Вам также может понравиться

- Financial Accounting AnalysisДокумент11 страницFinancial Accounting AnalysisRajni KumariОценок пока нет

- Golden Rules For Debit and CreditДокумент5 страницGolden Rules For Debit and CreditSharjeel 77Оценок пока нет

- Financial Accounting AnalysisДокумент10 страницFinancial Accounting AnalysisRohit GangurdeОценок пока нет

- Financial Accounting & Analysis - N (1A)Документ10 страницFinancial Accounting & Analysis - N (1A)Tajinder MatharuОценок пока нет

- Financial Accounting AnalysisДокумент12 страницFinancial Accounting AnalysisSamyak GargОценок пока нет

- Financial Accounting & Analysis June 2021 ExaminationДокумент9 страницFinancial Accounting & Analysis June 2021 ExaminationJayant MendevellОценок пока нет

- Financial Accounting & AnalysisДокумент10 страницFinancial Accounting & AnalysisLucky SinghОценок пока нет

- Sample - Financial-Accounting-Analysis-V-ST-8cjfveДокумент11 страницSample - Financial-Accounting-Analysis-V-ST-8cjfvesushainkapoor photoОценок пока нет

- Financial Accounting and Analysis AssignmentДокумент10 страницFinancial Accounting and Analysis AssignmentRahul RJОценок пока нет

- Debit and Credit Rules of AccountingДокумент6 страницDebit and Credit Rules of AccountingsbcluincОценок пока нет

- Accounting For Receivables Accounts ReceivableДокумент18 страницAccounting For Receivables Accounts Receivablelocomotingkenya.co.keОценок пока нет

- Accounts FinalДокумент10 страницAccounts FinalNeha PОценок пока нет

- Basic Accounting EquationДокумент3 страницыBasic Accounting EquationMaria Charise TongolОценок пока нет

- Financial Accounting and AnalysisДокумент6 страницFinancial Accounting and AnalysistanmayОценок пока нет

- Class 11 Accountancy Chapter-3 Revision NotesДокумент11 страницClass 11 Accountancy Chapter-3 Revision NotesMohd. Khushmeen KhanОценок пока нет

- Financial Accounting and AnalysisДокумент5 страницFinancial Accounting and Analysissumit86Оценок пока нет

- Financial AccountingДокумент8 страницFinancial AccountingHimani SachdevОценок пока нет

- The Effect of Profit or Loss On Capital and The Double Entry System For Expenses and RevenueДокумент35 страницThe Effect of Profit or Loss On Capital and The Double Entry System For Expenses and Revenueshabanzuhura706Оценок пока нет

- TДокумент6 страницTAgatha GomezОценок пока нет

- Accounting Information and Financial StatementsДокумент5 страницAccounting Information and Financial StatementsJay GadОценок пока нет

- Journal Entries Example PDFДокумент6 страницJournal Entries Example PDFshlokshah2006Оценок пока нет

- Journal Entries ExamplesДокумент9 страницJournal Entries Examplesmoon_mohi50% (2)

- Accounting Period and Accounting EquationДокумент19 страницAccounting Period and Accounting EquationsptaraОценок пока нет

- Balance Sheet: Prof. K.C. AroraДокумент52 страницыBalance Sheet: Prof. K.C. Aroraitikat_86Оценок пока нет

- Journal Entries The Rules of Double Entries Purchase Sale Transactions Accounting AccountДокумент8 страницJournal Entries The Rules of Double Entries Purchase Sale Transactions Accounting AccountirishjadeОценок пока нет

- Accounting Notes: Double Entry BookkeepingДокумент19 страницAccounting Notes: Double Entry Bookkeepingkashmala HussainОценок пока нет

- Lesson 3 - Mechanics of AccountingДокумент34 страницыLesson 3 - Mechanics of AccountingYogesh KumarОценок пока нет

- Financial Accounting & AnalysisДокумент7 страницFinancial Accounting & AnalysisMitaliОценок пока нет

