Вам также может понравиться

- Chapter06 - Answer PDFДокумент6 страницChapter06 - Answer PDFJONAS VINCENT SamsonОценок пока нет

- Ix - Completing The Audit and Audit of Financial Statements Presentation PROBLEM NO. 1 - Statement of Financial PositionДокумент12 страницIx - Completing The Audit and Audit of Financial Statements Presentation PROBLEM NO. 1 - Statement of Financial PositionKirstine DelegenciaОценок пока нет

- Joint Arrangement Quizzer 2 AnswerДокумент12 страницJoint Arrangement Quizzer 2 AnswerAndrea ReyesОценок пока нет

- Acctg 10 - Final ExamДокумент6 страницAcctg 10 - Final ExamNANОценок пока нет

- 55026RR 14-2010 Accreditation PDFДокумент5 страниц55026RR 14-2010 Accreditation PDFlmin34Оценок пока нет

- Petty Cash Fund SetupДокумент5 страницPetty Cash Fund SetupJay Lou PayotОценок пока нет

- Prelim CashДокумент10 страницPrelim CashMary Lynn Sta PriscaОценок пока нет

- Reviewer 1st PB P1 1920Документ7 страницReviewer 1st PB P1 1920Therese AcostaОценок пока нет

- Financial Accounting by ValixДокумент5 страницFinancial Accounting by Valixblahblahblue0% (1)

- Financial Assets Guide - Cash, Receivables, Investments & DerivativesДокумент5 страницFinancial Assets Guide - Cash, Receivables, Investments & DerivativesYami HeatherОценок пока нет

- Lecture Note - Receivables Sy 2014-2015Документ10 страницLecture Note - Receivables Sy 2014-2015LeneОценок пока нет

- Far - Pre BoardДокумент17 страницFar - Pre BoardClene DoconteОценок пока нет

- Understanding The SelfДокумент9 страницUnderstanding The SelfNatalie SerranoОценок пока нет

- ACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREДокумент12 страницACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREKabalaОценок пока нет

- This Study Resource Was: (Stale Check)Документ2 страницыThis Study Resource Was: (Stale Check)Lyca Mae CubangbangОценок пока нет

- Cash and Cash Equivalents Multiple Choice QuestionsДокумент11 страницCash and Cash Equivalents Multiple Choice Questionsjhela18Оценок пока нет

- Statement of Comprehensive Income: Irene Mae C. Guerra, CPA, CTTДокумент21 страницаStatement of Comprehensive Income: Irene Mae C. Guerra, CPA, CTTRuaya AilynОценок пока нет

- Optical Clinic Financial RecordsДокумент3 страницыOptical Clinic Financial RecordsJadon MejiaОценок пока нет

- Audit of Receivables AdjustmentsДокумент5 страницAudit of Receivables AdjustmentsandreamrieОценок пока нет

- Diagnostic Test CashДокумент2 страницыDiagnostic Test CashJoannah maeОценок пока нет

- 07 - Revenue - Consignment Sales PDFДокумент17 страниц07 - Revenue - Consignment Sales PDFCarla MarieОценок пока нет

- Questionnaire Expenditure CycleДокумент1 страницаQuestionnaire Expenditure Cycleleodenin tulangОценок пока нет

- Psa 600Документ9 страницPsa 600Bhebi Dela CruzОценок пока нет

- RFBT Quiz 1 B45 PDFДокумент5 страницRFBT Quiz 1 B45 PDFrose annОценок пока нет

- Partnership Accounting ModuleДокумент15 страницPartnership Accounting ModuleMon RamОценок пока нет

- Audit of Educational InstitutionsДокумент3 страницыAudit of Educational InstitutionsjajoriaОценок пока нет

- Accounting for Business CombinationsДокумент13 страницAccounting for Business Combinationsmax pОценок пока нет

- MS Corporation financial data analysis 2018-2019Документ2 страницыMS Corporation financial data analysis 2018-2019Princess Edelyn CastorОценок пока нет

