Вам также может понравиться

- Decoding Tomorrow's Currency: An In-Depth Exploration of the Future of CryptocurrencyОт EverandDecoding Tomorrow's Currency: An In-Depth Exploration of the Future of CryptocurrencyОценок пока нет

- Bitcoin PDFДокумент59 страницBitcoin PDFheshanОценок пока нет

- Crypto ProjectДокумент7 страницCrypto Projectshekarpenthala123Оценок пока нет

- Chiu PaperДокумент60 страницChiu PaperUmar Farouq Mohammed GalibОценок пока нет

- Bitcoin - Review of LiteratureДокумент9 страницBitcoin - Review of LiteratureNeha ChhabdaОценок пока нет

- Bitcoin - Review of LiteratureДокумент27 страницBitcoin - Review of LiteratureNeha ChhabdaОценок пока нет

- ContentServer PDF (Biblio2)Документ17 страницContentServer PDF (Biblio2)Pri MarinkovicОценок пока нет

- A Novel Cryptocurrency Price Prediction Model Using GRU, LSTM and bi-LSTM Machine Learning AlgorithmsДокумент20 страницA Novel Cryptocurrency Price Prediction Model Using GRU, LSTM and bi-LSTM Machine Learning Algorithmsjaya prakash KoduruОценок пока нет

- Equilibrium PriceДокумент40 страницEquilibrium PricemanbotoОценок пока нет

- V14i4016 PDFДокумент7 страницV14i4016 PDF573 Sai Charan LahiriОценок пока нет

- Cryptocurrency - A New Investment OpportunityДокумент26 страницCryptocurrency - A New Investment OpportunityMohd. Anisul IslamОценок пока нет

- M A Thesis Anon PDFДокумент41 страницаM A Thesis Anon PDFMitchell WRОценок пока нет

- Electronics 11 04088 v2Документ18 страницElectronics 11 04088 v2Tallha AzizОценок пока нет

- Electronics 11 02349 v2Документ22 страницыElectronics 11 02349 v2alperen.unal89Оценок пока нет

- Paper TsFKfa85Документ17 страницPaper TsFKfa85Hakim ThumОценок пока нет

- Karels, Racole (Cryptocurrencies and The Economy) Capstone 201718Документ21 страницаKarels, Racole (Cryptocurrencies and The Economy) Capstone 201718saquibkazi55Оценок пока нет

- Cryptocurrencies: The Revolution in The World Finance: Sanjeev Kumar Joshi, Nitesh Khatiwada, Jyoti GiriДокумент12 страницCryptocurrencies: The Revolution in The World Finance: Sanjeev Kumar Joshi, Nitesh Khatiwada, Jyoti GirimaryamОценок пока нет

- Network Analysis On Bitcoin Arbitrage OpportunitiesДокумент16 страницNetwork Analysis On Bitcoin Arbitrage OpportunitiesLeandro Aparecido LopesОценок пока нет

- Forecasting Bitcoin Price Using Deep Learning AlgorithmДокумент7 страницForecasting Bitcoin Price Using Deep Learning AlgorithmIJRASETPublicationsОценок пока нет

- A Novel Method For Prediction of Cryptocurrency PriceДокумент7 страницA Novel Method For Prediction of Cryptocurrency PriceIJRASETPublicationsОценок пока нет

- Crypto Currency Forecasting Using Deep LearningДокумент6 страницCrypto Currency Forecasting Using Deep LearningKrios143Оценок пока нет

- Cryptocurrencies: The Revolution in The World Finance: Sanjeev Kumar Joshi, Nitesh Khatiwada, Jyoti GiriДокумент9 страницCryptocurrencies: The Revolution in The World Finance: Sanjeev Kumar Joshi, Nitesh Khatiwada, Jyoti GirimaryamОценок пока нет

