Вам также может понравиться

- Maria Abriel C. Buena Advance II: About IQ OptionДокумент4 страницыMaria Abriel C. Buena Advance II: About IQ Optionlady chase50% (2)

- Bank Is An Agent, Trustee, Executor, Administrator For CustomersДокумент5 страницBank Is An Agent, Trustee, Executor, Administrator For Customersgazi faisalОценок пока нет

- Financial Analysis P&GДокумент10 страницFinancial Analysis P&Gsayko88Оценок пока нет

- Analysis of The ManzanaДокумент24 страницыAnalysis of The ManzanaAnalogic Rome100% (1)

- Butler Lumber Case DiscussionДокумент3 страницыButler Lumber Case DiscussionJayzie Li100% (1)

- Company Valuation and Financial Analysis of Power Root (M) Sdn BhdДокумент35 страницCompany Valuation and Financial Analysis of Power Root (M) Sdn BhdKar EngОценок пока нет

- Assignment Next PLCДокумент16 страницAssignment Next PLCJames Jane50% (2)

- Star River - Sample ReportДокумент15 страницStar River - Sample ReportMD LeeОценок пока нет

- Case Analysis NATOДокумент5 страницCase Analysis NATOTalha SiddiquiОценок пока нет

- Butler Lumber Final First DraftДокумент12 страницButler Lumber Final First DraftAdit Swarup100% (2)

- Financial Analysis of Martin Manufacturing Company Highlights Key Liquidity, Activity and Profitability RatiosДокумент15 страницFinancial Analysis of Martin Manufacturing Company Highlights Key Liquidity, Activity and Profitability RatiosdjmondieОценок пока нет

- Estimating Funds Requirements Butler Lumber CompanyДокумент18 страницEstimating Funds Requirements Butler Lumber CompanyNabab Shirajuddoula71% (7)

- Costco Wholesale Corporation Financial AnalysisДокумент14 страницCostco Wholesale Corporation Financial Analysisdejong100% (1)

- INVESTMENT AVENUES BLACK BOOK UpgradedДокумент71 страницаINVESTMENT AVENUES BLACK BOOK UpgradedJack DawsonОценок пока нет

- Star River Assignment-ReportДокумент15 страницStar River Assignment-ReportBlessing Simons33% (3)

- Problem 9-1, 2 & 3Документ3 страницыProblem 9-1, 2 & 3Micah April SabularseОценок пока нет

- Final Project - FA Assignment Financial Analysis of VoltasДокумент26 страницFinal Project - FA Assignment Financial Analysis of VoltasHarvey100% (2)

- Nism 5 A - Mutual Fund Exam - Practice Test 1Документ24 страницыNism 5 A - Mutual Fund Exam - Practice Test 1Aditi Sawant100% (5)

- Butler Lumber Company: Following Questions Are Answered in This Case Study SolutionДокумент3 страницыButler Lumber Company: Following Questions Are Answered in This Case Study SolutionTalha SiddiquiОценок пока нет

- Audit Program Liabilities Against AssetsДокумент11 страницAudit Program Liabilities Against AssetsRoemi Rivera Robedizo100% (3)

- Analysis of Annual Report - UnileverДокумент7 страницAnalysis of Annual Report - UnileverUmair KhizarОценок пока нет

- Auditors Report and Financial Analysis of ITCДокумент28 страницAuditors Report and Financial Analysis of ITCNeeraj BhartiОценок пока нет

- Financial Analysis of Reliance Steel and Aluminium Co. LTDДокумент4 страницыFinancial Analysis of Reliance Steel and Aluminium Co. LTDROHIT SETHIОценок пока нет

- Credit Policy For Tam EnterprisesДокумент3 страницыCredit Policy For Tam Enterprises04Ronita MitraОценок пока нет

- NPV, IRR and Financial Evaluation for Waste Collection ContractДокумент9 страницNPV, IRR and Financial Evaluation for Waste Collection ContractTwafik MoОценок пока нет

- Cases in Finance - FIN 200Документ3 страницыCases in Finance - FIN 200avegaОценок пока нет

- Ratio Analysis of Renata Limited PPPДокумент32 страницыRatio Analysis of Renata Limited PPPmdnabab0% (1)

- Term Paper of Reliance Weaving LTDДокумент12 страницTerm Paper of Reliance Weaving LTDadeelasghar091Оценок пока нет

