Вам также может понравиться

- Feasibility Study and Risk AssesmentДокумент6 страницFeasibility Study and Risk AssesmentSanjayОценок пока нет

- TCS Project HRMДокумент36 страницTCS Project HRMAnonymous bPjBn5LxNОценок пока нет

- MBA ProjectДокумент63 страницыMBA Projectsreddy68Оценок пока нет

- Marketing Management - TruEarth Health Foods CaseДокумент6 страницMarketing Management - TruEarth Health Foods Casesmithmelina100% (2)

- Consumer Buying Behaviour of Tata MotorsДокумент55 страницConsumer Buying Behaviour of Tata MotorsAnkit Sharma0% (1)

- Chapter: 2. Creation of New Ventures: Entrepreneurship For EngineersДокумент11 страницChapter: 2. Creation of New Ventures: Entrepreneurship For EngineersAbdulhakim BushraОценок пока нет

- IT InfrastructureДокумент11 страницIT Infrastructurefahri kurniawanОценок пока нет

- Jade Globals Hi Tech Industry SolutionsДокумент3 страницыJade Globals Hi Tech Industry SolutionsSapna SoniОценок пока нет

- Ayush STPR Report Complete 1Документ85 страницAyush STPR Report Complete 1sanjeev sam50% (2)

- SAP IS Blue Print DocumentДокумент4 страницыSAP IS Blue Print DocumentSupriyo DuttaОценок пока нет

- T3TMD - Miscellaneous Deals - R10Документ78 страницT3TMD - Miscellaneous Deals - R10KLB USERОценок пока нет

- TOGAF 9.1 - Level 1 and 2 Student Handbook - ITpreneurs PDFДокумент64 страницыTOGAF 9.1 - Level 1 and 2 Student Handbook - ITpreneurs PDFZain AtifОценок пока нет

- IoT Forrester Wave IoT Software Platforms November 2016Документ19 страницIoT Forrester Wave IoT Software Platforms November 2016Ivan Kuraj100% (1)

- Employees Satisfaction and Quality of Work Life at Tata SteelДокумент84 страницыEmployees Satisfaction and Quality of Work Life at Tata SteelSwati Sharma100% (5)

- Mastering The Industrial Internet of Things (Iiot)Документ16 страницMastering The Industrial Internet of Things (Iiot)Sowmya KoneruОценок пока нет

- A Project ReportДокумент85 страницA Project ReportHCL22211160% (5)

- Project Report On Employee Participation On Business DevelopmentДокумент94 страницыProject Report On Employee Participation On Business DevelopmentRoyal ProjectsОценок пока нет

- Recruitment & Selection Reliance Jio Full Report - 100 Page MANU SHARMA MBA 3rd SEMДокумент102 страницыRecruitment & Selection Reliance Jio Full Report - 100 Page MANU SHARMA MBA 3rd SEMImpression Graphics100% (3)

- Information Sheet: Lending Company - Head OfficeДокумент4 страницыInformation Sheet: Lending Company - Head OfficesakilogicОценок пока нет

- BSBMGT608 Student Assessment Tasks 2020Документ45 страницBSBMGT608 Student Assessment Tasks 2020Chirayu ManandharОценок пока нет

- Food Safety Culture Module BrochureДокумент8 страницFood Safety Culture Module Brochurejamil voraОценок пока нет

- HR ProjectДокумент61 страницаHR ProjectNeema Pal100% (2)

- Final pROJECT INDIAN IT sECTOR 1Документ46 страницFinal pROJECT INDIAN IT sECTOR 1Ankit Fating73% (15)

- Recruitment and Selection Process of TCSДокумент34 страницыRecruitment and Selection Process of TCSkhushboolangalia100% (3)

- Recruitment and Selection in WiproДокумент41 страницаRecruitment and Selection in WiproShivraj Ghodeswar100% (3)

- Jio Recruitment and Selection ProjectДокумент101 страницаJio Recruitment and Selection ProjectShobhit Goswami50% (6)