- Accounting 4 Note Payable and Debt RestructureДокумент2 страницыAccounting 4 Note Payable and Debt RestructurelorenОценок пока нет

- Cash and Cash EquivalentДокумент5 страницCash and Cash EquivalentPau SantosОценок пока нет

- Jpia LetterДокумент1 страницаJpia LetterAphze Bautista VlogОценок пока нет

- Trial Balance of Entity A GovernmentДокумент3 страницыTrial Balance of Entity A GovernmentPrincess NozalОценок пока нет

- Temporary Differences and Deferred Tax Assets & Liabilities ExplainedДокумент6 страницTemporary Differences and Deferred Tax Assets & Liabilities ExplainedLeng ChhunОценок пока нет

- DLSU CPA Cash and Cash EquivalentsДокумент3 страницыDLSU CPA Cash and Cash EquivalentsEuniceChungОценок пока нет

- Operational Auditing Group RecommendationsДокумент4 страницыOperational Auditing Group RecommendationscristinatubleОценок пока нет

- Petty Cash, Part 3 - Kuya Joseph's BlogДокумент5 страницPetty Cash, Part 3 - Kuya Joseph's BlogCM LanceОценок пока нет

- IAS 34 Interim Financial Reporting StandardsДокумент12 страницIAS 34 Interim Financial Reporting StandardsJenne LeeОценок пока нет

- Retained Earnings - ModuleДокумент12 страницRetained Earnings - ModuleFiverr RallОценок пока нет

- Audit of Cash and Cash EquivalentsДокумент2 страницыAudit of Cash and Cash EquivalentsWawex Davis100% (1)

- Home Office & Branch Accounting Problems SolvedДокумент3 страницыHome Office & Branch Accounting Problems SolvedChristianAquinoОценок пока нет

- Ae 231 2Документ4 страницыAe 231 2Mae-shane SagayoОценок пока нет

- Applied Auditing Report (Audit of Receivables)Документ7 страницApplied Auditing Report (Audit of Receivables)mary louise magana100% (1)

- Sales Made Evenly (Warranty Liability)Документ4 страницыSales Made Evenly (Warranty Liability)Jorufel Tomo PapasinОценок пока нет

- Gov AccДокумент13 страницGov AccZarah H. LeongОценок пока нет

- Calculate gross estate for cases of resident and non-resident decedentsДокумент6 страницCalculate gross estate for cases of resident and non-resident decedentsPaulo VillarinОценок пока нет

- CHAPTER 8 Intermediate Acctng 1Документ58 страницCHAPTER 8 Intermediate Acctng 1Tessang OnongenОценок пока нет

- Buscom ReviewerДокумент16 страницBuscom ReviewereysiОценок пока нет

- CH 6 Audit of Conversion CycleДокумент24 страницыCH 6 Audit of Conversion CyclerogealynОценок пока нет

- #10 Cash and Cash EquivalentsДокумент2 страницы#10 Cash and Cash Equivalentsmilan100% (3)

- Auditing 1 Final ExamДокумент8 страницAuditing 1 Final ExamEdemson NavalesОценок пока нет

- BS ACCOUNTANCY TRUE OR FALSE STATEMENTSДокумент1 страницаBS ACCOUNTANCY TRUE OR FALSE STATEMENTSSheena ClataОценок пока нет

- Cash With Cash EqualantДокумент5 страницCash With Cash EqualantkaviyapriyaОценок пока нет

- Planning an Audit of Financial StatementsДокумент10 страницPlanning an Audit of Financial StatementsTrixie Pearl TompongОценок пока нет

- Auditing Problems Test Banks - PPE Part 2Документ5 страницAuditing Problems Test Banks - PPE Part 2Alliah Mae ArbastoОценок пока нет

- Finals Government Accounting: Petty Cash FundДокумент4 страницыFinals Government Accounting: Petty Cash FundRafael Capunpon VallejosОценок пока нет