- The Effect of Us Monetary Policy Shocks On Cryptocurrency ReturnsДокумент25 страницThe Effect of Us Monetary Policy Shocks On Cryptocurrency ReturnsAIRDROP COINОценок пока нет

- Master Thesis Bitcoin As Asset or Currency Preliminary Draft More Detail About El SalvadorДокумент46 страницMaster Thesis Bitcoin As Asset or Currency Preliminary Draft More Detail About El SalvadordanielОценок пока нет

- Crypto PDFДокумент39 страницCrypto PDFBambang Riyadi AriekОценок пока нет

- العملات الافتراضية - تقارير بنك التوسيات الدولى BISДокумент6 страницالعملات الافتراضية - تقارير بنك التوسيات الدولى BISWael HassanОценок пока нет

- Bitcoin As Decentralized Money: Prices, Mining, and Network SecurityДокумент78 страницBitcoin As Decentralized Money: Prices, Mining, and Network SecurityJhОценок пока нет

- Cryptocurrencies and The Future of Money: Mcmaster University, Hamilton, Canada Mit, Cambridge, UsaДокумент22 страницыCryptocurrencies and The Future of Money: Mcmaster University, Hamilton, Canada Mit, Cambridge, UsaAtul MhatreОценок пока нет

- Antonakakis Et Al Cryptocurrency Market ContagionДокумент15 страницAntonakakis Et Al Cryptocurrency Market ContagionSaul BerrisОценок пока нет

- Chubitcoinatheoreticalanalysisofmoneychoice 0Документ28 страницChubitcoinatheoreticalanalysisofmoneychoice 0DylanОценок пока нет

- Crypto IntroДокумент11 страницCrypto IntroFY MicroОценок пока нет

- Corbet 2017Документ18 страницCorbet 2017BradОценок пока нет

- Fundamental Analysis of Price Fluctuations: A Case Study of 2019-2020)Документ12 страницFundamental Analysis of Price Fluctuations: A Case Study of 2019-2020)Rendy FrancescoОценок пока нет

- Factors Influencing Cryptocurrency Prices: Evidence From Bitcoin, Ethereum, Dash, Litcoin, and MoneroДокумент28 страницFactors Influencing Cryptocurrency Prices: Evidence From Bitcoin, Ethereum, Dash, Litcoin, and MoneroshakilanepaliОценок пока нет

- Cryptocurrency: Ingolf G. A. Pernice Brett ScottДокумент10 страницCryptocurrency: Ingolf G. A. Pernice Brett ScottNguyen TungОценок пока нет

- White Paper Chain X 1Документ20 страницWhite Paper Chain X 1Ishan PandeyОценок пока нет

- Cryptocurrency: A New Investment Opportunity?: SSRN Electronic Journal January 2017Документ26 страницCryptocurrency: A New Investment Opportunity?: SSRN Electronic Journal January 2017StefanoОценок пока нет

- How To Value Payment Tokens 0.5. v2Документ14 страницHow To Value Payment Tokens 0.5. v2Distro MusicОценок пока нет

- Mini Project Synopsis PPT FinalДокумент21 страницаMini Project Synopsis PPT FinalSaran AgarwalОценок пока нет

- Reserch Paper BitДокумент6 страницReserch Paper Bitpratiknavale1131Оценок пока нет

- Tokenomics - Dynamic Adoption and ValuationДокумент46 страницTokenomics - Dynamic Adoption and ValuationetooskimОценок пока нет

- The Crypto Effect On Cross Border Transfers and Future Trends of CryptocurrenciesДокумент12 страницThe Crypto Effect On Cross Border Transfers and Future Trends of CryptocurrenciesKasia AdamskaОценок пока нет

- Bondar - Stablecoins From Electronic Money On Blockchain To A Cryptocurrency Basket PDFДокумент97 страницBondar - Stablecoins From Electronic Money On Blockchain To A Cryptocurrency Basket PDFДмитрий БондарьОценок пока нет