- Reliance HR ProjectДокумент104 страницыReliance HR ProjectAnanyaa82% (33)

- Deloitte Cost OptimizationДокумент32 страницыDeloitte Cost OptimizationVik DixОценок пока нет

- GroupeAriel S.AДокумент3 страницыGroupeAriel S.AEina GuptaОценок пока нет

- Recruitment and Selection Process at Infosys and Learning MateДокумент78 страницRecruitment and Selection Process at Infosys and Learning Matechao sherpa80% (10)

- Project Report On HR Policies and Its Implementation at Deepak Nitrite LimitedДокумент64 страницыProject Report On HR Policies and Its Implementation at Deepak Nitrite LimitedRajkumar Das75% (4)

- TCS Organization StructureДокумент34 страницыTCS Organization Structureurmi_patel22Оценок пока нет

- Project Report BBA Human Resource Planning in Dainika BhaskarДокумент62 страницыProject Report BBA Human Resource Planning in Dainika BhaskarAditi Pareek90% (10)

- It Industry ProfileДокумент9 страницIt Industry ProfileJoshua Stalin Selvaraj67% (3)

- Itc Project ReportДокумент55 страницItc Project ReportSaloniGupta100% (1)

- A Study On Training and Development Process at HCL Technologies LTD Lucknow HRДокумент100 страницA Study On Training and Development Process at HCL Technologies LTD Lucknow HRChandan Srivastava100% (1)

- Project ReportДокумент75 страницProject Reportsrivastava_sonal06100% (6)

- Mba Project Titles On HRДокумент1 страницаMba Project Titles On HRkumar_208982% (11)

- Selection and Recruitment Process at InfosysДокумент12 страницSelection and Recruitment Process at Infosysshibhal83% (24)

- MTR Foods-A Marketing MarvelДокумент13 страницMTR Foods-A Marketing MarvelShabana IbrahimОценок пока нет

- MTR Foods-A Marketing MarvelДокумент13 страницMTR Foods-A Marketing MarvelShabana IbrahimОценок пока нет

- Tcs Company ProfileДокумент3 страницыTcs Company ProfileSridhar Vakkapati50% (2)

- Introduction To IT SectorДокумент2 страницыIntroduction To IT SectorNishant Gambhir75% (4)

- Airtel Final Project ReportДокумент69 страницAirtel Final Project ReportDrJyoti Agarwal100% (1)

- A Project Report On Recruitment and Selection Process1Документ108 страницA Project Report On Recruitment and Selection Process1piyush_dev100% (3)

- ISM-Practical File-BBA 212Документ20 страницISM-Practical File-BBA 212chandniОценок пока нет

- Report On IT IndustryДокумент43 страницыReport On IT IndustryAkshay GuptaОценок пока нет

- Final ProjectДокумент64 страницыFinal ProjectAneesh Chorode0% (2)

- Report On It Industry: Submitted By: Group 11 Ashwin Sarah Surendra Ankit PallaviДокумент49 страницReport On It Industry: Submitted By: Group 11 Ashwin Sarah Surendra Ankit PallaviSurendra Kumar KandruОценок пока нет

- Project Report of LG-MBA Project Report-Prince DudhatraДокумент93 страницыProject Report of LG-MBA Project Report-Prince DudhatrapRiNcE DuDhAtRa100% (1)

- A Project Report.Документ50 страницA Project Report.Ompriya Acharya100% (2)

- Executive SummaryДокумент10 страницExecutive SummarySujanShukla100% (1)

- MBA PROJECT Reliance Energe Employee EngagementДокумент85 страницMBA PROJECT Reliance Energe Employee EngagementAakash Pareek100% (2)

- Tata Group Project 1 1Документ53 страницыTata Group Project 1 1NAVEEN ROYОценок пока нет

- Airtel Internship ReportДокумент46 страницAirtel Internship ReportHarish Prajapat100% (3)

- Module 8 - Information TechnologyДокумент5 страницModule 8 - Information TechnologyNECIE JOY LUNARIOОценок пока нет

