheetДокумент6 страницStock Valuation Sheetthouseef06Оценок пока нет

- HDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971Документ1 страницаHDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971Devender5194Оценок пока нет

- Mdpe - (HDD-01) PP DrawingДокумент1 страницаMdpe - (HDD-01) PP DrawingSaravananОценок пока нет

- Pincon Spirit Limited: 37th Annual ReportДокумент66 страницPincon Spirit Limited: 37th Annual ReportSiddharth ShekharОценок пока нет

- Tata PowerДокумент8 страницTata PowerAyan ChatterjeeОценок пока нет

- Willingness of LGATДокумент3 страницыWillingness of LGATAhmed HannanОценок пока нет

- Financial Aspects of Kotak Mahindra BankДокумент6 страницFinancial Aspects of Kotak Mahindra Bankajeetkumarverma 2k21dmba20Оценок пока нет

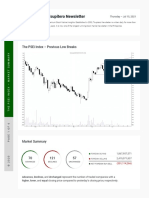

- Tsupitero Newsletter: The Psei Index - Previous Low BreaksДокумент6 страницTsupitero Newsletter: The Psei Index - Previous Low BreaksEdsel LoquillanoОценок пока нет

- Meta 156-1Документ15 страницMeta 156-1anyelo_jossueОценок пока нет

- Shiba Floki BEP-20 Audit 8725475Документ19 страницShiba Floki BEP-20 Audit 8725475prila hermantoОценок пока нет

- Financial DataДокумент21 страницаFinancial DataTest DriveОценок пока нет

- Cash Flow2DДокумент1 страницаCash Flow2DFurquan KhanОценок пока нет

- Allied Engineering & Services (PVT.) LTDДокумент2 страницыAllied Engineering & Services (PVT.) LTDmuhammad omerОценок пока нет

- Grignard 5Документ1 страницаGrignard 5elbronОценок пока нет

- Grignard 1Документ2 страницыGrignard 1elbronОценок пока нет

- Grignard 3Документ2 страницыGrignard 3elbronОценок пока нет

- Grignard 4Документ2 страницыGrignard 4elbronОценок пока нет

- Limitations of The Grignard Reaction Grignard ReagentsДокумент2 страницыLimitations of The Grignard Reaction Grignard ReagentselbronОценок пока нет

- Wind Power or Wind Energy Is The Use ofДокумент1 страницаWind Power or Wind Energy Is The Use ofelbronОценок пока нет

- Philosophy (From: Philosopher Mathematical Principles of Natural PhilosophyДокумент1 страницаPhilosophy (From: Philosopher Mathematical Principles of Natural PhilosophyelbronОценок пока нет

- SubtractionДокумент1 страницаSubtractionelbronОценок пока нет

- Tagalog Song Lyrics: PasensyaДокумент1 страницаTagalog Song Lyrics: PasensyaelbronОценок пока нет

- Solar EnergyДокумент1 страницаSolar EnergySHARON GARCIA PUENTESОценок пока нет

- HW4 Lit110Документ1 страницаHW4 Lit110elbronОценок пока нет

- SubtractionДокумент1 страницаSubtractionelbronОценок пока нет

- ACLC CutesДокумент1 страницаACLC CutesnnaemzОценок пока нет

- Notes From ReadingsДокумент5 страницNotes From ReadingselbronОценок пока нет

- Grade: 1. 2. 3. 4. 5. 6. 7. 8. 9. Salvanera, Pinky T. EE101L/B7 2014141532Документ11 страницGrade: 1. 2. 3. 4. 5. 6. 7. 8. 9. Salvanera, Pinky T. EE101L/B7 2014141532elbronОценок пока нет

- Experiment 4. ProcedureДокумент2 страницыExperiment 4. ProcedureelbronОценок пока нет

- DocxДокумент5 страницDocxelbronОценок пока нет

- DocxДокумент5 страницDocxelbronОценок пока нет

- EE21L Experiment 6 1.1Документ9 страницEE21L Experiment 6 1.1Filbert SaavedraОценок пока нет

- EE21L Experiment 6 1.1Документ9 страницEE21L Experiment 6 1.1Filbert SaavedraОценок пока нет

- Grade: 1. 2. 3. 4. 5. 6. 7. 8. 9. Salvanera, Pinky T. EE101L/B7 2014141532Документ11 страницGrade: 1. 2. 3. 4. 5. 6. 7. 8. 9. Salvanera, Pinky T. EE101L/B7 2014141532elbronОценок пока нет

- The Art of Japanese Candlestick Charting Summary PDFДокумент24 страницыThe Art of Japanese Candlestick Charting Summary PDFelbronОценок пока нет