- Cherry Company accounts receivable adjustmentsДокумент6 страницCherry Company accounts receivable adjustmentsEdemson NavalesОценок пока нет

- Partnership Dissolution: QuizДокумент5 страницPartnership Dissolution: QuizLee SuarezОценок пока нет

- Assignment Notes PayableДокумент3 страницыAssignment Notes PayableLourdios EdullantesОценок пока нет

- Chapter 13 OutlineДокумент6 страницChapter 13 OutlineShella FrankeraОценок пока нет

- W6 Module 10 Cash and Cash Equivalents Part 2Документ8 страницW6 Module 10 Cash and Cash Equivalents Part 2leare ruazaОценок пока нет

- Break-Even Analysis Group ActivityДокумент2 страницыBreak-Even Analysis Group ActivityJimbo ManalastasОценок пока нет

- Countries Are Ranked On Everything From Health To HappinessДокумент8 страницCountries Are Ranked On Everything From Health To HappinessJimbo ManalastasОценок пока нет

- UST WC Finance With AnswersДокумент11 страницUST WC Finance With AnswersPauline Kisha Castro100% (1)

- DiversityДокумент1 страницаDiversityJimbo ManalastasОценок пока нет

- Worksheet # 3Документ3 страницыWorksheet # 3Ezer Cruz BarrantesОценок пока нет

- Case 3 Finals - 3Документ1 страницаCase 3 Finals - 3Jimbo ManalastasОценок пока нет

- Customer Day Browser Time (Min) Pages Viewed Amount Spent ($)Документ32 страницыCustomer Day Browser Time (Min) Pages Viewed Amount Spent ($)Jimbo ManalastasОценок пока нет

- FEU feasibility study on Bola Setenta chicken wings storeДокумент189 страницFEU feasibility study on Bola Setenta chicken wings storeJimbo ManalastasОценок пока нет

- Presentation Rubric (Position Paper) : Category Scoring Criteria Total PointsДокумент2 страницыPresentation Rubric (Position Paper) : Category Scoring Criteria Total PointsJimbo ManalastasОценок пока нет

- AI Ethics Values at SalesforceДокумент2 страницыAI Ethics Values at SalesforceJimbo ManalastasОценок пока нет

- Performance Output: School's Environmental Action PlanДокумент7 страницPerformance Output: School's Environmental Action PlanJimbo ManalastasОценок пока нет

- STUDENTS' FEEDBACK ABOUT THE LEARNING OUTCOMES - Canvas-1Документ2 страницыSTUDENTS' FEEDBACK ABOUT THE LEARNING OUTCOMES - Canvas-1Jimbo ManalastasОценок пока нет

- University State Graduation Rate % of Classes Under 20 Student-Faculty RatioДокумент31 страницаUniversity State Graduation Rate % of Classes Under 20 Student-Faculty RatioJimbo ManalastasОценок пока нет

- Dynamighty ContentДокумент5 страницDynamighty ContentJimbo ManalastasОценок пока нет

- Document 1etoДокумент2 страницыDocument 1etoJimbo ManalastasОценок пока нет

- Work Force: Name Task Job DescriptionДокумент1 страницаWork Force: Name Task Job DescriptionJimbo ManalastasОценок пока нет

- Work Force: Name Task Job DescriptionДокумент1 страницаWork Force: Name Task Job DescriptionJimbo ManalastasОценок пока нет

- Document 1etoДокумент2 страницыDocument 1etoJimbo ManalastasОценок пока нет

- Intermolecular Forces SimulationДокумент5 страницIntermolecular Forces SimulationJimbo ManalastasОценок пока нет

- Dynamighty ContentДокумент5 страницDynamighty ContentJimbo ManalastasОценок пока нет

- Financial Accounting and Reporting II Final Quiz QuestionsДокумент7 страницFinancial Accounting and Reporting II Final Quiz QuestionsjemsОценок пока нет

