Вам также может понравиться

- Key Responsibility Areas: Technical Officer - Core Banking and Application SupportДокумент3 страницыKey Responsibility Areas: Technical Officer - Core Banking and Application SupportWaiОценок пока нет

- Data Migration SheetДокумент58 страницData Migration SheetWai100% (1)

- Key Responsibility Areas: T24 Consultant - Core BankingДокумент3 страницыKey Responsibility Areas: T24 Consultant - Core BankingWaiОценок пока нет

- PD IT Support Team Leader coreBankingApplicationSupport PDFДокумент5 страницPD IT Support Team Leader coreBankingApplicationSupport PDFWaiОценок пока нет

- Job Description - Application LeadДокумент11 страницJob Description - Application LeadWaiОценок пока нет

- Cardnumber Datetime Terminalpid Transactiontype Amount Currency ResponsecodeДокумент20 страницCardnumber Datetime Terminalpid Transactiontype Amount Currency ResponsecodeWaiОценок пока нет

- Case Study: Metro BankДокумент28 страницCase Study: Metro BankWaiОценок пока нет

- Book 2Документ18 страницBook 2WaiОценок пока нет

- Standards MT Release 2018 Impact On Messaging Interfaces: Mandatory Presence of Field 121 Unique End-To-End Transaction Reference (UETR)Документ6 страницStandards MT Release 2018 Impact On Messaging Interfaces: Mandatory Presence of Field 121 Unique End-To-End Transaction Reference (UETR)WaiОценок пока нет

- Swift Standards sr2018 MT Updated High Level InformationДокумент38 страницSwift Standards sr2018 MT Updated High Level InformationWai100% (1)

- B ANKINGДокумент10 страницB ANKINGWaiОценок пока нет

- Smartvista CBS SpecificationДокумент62 страницыSmartvista CBS SpecificationWai100% (1)

- Colostomy BagДокумент1 страницаColostomy BagWaiОценок пока нет

- ResumeДокумент1 страницаResumeWaiОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Correct Mark 1.00 Out of 1.00: DirectДокумент13 страницCorrect Mark 1.00 Out of 1.00: DirectRuth Abrogar71% (7)

- Work Experience: Area Sales ManagerДокумент4 страницыWork Experience: Area Sales ManagerHamid SaifОценок пока нет

- Gmat 700 - 800 Level QuestionsДокумент6 страницGmat 700 - 800 Level Questionsfrancescoabc0% (1)

- MH5 PDFДокумент55 страницMH5 PDFHammadОценок пока нет

- Accounts Receivable Notes Receivable RevenueДокумент11 страницAccounts Receivable Notes Receivable RevenueVatchdemonОценок пока нет

- Chap 014 PДокумент18 страницChap 014 PMartin TisherОценок пока нет

- MRII Lean 6 Sigma WorkshopДокумент191 страницаMRII Lean 6 Sigma WorkshopDonna CincoОценок пока нет

- Amazon - Power 5 - Strategic Plan ReportДокумент35 страницAmazon - Power 5 - Strategic Plan ReportELECTRIC EGYPTОценок пока нет

- Fundamentals of Cost Analysis For Decision Making: True / False QuestionsДокумент231 страницаFundamentals of Cost Analysis For Decision Making: True / False QuestionsElaine Gimarino0% (1)

- Business Model CanvasДокумент2 страницыBusiness Model CanvasNurul DiyanaОценок пока нет

- MaricoДокумент39 страницMaricoanon_6506039460% (5)

- The Five Competitive Forces That Shape StrategyДокумент5 страницThe Five Competitive Forces That Shape StrategyAmol Deherkar67% (3)

- Problematique MapДокумент3 страницыProblematique MapMel TuazonОценок пока нет

- P5 PDFДокумент82 страницыP5 PDFLukasz HorzelaОценок пока нет

- Mohsin Hassan Bba Iib BUS-19F-044 Principle of AccountingДокумент7 страницMohsin Hassan Bba Iib BUS-19F-044 Principle of AccountingMohsin HassanОценок пока нет

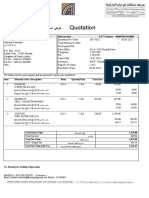

- Quotation: Customer Code: 10002349 Information VAT Number - 300055945410003Документ2 страницыQuotation: Customer Code: 10002349 Information VAT Number - 300055945410003Marcial MilitanteОценок пока нет

- Sales Career in ITC - STR 2022-MumbaiДокумент2 страницыSales Career in ITC - STR 2022-MumbaiKuhu MiglaniОценок пока нет

- ACC 422case ExamДокумент11 страницACC 422case ExamYutaka KomatsuzakiОценок пока нет

- Bcom Sem Vi - Principles of Business DecisionsДокумент24 страницыBcom Sem Vi - Principles of Business DecisionsNaveen Kalakat0% (1)

- Laws, Ethics, and Social Responsibility in Pricing: College of Management and Business TechnologyДокумент21 страницаLaws, Ethics, and Social Responsibility in Pricing: College of Management and Business TechnologyFergus ParungaoОценок пока нет

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Документ1 страницаTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)UP Vlogger Sheetal SharmaОценок пока нет

- 67767bos54359 cp8 PDFДокумент193 страницы67767bos54359 cp8 PDFvenuОценок пока нет

- Corporate Level Strategies: DR - Hameed AkhtarДокумент30 страницCorporate Level Strategies: DR - Hameed AkhtarNazir AnsariОценок пока нет

- Lesson 1 - STSДокумент8 страницLesson 1 - STSThanh ThuýОценок пока нет

- TEST1 ACC 106 Nov 2017 Solution Part AДокумент4 страницыTEST1 ACC 106 Nov 2017 Solution Part AZulaikha JasniОценок пока нет

- CH 5 Quiz 1Документ2 страницыCH 5 Quiz 1Jessa BasadreОценок пока нет

- Topic 7 - Receivables - Rev (Students)Документ48 страницTopic 7 - Receivables - Rev (Students)RomziОценок пока нет

- Appraisal Form - AmmaДокумент3 страницыAppraisal Form - AmmaMilestone Institute of TechnologyОценок пока нет

- Real Estate Purchase Offer Form PDFДокумент1 страницаReal Estate Purchase Offer Form PDFEd williamsonОценок пока нет

- Summer Training Project ReportДокумент53 страницыSummer Training Project Reportbhavya tayalОценок пока нет