- College of Administrative and Financial Sciences: Instructions - Please Read Them CarefullyДокумент8 страницCollege of Administrative and Financial Sciences: Instructions - Please Read Them CarefullymoonbohoraОценок пока нет

- Double Entry SystemДокумент17 страницDouble Entry Systemhansali diasОценок пока нет

- MGT101 Solved Subjective Question Question No: 49 (Marks: 3)Документ22 страницыMGT101 Solved Subjective Question Question No: 49 (Marks: 3)baniОценок пока нет

- Acc EqДокумент5 страницAcc EqBianca BgnОценок пока нет

- AccountsДокумент4 страницыAccountsPranshu BansalОценок пока нет

- 2 Accounting Equestion and Double Entry UDДокумент10 страниц2 Accounting Equestion and Double Entry UDERICK MLINGWAОценок пока нет

- Accounts ReceivableДокумент21 страницаAccounts ReceivableMurtaza Hussain SyedОценок пока нет

- 1.3 Accounting EquationДокумент6 страниц1.3 Accounting EquationTvet AcnОценок пока нет

- 11 Concepts of Accounting (Hashi)Документ9 страниц11 Concepts of Accounting (Hashi)mohamedОценок пока нет

- Debit Credit RulesДокумент9 страницDebit Credit RulesMubeen JavedОценок пока нет

- Accounting For DebenturesДокумент13 страницAccounting For DebenturesDivisha AgarwalОценок пока нет

- Financial Statements: Instructor Dr. Jagan Kumar SurДокумент48 страницFinancial Statements: Instructor Dr. Jagan Kumar SurBabusona SahaОценок пока нет

- 2 Accounting Equestion and Double EntryДокумент10 страниц2 Accounting Equestion and Double EntryAlex MaugoОценок пока нет

- Chap 3 Accounting Classification & Equation (Basic+Expended) - ClassДокумент37 страницChap 3 Accounting Classification & Equation (Basic+Expended) - Classnabkill100% (1)

- TransactionДокумент2 страницыTransactionYuKiNa Hymns-Acheron100% (1)

- Refundable DepositsДокумент1 страницаRefundable DepositsNicah AcojonОценок пока нет

- Adjusting EntriesДокумент3 страницыAdjusting EntriesMarini HernandezОценок пока нет

- Conceptual RevisionДокумент1 страницаConceptual RevisionNimra MerajОценок пока нет

- Journal Ledger & Trial BalanceДокумент11 страницJournal Ledger & Trial BalanceTushar SahuОценок пока нет

- Question No 1Документ3 страницыQuestion No 1knvs sivakumarОценок пока нет

- Exam Revision - 9 & 10 SolДокумент7 страницExam Revision - 9 & 10 SolNguyễn Minh ĐứcОценок пока нет

- Accounting Principles 1Документ27 страницAccounting Principles 1shaza jocarlos100% (1)

- 68633240042Документ3 страницы68633240042rooneyboyy6Оценок пока нет

- Financial Accounting BasicsДокумент4 страницыFinancial Accounting BasicsDemoОценок пока нет

- Important Concepts ExplainedДокумент4 страницыImportant Concepts ExplainedRamanaОценок пока нет

- Recording in The Journals or JournalizingДокумент6 страницRecording in The Journals or JournalizingMardy DahuyagОценок пока нет

- Chapter 5Документ6 страницChapter 5mardyjanedahuyagОценок пока нет

- Exam Revision - Chapter 9 10Документ7 страницExam Revision - Chapter 9 10Vũ Thị NgoanОценок пока нет

- Debentures: 1.objectivesДокумент15 страницDebentures: 1.objectivesharishОценок пока нет

- Financial Accounting & AnalysisДокумент7 страницFinancial Accounting & Analysisneha bakshiОценок пока нет

- Accounting and Financial StatementДокумент5 страницAccounting and Financial StatementGordon SmithОценок пока нет