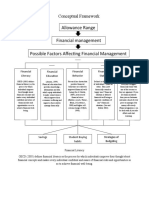

- Allowance Range: Conceptual FrameworkДокумент2 страницыAllowance Range: Conceptual FrameworkJimbo ManalastasОценок пока нет

- Tax Supplemental Reviewer - October 2019Документ46 страницTax Supplemental Reviewer - October 2019Daniel Anthony CabreraОценок пока нет

- Business Proposal: Product: DynamiteДокумент10 страницBusiness Proposal: Product: DynamiteJimbo ManalastasОценок пока нет

- Quiz - QUIZ 1Документ17 страницQuiz - QUIZ 1Jimbo ManalastasОценок пока нет

- Just-In-Time and Back Flush Costing: Cost Accounting and Control With SAPДокумент11 страницJust-In-Time and Back Flush Costing: Cost Accounting and Control With SAPJimbo ManalastasОценок пока нет

- IAS 20 Summary: Accounting for Government GrantsДокумент2 страницыIAS 20 Summary: Accounting for Government Grantsenzo100% (1)

- Practice Exercises: Graphical Method of Linear Programming Graph The Following Equations Then Find The FollowingДокумент4 страницыPractice Exercises: Graphical Method of Linear Programming Graph The Following Equations Then Find The FollowingJimbo ManalastasОценок пока нет

- Reviewer Links Sa Business TaxДокумент1 страницаReviewer Links Sa Business TaxJimbo ManalastasОценок пока нет

- Allocation of Service CostДокумент8 страницAllocation of Service CostJimbo ManalastasОценок пока нет

- Hindusthan Microfinance provides loans to Mumbai's poorДокумент25 страницHindusthan Microfinance provides loans to Mumbai's poorsunnyОценок пока нет

- Vajiram & Ravi Civil Services Exam Details for Sept 2022-23Документ3 страницыVajiram & Ravi Civil Services Exam Details for Sept 2022-23Appu MansaОценок пока нет

- Toa Consolidated Sample QuestionsДокумент60 страницToa Consolidated Sample QuestionsBabi Dimaano NavarezОценок пока нет

- LTD Report Innocent Purchaser For ValueДокумент3 страницыLTD Report Innocent Purchaser For ValuebcarОценок пока нет

- CDP Revised Toolkit Jun 09Документ100 страницCDP Revised Toolkit Jun 09kittu1216Оценок пока нет

- Securitization of Financial AssetsДокумент7 страницSecuritization of Financial Assetsnaglaa alyОценок пока нет

- Project Report On "Role of Banks in International Trade": Page - 1Документ50 страницProject Report On "Role of Banks in International Trade": Page - 1Adarsh Rasal100% (1)

- NMIMS MUMBAI NAVI MUMBAI Student Activity Sponsorship and Exp - POLICYДокумент5 страницNMIMS MUMBAI NAVI MUMBAI Student Activity Sponsorship and Exp - POLICYRushil ShahОценок пока нет

- IPP Report PakistanДокумент296 страницIPP Report PakistanALI100% (1)

- Syllabus - Wills and SuccessionДокумент14 страницSyllabus - Wills and SuccessionJImlan Sahipa IsmaelОценок пока нет

- Policy On Emergency LoanДокумент3 страницыPolicy On Emergency LoanLancemachang EugenioОценок пока нет

- Mechanics of Futures MarketsДокумент42 страницыMechanics of Futures MarketsSidharth ChoudharyОценок пока нет

- LIC Jeevan Anand Plan PPT Nitin 359Документ11 страницLIC Jeevan Anand Plan PPT Nitin 359Nitin ShindeОценок пока нет

- SEDA (Application Form) Manual 425kWp Up To 1MW - 140514Документ13 страницSEDA (Application Form) Manual 425kWp Up To 1MW - 140514raghuram86Оценок пока нет