- Stock Market Basics - InvestopediaДокумент26 страницStock Market Basics - InvestopediaLaurence MorenoОценок пока нет

- How To Pick Winning Stock (Martin Zweig) : 1.0 Acting Better - Avoid Stocks 2.0 Clear UptrendДокумент2 страницыHow To Pick Winning Stock (Martin Zweig) : 1.0 Acting Better - Avoid Stocks 2.0 Clear UptrendJohn Dennis TijamОценок пока нет

- Math Project ProblemsДокумент2 страницыMath Project ProblemselbronОценок пока нет

- Spot The DifferenceДокумент16 страницSpot The DifferenceelbronОценок пока нет

- COL Technical Analysis (Part 1)Документ36 страницCOL Technical Analysis (Part 1)Glenzo Jaye Pigao Daroy100% (1)

- COL A Primer Into TAДокумент45 страницCOL A Primer Into TAJunar AmaroОценок пока нет

- Kahoot Trivia Questions. (Answers Are Highlighted)Документ7 страницKahoot Trivia Questions. (Answers Are Highlighted)elbronОценок пока нет

- Eco402 Collection of Old PapersДокумент37 страницEco402 Collection of Old Paperscs619finalproject.com100% (2)

- self+destructive+habits+TheSmartManager,+JagdishSeth,+Jun-Jul+07 412Документ12 страницself+destructive+habits+TheSmartManager,+JagdishSeth,+Jun-Jul+07 412Nabendu BhaumikОценок пока нет

- Corporate Law MGT-513: ARSHAD ISLAM Lecturer City University Peshawar PakistamДокумент9 страницCorporate Law MGT-513: ARSHAD ISLAM Lecturer City University Peshawar PakistamArshad IslamОценок пока нет

- Acctg BasicsДокумент41 страницаAcctg BasicsLara Lewis AchillesОценок пока нет

- Alasdair Macleod Sound Money 555Документ5 страницAlasdair Macleod Sound Money 555Kevin CreaseyОценок пока нет

- Industry Analysis AXIS BANKДокумент13 страницIndustry Analysis AXIS BANKEric D'souza0% (1)

- Shift The Focus From The Super-Poor To The Super-Rich (Otto, 2019)Документ3 страницыShift The Focus From The Super-Poor To The Super-Rich (Otto, 2019)CliffhangerОценок пока нет

- Chapter 4 (James C.Van Horne)Документ63 страницыChapter 4 (James C.Van Horne)Maaz SheikhОценок пока нет

- Portfolio Composition and Backtesting: Dakota WixomДокумент34 страницыPortfolio Composition and Backtesting: Dakota WixomGedela BharadwajОценок пока нет

- AS 37 (IAS Plus)Документ6 страницAS 37 (IAS Plus)SarmadОценок пока нет

- Conservative Mutual Funds AssessmentДокумент24 страницыConservative Mutual Funds AssessmentRula Abu NuwarОценок пока нет

- Practice Questions For AMFI TestДокумент41 страницаPractice Questions For AMFI TestanupОценок пока нет

- The Investment Detective PDFДокумент2 страницыThe Investment Detective PDFAroosa KhawajaОценок пока нет

- Shil and DasДокумент8 страницShil and Dasbhagaban_fm8098Оценок пока нет

- Sacco Societies Act 2008Документ32 страницыSacco Societies Act 2008elinzolaОценок пока нет

- Unlocking The Power of IMC - Keller 2016Документ17 страницUnlocking The Power of IMC - Keller 2016Jocelyn SabandoОценок пока нет

- CapitalGain Summary Report - 1658151067650 - 11Документ1 страницаCapitalGain Summary Report - 1658151067650 - 11honey mittalОценок пока нет

- Netflix FinancialsДокумент39 страницNetflix Financialsakram balochОценок пока нет

- CF 26051Документ20 страницCF 26051sdfdsfОценок пока нет

- Portfolio RevisionДокумент14 страницPortfolio RevisionchitkarashellyОценок пока нет

- Guidance Note (Mat)Документ6 страницGuidance Note (Mat)Cma Saurabh AroraОценок пока нет

- Ordinary Share CapitalДокумент7 страницOrdinary Share CapitalKenneth RonoОценок пока нет

- Apple's Supply-Chain Secret? Hoard LasersДокумент13 страницApple's Supply-Chain Secret? Hoard LasersBirte ReiterОценок пока нет

- Shirkah and Its Variant SummaryДокумент4 страницыShirkah and Its Variant SummaryOmayr QureshiОценок пока нет

- Ratio Analysis LenovoДокумент3 страницыRatio Analysis LenovoAbdy ShahОценок пока нет