- Tusk Investments - Case Study (Round 1) - Metals and MiningДокумент9 страницTusk Investments - Case Study (Round 1) - Metals and MiningdebojyotiОценок пока нет

- S7 BuiltinFunctions StartДокумент9 страницS7 BuiltinFunctions StartdebojyotiОценок пока нет

- Candito Deadlift Program: What Date Do You Want To Start The Program?Документ16 страницCandito Deadlift Program: What Date Do You Want To Start The Program?Nishant GuptaОценок пока нет

- Activity Description Activity Symbol Preceeding Activity Completion Times (In Weeks)Документ2 страницыActivity Description Activity Symbol Preceeding Activity Completion Times (In Weeks)debojyotiОценок пока нет

- Project Assessment at Railways FinalДокумент5 страницProject Assessment at Railways FinaldebojyotiОценок пока нет

- Ferrous Metals - Elara Securities - 20 January 2021Документ43 страницыFerrous Metals - Elara Securities - 20 January 2021debojyotiОценок пока нет

- TOPSISДокумент1 страницаTOPSISdebojyotiОценок пока нет

- NBFCs and Their Regulation - ClassДокумент8 страницNBFCs and Their Regulation - ClassdebojyotiОценок пока нет

- Examples Bank BalancesheetДокумент3 страницыExamples Bank BalancesheetdebojyotiОценок пока нет

- Financial Services (FS) Instructor: Golaka C Nath, PH.D.: Overview of The CourseДокумент3 страницыFinancial Services (FS) Instructor: Golaka C Nath, PH.D.: Overview of The CoursedebojyotiОценок пока нет

- Volcker Rule: What Is It?Документ2 страницыVolcker Rule: What Is It?debojyotiОценок пока нет

- Leveraged Leasing Hardware Leasing Company Data:: PV of Net Lease Receipts $88,606Документ2 страницыLeveraged Leasing Hardware Leasing Company Data:: PV of Net Lease Receipts $88,606debojyotiОценок пока нет

- IIM Sambalpur ExampleДокумент2 страницыIIM Sambalpur ExampledebojyotiОценок пока нет

- Excel 18Документ11 страницExcel 18debojyotiОценок пока нет

- Assets, Liabilities, and The Balance SheetДокумент19 страницAssets, Liabilities, and The Balance Sheetdebojyoti100% (1)

- Chapter - 8 Foreign Exchange Forwards and Futures: Example 8.1Документ40 страницChapter - 8 Foreign Exchange Forwards and Futures: Example 8.1debojyotiОценок пока нет

- Chapter - 13 Options On Stock Indexes, Foreign Currencies, Futures Contracts, and Volatility IndexesДокумент49 страницChapter - 13 Options On Stock Indexes, Foreign Currencies, Futures Contracts, and Volatility IndexesdebojyotiОценок пока нет

- Excel 19Документ6 страницExcel 19debojyotiОценок пока нет

- Company - Swiggy Position - AnalyticsДокумент1 страницаCompany - Swiggy Position - AnalyticsdebojyotiОценок пока нет

- George Soros and His Speculative Activities: Assignment OnДокумент3 страницыGeorge Soros and His Speculative Activities: Assignment OndebojyotiОценок пока нет

- List of GIC CompaniesДокумент49 страницList of GIC Companiesdebojyoti91% (35)

- Assignment On India's Current Account DeficitДокумент6 страницAssignment On India's Current Account DeficitdebojyotiОценок пока нет

- Recommendation Rough SketchДокумент4 страницыRecommendation Rough SketchdebojyotiОценок пока нет

- Isc Report1c 1314Документ33 страницыIsc Report1c 1314Rajanna JadiОценок пока нет

- Natixis Global Asset ManagementДокумент26 страницNatixis Global Asset ManagementAlezNgОценок пока нет