- Literature Review 3Документ36 страницLiterature Review 3Amit KumarОценок пока нет

- Factors Influencing Cryptocurrency Prices: Evidence From Bitcoin, Ethereum, Dash, Litcoin, and MoneroДокумент28 страницFactors Influencing Cryptocurrency Prices: Evidence From Bitcoin, Ethereum, Dash, Litcoin, and MoneroFika JeОценок пока нет

- International Journal of Forecasting: Wei Chen, Huilin Xu, Lifen Jia, Ying GaoДокумент16 страницInternational Journal of Forecasting: Wei Chen, Huilin Xu, Lifen Jia, Ying GaoJanko DiminićОценок пока нет

- How To Design Cryptocurrency Value and How To Secure Its Sustainability in The MarketДокумент12 страницHow To Design Cryptocurrency Value and How To Secure Its Sustainability in The Marketm_vamshikrishna22Оценок пока нет

- Very ImpДокумент12 страницVery Impm_vamshikrishna22Оценок пока нет

- ISJBCДокумент12 страницISJBCAlex-samaОценок пока нет

- Cryptocurrency: Internet Policy Review May 2021Документ10 страницCryptocurrency: Internet Policy Review May 2021tina afsharОценок пока нет

- Improving The Cryptocurrency Price Prediction Performance Based On Reinforcement LearningДокумент9 страницImproving The Cryptocurrency Price Prediction Performance Based On Reinforcement LearningharshinigonuguntlaОценок пока нет

- Algorithms 15 00230Документ13 страницAlgorithms 15 00230ilkerОценок пока нет

- Block Chain Technology Assignment On Crypto EconomicsДокумент4 страницыBlock Chain Technology Assignment On Crypto EconomicsFATHIMA ZAHRA 1610326Оценок пока нет

- The Effect of Cryptocurrency On InvestmeДокумент10 страницThe Effect of Cryptocurrency On InvestmePradeepОценок пока нет

- Brianperrycarrera DjeДокумент41 страницаBrianperrycarrera DjeTallha AzizОценок пока нет

- 2020 Using On Chain and Market Metrics To Analyse The Value of Crypto AssetsДокумент22 страницы2020 Using On Chain and Market Metrics To Analyse The Value of Crypto AssetsAhsan RazaОценок пока нет

- CRYPTOCURRENCYДокумент18 страницCRYPTOCURRENCYShravani AnemiОценок пока нет

- Assignment 8Документ4 страницыAssignment 8Alberto Jr. AguirreОценок пока нет

- The Crypto Revolution: A Guide to Building Wealth with CryptocurrenciesОт EverandThe Crypto Revolution: A Guide to Building Wealth with CryptocurrenciesОценок пока нет

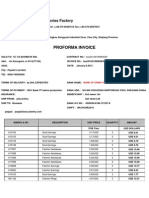

- Proforma Invoice: China Asu Fashion Accessories FactoryДокумент5 страницProforma Invoice: China Asu Fashion Accessories FactorySilviu GurbanescuОценок пока нет

- Servicenow q3 2022 Investor PresentationДокумент25 страницServicenow q3 2022 Investor Presentationstan LeeОценок пока нет

- SBM QuestionsДокумент148 страницSBM QuestionsGeorge NicholsonОценок пока нет

- Banana VCin Ethiopia AsmiroДокумент11 страницBanana VCin Ethiopia AsmirovipinОценок пока нет

- How To Survive The Collapse of CivilizationДокумент126 страницHow To Survive The Collapse of CivilizationDaniel100% (1)

- English For Students of EconomicsДокумент217 страницEnglish For Students of EconomicsSayed Farhad QattaliОценок пока нет

- Cancel Credit Card Debt / Defeat TaxesДокумент96 страницCancel Credit Card Debt / Defeat TaxesXR500Final100% (24)

- 2021 Annual Economic Survey 20220605 PDFДокумент148 страниц2021 Annual Economic Survey 20220605 PDFRiannaОценок пока нет