- International Standard On Auditing: Option .1 Cross Sectional Analysis - Liquidity Ratios:-Current RatioДокумент3 страницыInternational Standard On Auditing: Option .1 Cross Sectional Analysis - Liquidity Ratios:-Current RatioikramunirОценок пока нет

- FRA - IV (Tarsons Products)Документ9 страницFRA - IV (Tarsons Products)RR AnalystОценок пока нет

- Ratios NoteДокумент24 страницыRatios Noteamit singhОценок пока нет

- 277 Financial Statement As Management ToolДокумент8 страниц277 Financial Statement As Management ToolkandriantoОценок пока нет

- Finance Henry BootДокумент19 страницFinance Henry BootHassanОценок пока нет

- Ratio AnalysisДокумент13 страницRatio AnalysisBharatsinh SarvaiyaОценок пока нет

- Ratio AnaalysisДокумент10 страницRatio AnaalysisMark K. EapenОценок пока нет

- Engro Foods Engro Foods Engro FoodsДокумент37 страницEngro Foods Engro Foods Engro FoodsAli haiderОценок пока нет

- Final Report On Attock - IbfДокумент25 страницFinal Report On Attock - IbfSanam Aamir0% (1)

- Financial ManagementДокумент6 страницFinancial ManagementNavinYattiОценок пока нет

- Chapter 26 - Analysis of Accounts (EDITED)Документ17 страницChapter 26 - Analysis of Accounts (EDITED)Amour PartekaОценок пока нет

- Analysis of Financial Statement: AFS ProjectДокумент11 страницAnalysis of Financial Statement: AFS ProjectErum AnwerОценок пока нет

- Financial Management (1) (8818)Документ22 страницыFinancial Management (1) (8818)georgeОценок пока нет

- Finance Coursework FinalДокумент7 страницFinance Coursework FinalmattОценок пока нет

- Below Are Balance Sheet, Income Statement, Statement of Cash Flows, and Selected Notes To The Financial StatementsДокумент14 страницBelow Are Balance Sheet, Income Statement, Statement of Cash Flows, and Selected Notes To The Financial StatementsQueen ValleОценок пока нет

- IOCL AnalysisДокумент3 страницыIOCL Analysisprit6924Оценок пока нет

- WCM AnalysisДокумент7 страницWCM AnalysisUtsab SenОценок пока нет

- Financial Statement Analysis ReportДокумент30 страницFinancial Statement Analysis ReportMariyam LiaqatОценок пока нет

- Eng Kah Corporation BerhadДокумент5 страницEng Kah Corporation BerhadNoel KlОценок пока нет

- Financial Statement Analysis: Text Book-Chapter 12Документ13 страницFinancial Statement Analysis: Text Book-Chapter 12anwesh pradhanОценок пока нет

- MANAGERIAL ACCOUNTING INSTRUCTIONAL MATERIAL Chapter 4Документ11 страницMANAGERIAL ACCOUNTING INSTRUCTIONAL MATERIAL Chapter 4gleem.laurelОценок пока нет

- DATE: 12 June 2011: Financial Performance Report For MPLCДокумент20 страницDATE: 12 June 2011: Financial Performance Report For MPLCVinay RamamurthyОценок пока нет

- Profitability AnalysisДокумент9 страницProfitability AnalysisAnkit TyagiОценок пока нет

- Financial Management and Control - AssignmentДокумент7 страницFinancial Management and Control - AssignmentSabahat BashirОценок пока нет

- "Financial Analysis of Kilburn Chemicals": Case Study OnДокумент20 страниц"Financial Analysis of Kilburn Chemicals": Case Study Onshraddha mehtaОценок пока нет

- Documents Tips Pgbm01-Finance-Management PDFДокумент25 страницDocuments Tips Pgbm01-Finance-Management PDFJonathan LimОценок пока нет

- Cognizant Accounts. FinalДокумент9 страницCognizant Accounts. FinalkrunalОценок пока нет

- PIDILITE INDUSTRIES FINANCIAL ANALYSISДокумент2 страницыPIDILITE INDUSTRIES FINANCIAL ANALYSISronaldweasley6Оценок пока нет

- Financial Analysis Report Shell Cluster 7531Документ4 страницыFinancial Analysis Report Shell Cluster 7531Darren MavadyОценок пока нет

- Analysis of Financial Statements: QuestionsДокумент44 страницыAnalysis of Financial Statements: QuestionsgeubrinariaОценок пока нет

- A Project Report On Ratio Analysis at BemulДокумент94 страницыA Project Report On Ratio Analysis at BemulBabasab Patil (Karrisatte)Оценок пока нет