- f7 Mock QuestionДокумент20 страницf7 Mock Questionnoor ul anumОценок пока нет

- Key Features: A Oke9Wjwm36Onlmr&Redirect Signup A Oke9Wjwm36OnlmrДокумент5 страницKey Features: A Oke9Wjwm36Onlmr&Redirect Signup A Oke9Wjwm36OnlmrVicard GibbingsОценок пока нет

- Beginning InventoryДокумент10 страницBeginning InventoryMegersa DinsaОценок пока нет

- LT E-BillДокумент2 страницыLT E-Billsarika25Оценок пока нет

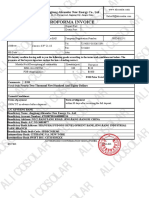

- Alicosolar Proforma Invoice For AS450WДокумент1 страницаAlicosolar Proforma Invoice For AS450WAngie GuerreroОценок пока нет

- Ghana Commercial BankДокумент1 страницаGhana Commercial Bankapi-3728882100% (2)

- Corporate Finance 3rd Edition by Berk DeMarzo ISBN Test BankДокумент38 страницCorporate Finance 3rd Edition by Berk DeMarzo ISBN Test Bankcarl100% (24)

- SasДокумент9 страницSasShubham Prabhat SakyaОценок пока нет

- A Study On Customer's Preference While Investing in Systematic Investment PlanДокумент11 страницA Study On Customer's Preference While Investing in Systematic Investment PlanK C ChandanОценок пока нет

- Audit of Insurance CompaniesДокумент15 страницAudit of Insurance CompaniesYoung MetroОценок пока нет

- Zurich Captive Guide 2022Документ39 страницZurich Captive Guide 2022david.russellОценок пока нет

- MATH 108X - Savings & Loans Project (Vehicle Option)Документ25 страницMATH 108X - Savings & Loans Project (Vehicle Option)Boy of SteelОценок пока нет

- Module 1, Assessment 1Документ31 страницаModule 1, Assessment 1praveena100% (2)

- Turkey: Country Specific FeaturesДокумент12 страницTurkey: Country Specific FeaturesUdayraj SinghОценок пока нет

- Detail Project Report For The Medical College With Teaching HospitalДокумент5 страницDetail Project Report For The Medical College With Teaching HospitalSuresh SharmaОценок пока нет

- AAC Seeded ControlsДокумент8 страницAAC Seeded ControlsvenkkatmandulaОценок пока нет

- 11 Accounts 2Документ183 страницы11 Accounts 2Sai BhargavОценок пока нет

- The Scope of Marine InsuranceДокумент4 страницыThe Scope of Marine InsuranceseaguyinОценок пока нет

- Five Common Investing Mistakes To AvoidДокумент3 страницыFive Common Investing Mistakes To AvoidjanivarunОценок пока нет

- HSBC - Personal Banking Agreement en PDFДокумент52 страницыHSBC - Personal Banking Agreement en PDFRuslan ParisОценок пока нет

- Script Financial LiteracyДокумент6 страницScript Financial LiteracyAngelica AruyalОценок пока нет

- Tutorial Investment PropertiesДокумент3 страницыTutorial Investment Propertiesnadya bujangОценок пока нет

- Ujjivan SFB Analyst Day 9jun23Документ6 страницUjjivan SFB Analyst Day 9jun23Sharath JuturОценок пока нет

- M/s Rishabh Creations Sikka Knitting FabДокумент1 страницаM/s Rishabh Creations Sikka Knitting FabVarun AgarwalОценок пока нет

- P3 Pertemuan 3Документ8 страницP3 Pertemuan 3Ahsan FirdausОценок пока нет

- Financial Management:: Firms and The Financial MarketДокумент53 страницыFinancial Management:: Firms and The Financial MarketArgem Jay PorioОценок пока нет

- Banking Regulation Act 1949Документ13 страницBanking Regulation Act 1949jhumli0% (1)

- DRHP AimlДокумент636 страницDRHP AimlSubscriptionОценок пока нет