- Bill Already Paid in Full LetterДокумент8 страницBill Already Paid in Full LetterRoberto Monterrosa97% (58)

- Multinational Accounting: Foreign Currency Transactions and Financial InstrumentsДокумент29 страницMultinational Accounting: Foreign Currency Transactions and Financial InstrumentsBelatrix LestrangeОценок пока нет

- Monetary Policy1.2Документ567 страницMonetary Policy1.2Eric GarrisОценок пока нет

- Analysis of Glencore Xstrata's Sale of The Las Bambas Copper ProjectДокумент4 страницыAnalysis of Glencore Xstrata's Sale of The Las Bambas Copper ProjectFraserОценок пока нет

- BB Cost of Mba Report 2022 PDFДокумент17 страницBB Cost of Mba Report 2022 PDFNfaОценок пока нет

- First Division Engr. Jose E. Cayanan, G.R. No. 172954: ChairpersonДокумент4 страницыFirst Division Engr. Jose E. Cayanan, G.R. No. 172954: ChairpersonJaysieMicabaloОценок пока нет

- Baur, McDermott (2010) - Is Gold A Safe Haven - International EvidenceДокумент13 страницBaur, McDermott (2010) - Is Gold A Safe Haven - International EvidencefrechekroeteОценок пока нет

- Q.12-Allow Multi-Currency in TallyДокумент4 страницыQ.12-Allow Multi-Currency in TallySrinivas RaoОценок пока нет

- Chapter 12: Derivatives and Foreign Currency Transactions: Advanced AccountingДокумент52 страницыChapter 12: Derivatives and Foreign Currency Transactions: Advanced AccountingindahmuliasariОценок пока нет

- Exorbitant Pillage by Martin ZamyatinДокумент2 страницыExorbitant Pillage by Martin ZamyatinSamsara ChomolungmaОценок пока нет

- Tourism NSC QP Sept 2022 EngДокумент28 страницTourism NSC QP Sept 2022 Eng9c696qbzngОценок пока нет

- Workshop 1 - Maths - March 20Документ12 страницWorkshop 1 - Maths - March 20Julieth CaviativaОценок пока нет

- Part I Kris Matthews The Gestalt ShiftДокумент12 страницPart I Kris Matthews The Gestalt ShiftOlamide Afolabi AyodejiОценок пока нет

- UNOPS Grant AgreementДокумент14 страницUNOPS Grant Agreementhb proposalОценок пока нет

- Money As Debt 2 TranscriptДокумент34 страницыMoney As Debt 2 Transcriptjoedoe1Оценок пока нет

- Problem 19.1 Trefica de Honduras: Assumptions ValuesДокумент2 страницыProblem 19.1 Trefica de Honduras: Assumptions ValueskamlОценок пока нет

- Material 2. Writing A Synthesis Essay. Behrens, Rosen - pp.120-134Документ15 страницMaterial 2. Writing A Synthesis Essay. Behrens, Rosen - pp.120-134George MujiriОценок пока нет

- International Monetary SystemДокумент25 страницInternational Monetary SystemMahin Mahmood33% (3)

- Sep 05, 2023 10:34 AM MDT: Recipient: Taha Latif Transfer No.: R64 671 118 382Документ4 страницыSep 05, 2023 10:34 AM MDT: Recipient: Taha Latif Transfer No.: R64 671 118 382otisstillwell55Оценок пока нет

- Module 10 InflationДокумент10 страницModule 10 InflationRhonita Dea AndariniОценок пока нет

- PayPal Website Payment Details - PayPal LentesДокумент2 страницыPayPal Website Payment Details - PayPal LentesDionis VenturaОценок пока нет

- Abandonment and Site Restoration (ASR) ReservationДокумент7 страницAbandonment and Site Restoration (ASR) Reservationnanda berkahОценок пока нет