- FRA Report: GMR Infrastructure: Submitted To: Submitted byДокумент12 страницFRA Report: GMR Infrastructure: Submitted To: Submitted bySunil KumarОценок пока нет

- Financial Statement Analysis With Ratio Analysis On: Glenmark Pharmaceutical LimitedДокумент41 страницаFinancial Statement Analysis With Ratio Analysis On: Glenmark Pharmaceutical LimitedGovindraj PrabhuОценок пока нет

- Vladi FAF Financial ReportДокумент4 страницыVladi FAF Financial ReportVladi DimitrovОценок пока нет

- Profit standards for residential contractorsДокумент4 страницыProfit standards for residential contractorsKhai08 DenОценок пока нет

- Tunku Puteri Intan Safinaz School of Accountancy Bkal3063 Integrated Case Study FIRST SEMESTER 2020/2021 (A201)Документ14 страницTunku Puteri Intan Safinaz School of Accountancy Bkal3063 Integrated Case Study FIRST SEMESTER 2020/2021 (A201)Aisyah ArifinОценок пока нет

- Profitability Turnover RatiosДокумент32 страницыProfitability Turnover RatiosAnushka JindalОценок пока нет

- Strategic Financial Management: Presented By:-Rupesh Kadam (PG-11-084)Документ40 страницStrategic Financial Management: Presented By:-Rupesh Kadam (PG-11-084)Rupesh KadamОценок пока нет

- ROIC ChangedДокумент2 страницыROIC ChangedTalha SiddiquiОценок пока нет

- Can Lenovo Regain Past GloryДокумент22 страницыCan Lenovo Regain Past GloryTalha SiddiquiОценок пока нет

- Dyna Tronic SДокумент1 страницаDyna Tronic SPolina TsviyovichОценок пока нет

- Eureka Fair InstructionsДокумент2 страницыEureka Fair InstructionsTalha SiddiquiОценок пока нет

- AT&T vs Verizon Case StudyДокумент9 страницAT&T vs Verizon Case Studyroyal lathОценок пока нет

- TOI-SU20-SAT-EPEP - Prototype Video & Website LinksДокумент1 страницаTOI-SU20-SAT-EPEP - Prototype Video & Website LinksTalha SiddiquiОценок пока нет

- Toi Su20 Sat EpepДокумент5 страницToi Su20 Sat EpepTalha SiddiquiОценок пока нет

- Toi Su20 Sat Epep Term ReportДокумент17 страницToi Su20 Sat Epep Term ReportTalha SiddiquiОценок пока нет

- Dyna Tronic SДокумент1 страницаDyna Tronic SPolina TsviyovichОценок пока нет

- Toi Su20 Sat EpepДокумент5 страницToi Su20 Sat EpepTalha SiddiquiОценок пока нет

- Toi Su20 Sat Epep Term ReportДокумент17 страницToi Su20 Sat Epep Term ReportTalha SiddiquiОценок пока нет

- Toi Su20 Sat Epep Term ReportДокумент17 страницToi Su20 Sat Epep Term ReportTalha SiddiquiОценок пока нет

- Toi Su20 Sat EpepДокумент5 страницToi Su20 Sat EpepTalha SiddiquiОценок пока нет

- Toi Su20 Sat Epep ProposalДокумент7 страницToi Su20 Sat Epep ProposalTalha SiddiquiОценок пока нет

- Aasan Solutions - Home Based Services AppДокумент11 страницAasan Solutions - Home Based Services AppTalha SiddiquiОценок пока нет

- TOI-SU20-SAT-EPEP - Prototype Video & Website LinksДокумент1 страницаTOI-SU20-SAT-EPEP - Prototype Video & Website LinksTalha SiddiquiОценок пока нет

- Competitive Advantage - Revisited Michael PorterДокумент20 страницCompetitive Advantage - Revisited Michael PorterVidya NatawidhaОценок пока нет

- Porter DiamondДокумент8 страницPorter DiamondBayu PrabowoОценок пока нет

- Blueoceanstrategy 100403005918 Phpapp02Документ78 страницBlueoceanstrategy 100403005918 Phpapp02Md Najmus SaquibОценок пока нет

- Butler Lumber Case SolutionДокумент4 страницыButler Lumber Case SolutionMohammad Owais ShaikhОценок пока нет

- Competitive StrategyДокумент9 страницCompetitive StrategyTalha SiddiquiОценок пока нет