- CC 101 SG1Документ16 страницCC 101 SG1Aaron CarolinoОценок пока нет

- Module IT COM1 Unit 1Документ16 страницModule IT COM1 Unit 1Joshua DalmacioОценок пока нет

- Presentasi TD (Farid Mutohhari 20702251002)Документ17 страницPresentasi TD (Farid Mutohhari 20702251002)hamid nurОценок пока нет

- Fm-Aa-CIA-15 CC 101 Study Guide 1 FinalДокумент13 страницFm-Aa-CIA-15 CC 101 Study Guide 1 Finalkamina ayatoОценок пока нет

- Session-4-5: Manojit ChattopadhyayДокумент42 страницыSession-4-5: Manojit ChattopadhyayUtkarsh GurjarОценок пока нет

- TOPIC 1 STUDY Computer and IT IndustriesДокумент12 страницTOPIC 1 STUDY Computer and IT IndustriesLouie Christian FriasОценок пока нет

- IT Infrastructure, Evolution, Latest Trends and IT Strategy: Fundamental of ComputersДокумент15 страницIT Infrastructure, Evolution, Latest Trends and IT Strategy: Fundamental of ComputersInder_Joshi_8243100% (2)

- G11 Ict 2 Group 4Документ9 страницG11 Ict 2 Group 4ZennnОценок пока нет

- Presentation of MIET For Engineering and IT CollegesДокумент36 страницPresentation of MIET For Engineering and IT CollegesSandip JadavОценок пока нет

- Homework 3 - B18231077Документ3 страницыHomework 3 - B18231077Ishtiaq ShushaanОценок пока нет

- Project ReportДокумент19 страницProject ReportM.Jenifer ShylajaОценок пока нет

- Introduction InglesДокумент10 страницIntroduction InglesJose Guillermo Valeriano LeañoОценок пока нет

- Technical Management & IT Services - ProjectДокумент62 страницыTechnical Management & IT Services - ProjectPrashant KumarОценок пока нет

- HRM (ITTIAM SYSTEMS PVT) AssignmentДокумент15 страницHRM (ITTIAM SYSTEMS PVT) AssignmentnikkuОценок пока нет

- Included in Information TechnologyДокумент2 страницыIncluded in Information TechnologyCrishia PeraltaОценок пока нет

- Isabela State University: Republic of The Philippines Cauayan City, IsabelaДокумент20 страницIsabela State University: Republic of The Philippines Cauayan City, IsabelaKaren joy BajoОценок пока нет

- Components of The Management Information System: Week.5Документ21 страницаComponents of The Management Information System: Week.5Tuba MirzaОценок пока нет

- Lifebuoy in India (BM)Документ2 страницыLifebuoy in India (BM)Shabana IbrahimОценок пока нет

- Group Discussion TopicsДокумент7 страницGroup Discussion TopicsShabana IbrahimОценок пока нет

- Logistics NotesДокумент5 страницLogistics NotesShabana IbrahimОценок пока нет

- How Does Sales Change - BakeryDataДокумент49 страницHow Does Sales Change - BakeryDataShabana IbrahimОценок пока нет

- Investigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerДокумент3 страницыInvestigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerShabana IbrahimОценок пока нет

- Investigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerДокумент3 страницыInvestigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerShabana IbrahimОценок пока нет

- 12 Angry MenДокумент2 страницы12 Angry MenShabana IbrahimОценок пока нет

- 12 Angry MenДокумент2 страницы12 Angry MenShabana IbrahimОценок пока нет

- Investigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerДокумент3 страницыInvestigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerShabana IbrahimОценок пока нет

- 12 Angry MenДокумент2 страницы12 Angry MenShabana IbrahimОценок пока нет

- Investigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerДокумент3 страницыInvestigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerShabana IbrahimОценок пока нет

- Investigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerДокумент3 страницыInvestigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerShabana IbrahimОценок пока нет

- Investigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerДокумент3 страницыInvestigation Report For The Root Cause To Managing Director (Ravishing LTD) - by Personnel ManagerShabana IbrahimОценок пока нет