- Description: Other Data: Cash Dividend Declared & Paid Rs 20,000Документ6 страницDescription: Other Data: Cash Dividend Declared & Paid Rs 20,000Talha SiddiquiОценок пока нет

- SFAD Week 1Документ4 страницыSFAD Week 1Talha SiddiquiОценок пока нет

- SFAD Week 2Документ10 страницSFAD Week 2Talha SiddiquiОценок пока нет

- Butler Lumber Company Case Solution CasesolДокумент3 страницыButler Lumber Company Case Solution CasesolTalha SiddiquiОценок пока нет

- Malelang, Roseanne Pearl, B. BSA 2-4Документ9 страницMalelang, Roseanne Pearl, B. BSA 2-4RoseanneОценок пока нет

- Bank Reconmciliation ProcessДокумент13 страницBank Reconmciliation ProcessRachelleОценок пока нет

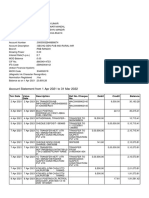

- Account Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент14 страницAccount Statement From 1 Apr 2021 To 31 Mar 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceRishav AnandОценок пока нет

- Haskayne Resume Template 1Документ1 страницаHaskayne Resume Template 1Mako SmithОценок пока нет

- E00B0 Credit Risk Management - Axis BankДокумент55 страницE00B0 Credit Risk Management - Axis BankwebstdsnrОценок пока нет

- RockAuto order confirmation for Paul JenkinsДокумент2 страницыRockAuto order confirmation for Paul JenkinsPaul JenkinsОценок пока нет

- Acctg 101 Module 1Документ22 страницыAcctg 101 Module 1Heart SebОценок пока нет

- Studio Renovations: Barbados Community College Division of Fine Arts - Music MathsДокумент10 страницStudio Renovations: Barbados Community College Division of Fine Arts - Music MathsShanice JohnОценок пока нет

- Lembar Kerja UD. Mudah HasilДокумент41 страницаLembar Kerja UD. Mudah HasilRoni NОценок пока нет

- Advacc 1 Answer Key Set AДокумент3 страницыAdvacc 1 Answer Key Set AA BОценок пока нет

- Sample SALN Form Excel FormatДокумент2 страницыSample SALN Form Excel FormatExtreme Fact TVОценок пока нет

- Valuation of SecuritiesДокумент7 страницValuation of SecuritiesEmmanuelОценок пока нет

- Transaction History Reportwellnxtcorporwellnxt Corporation14062019210657Документ2 страницыTransaction History Reportwellnxtcorporwellnxt Corporation14062019210657roda mansuetoОценок пока нет

- NFL Annual Report 2019 Compressed PDFДокумент130 страницNFL Annual Report 2019 Compressed PDFZUBAIRОценок пока нет

- 6409-Article Text-22422-1-10-20120709 PDFДокумент10 страниц6409-Article Text-22422-1-10-20120709 PDFAmosh ShresthaОценок пока нет

- Role of Banking Sector in Indian EconomyДокумент6 страницRole of Banking Sector in Indian EconomySandeep TiwariОценок пока нет

- Act 171 5.1-1 Midterm Exam 2021 NoneДокумент3 страницыAct 171 5.1-1 Midterm Exam 2021 NoneAngeliePanerioGonzagaОценок пока нет

- Transaction: Marathon Futurex, A & B Wing, 12th Floor, N. M. Joshi Marg, Lower Parel, Mumbai - 400013 1800-22-3345Документ21 страницаTransaction: Marathon Futurex, A & B Wing, 12th Floor, N. M. Joshi Marg, Lower Parel, Mumbai - 400013 1800-22-3345Nishant MeghwalОценок пока нет

- Receipt: Received From (Client Name) AmountДокумент1 страницаReceipt: Received From (Client Name) AmountHexel PratamaОценок пока нет

- Form2a Utkarshbnk NRДокумент8 страницForm2a Utkarshbnk NRzalak jintanwalaОценок пока нет

- Chawla Parties Upto 14 Jan-19Документ104 страницыChawla Parties Upto 14 Jan-19mudassar nazarОценок пока нет

- Accounting Cycle Journal Entries With Chart of AccountsДокумент4 страницыAccounting Cycle Journal Entries With Chart of Accountskutsara0300Оценок пока нет

- 8 - Cash Budget FormatДокумент4 страницы8 - Cash Budget Formatnur alia raihanaОценок пока нет

- HDB Enterprise Business Loans - HDBДокумент4 страницыHDB Enterprise Business Loans - HDBhermandeep5Оценок пока нет