- 12 Angry MenДокумент2 страницы12 Angry MenShabana IbrahimОценок пока нет

- HCL DSB BMP WorkДокумент5 страницHCL DSB BMP WorkShabana IbrahimОценок пока нет

- Comptia It Industry Outlook 2020 PDFДокумент42 страницыComptia It Industry Outlook 2020 PDFjoseacvОценок пока нет

- HCL DSB BMP WorkДокумент5 страницHCL DSB BMP WorkShabana IbrahimОценок пока нет

- Company Management: Board of DirectorsДокумент5 страницCompany Management: Board of DirectorsShabana IbrahimОценок пока нет

- Chapter 7, Problem 3Документ52 страницыChapter 7, Problem 3MagdalenaОценок пока нет

- Kisi-Kisi Uts Enterprise System Tipe I - Kemungkinan Bisa KeluarДокумент16 страницKisi-Kisi Uts Enterprise System Tipe I - Kemungkinan Bisa KeluarwahyuОценок пока нет

- EY Global Fraud SurveyДокумент28 страницEY Global Fraud SurveyannnooonnyyyymmousssОценок пока нет

- Accounting Cycle StepsДокумент4 страницыAccounting Cycle StepsAntiiasmawatiiОценок пока нет

- Unit 5 - Partnership ActДокумент28 страницUnit 5 - Partnership ActNataraj PОценок пока нет

- How To Plan For Growth Peter BartaДокумент122 страницыHow To Plan For Growth Peter BartaOlga MolocencoОценок пока нет

- ICAB Knowledge Level Accounting May-Jun 2016Документ2 страницыICAB Knowledge Level Accounting May-Jun 2016Bizness Zenius HantОценок пока нет

- H. Aronson & Co., Inc. v. Associated Labor UnionДокумент4 страницыH. Aronson & Co., Inc. v. Associated Labor UnionChing ApostolОценок пока нет

- Audit Internship Report Nida DKДокумент28 страницAudit Internship Report Nida DKShan Ali ShahОценок пока нет

- Learning Objectives - VAT (FINAL)Документ2 страницыLearning Objectives - VAT (FINAL)Pranay GovenderОценок пока нет

- Comparrative Analysis of Npa of Private Sector and Public Sector BankДокумент79 страницComparrative Analysis of Npa of Private Sector and Public Sector Bankhoney sriОценок пока нет

- Balance Sheet For Mahindra & Mahindra Pvt. LTD.: Assets Amount (In Crores) Non-Current AssetsДокумент32 страницыBalance Sheet For Mahindra & Mahindra Pvt. LTD.: Assets Amount (In Crores) Non-Current AssetsAniketОценок пока нет

- AIS Chapter 1Документ8 страницAIS Chapter 1Laurie Mae ToledoОценок пока нет

- SAP - Customizing Guide: Printed by Ahmad RizkiДокумент11 страницSAP - Customizing Guide: Printed by Ahmad RizkiJosé FaiaОценок пока нет

- Outsourcing Security Case StudyДокумент13 страницOutsourcing Security Case StudyismakieОценок пока нет

- BMA4106 Investment and Asset Management Lecture 2Документ21 страницаBMA4106 Investment and Asset Management Lecture 2Dickson OgendiОценок пока нет

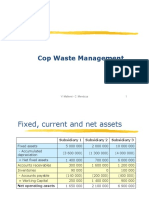

- Cop Waste Management SolutionДокумент5 страницCop Waste Management SolutionPaul GhanimehОценок пока нет

- Diamond Eagle Acquisition Corporation S-4Документ15 страницDiamond Eagle Acquisition Corporation S-4Carlos JesenaОценок пока нет

- Compiled By: Tanveer M Malik (17122) Atif Abbas Faizan Puri - 13368 MaheshДокумент38 страницCompiled By: Tanveer M Malik (17122) Atif Abbas Faizan Puri - 13368 MaheshM.TalhaОценок пока нет