- Cio Rajeev Thakkar's Note On Parag Parikh Flexi Cap FundДокумент3 страницыCio Rajeev Thakkar's Note On Parag Parikh Flexi Cap FundSaswat PremОценок пока нет

- Spring 2006Документ40 страницSpring 2006ed bookerОценок пока нет

- Fundamental Analysis Project.Документ82 страницыFundamental Analysis Project.Ajay Rockson100% (1)

- T-Accounts E. Tria Systems ConsultantДокумент8 страницT-Accounts E. Tria Systems ConsultantAnya DaniellaОценок пока нет

- CONTRACT OF LEASE (Virgo)Документ7 страницCONTRACT OF LEASE (Virgo)Grebert Karl Jennelyn SisonОценок пока нет

- Inventory Trading SampleДокумент28 страницInventory Trading SampleRonald Victor Galarza Hermitaño0% (1)

- Strategic Plan of Indian Tobacco Company (ItcДокумент27 страницStrategic Plan of Indian Tobacco Company (ItcJennifer Smith100% (1)

- GPPB Reso 27-2012Документ3 страницыGPPB Reso 27-2012Ax Scribd100% (1)

- Notes # 2 - Fundamentals of Real Estate Management PDFДокумент3 страницыNotes # 2 - Fundamentals of Real Estate Management PDFGessel Xan Lopez100% (2)

- Veneracion v. Mancilla (2006)Документ2 страницыVeneracion v. Mancilla (2006)Andre Philippe RamosОценок пока нет

- Alagappa University DDE BBM First Year Financial Accounting Exam - Paper2Документ5 страницAlagappa University DDE BBM First Year Financial Accounting Exam - Paper2mansoorbariОценок пока нет

- Wymac CapitalДокумент1 страницаWymac Capitalmrobison7697Оценок пока нет

- Fabm2: Quarter 1 Module 1.2 New Normal ABM For Grade 12Документ19 страницFabm2: Quarter 1 Module 1.2 New Normal ABM For Grade 12Janna Gunio0% (1)

- Hair Salon Business Plan ExampleДокумент20 страницHair Salon Business Plan ExampleJamesnjiruОценок пока нет

- Kirsty Nathoo - Startup Finance Pitfalls and How To Avoid ThemДокумент33 страницыKirsty Nathoo - Startup Finance Pitfalls and How To Avoid ThemMurali MohanОценок пока нет

- Solutions To Exercises and Problems - Budgeting: GivenДокумент8 страницSolutions To Exercises and Problems - Budgeting: GivenTiến AnhОценок пока нет

- Value: The Four Cornerstones of Corporate FinanceОт EverandValue: The Four Cornerstones of Corporate FinanceРейтинг: 4.5 из 5 звезд4.5/5 (18)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelОт Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelОценок пока нет

- Joy of Agility: How to Solve Problems and Succeed SoonerОт EverandJoy of Agility: How to Solve Problems and Succeed SoonerРейтинг: 4 из 5 звезд4/5 (1)

- Angel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000От EverandAngel: How to Invest in Technology Startups-Timeless Advice from an Angel Investor Who Turned $100,000 into $100,000,000Рейтинг: 4.5 из 5 звезд4.5/5 (86)

- Finance Basics (HBR 20-Minute Manager Series)От EverandFinance Basics (HBR 20-Minute Manager Series)Рейтинг: 4.5 из 5 звезд4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaОт EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaРейтинг: 4.5 из 5 звезд4.5/5 (14)

- Venture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistОт EverandVenture Deals, 4th Edition: Be Smarter than Your Lawyer and Venture CapitalistРейтинг: 4.5 из 5 звезд4.5/5 (73)

- Product-Led Growth: How to Build a Product That Sells ItselfОт EverandProduct-Led Growth: How to Build a Product That Sells ItselfРейтинг: 5 из 5 звезд5/5 (1)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanОт EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanРейтинг: 4.5 из 5 звезд4.5/5 (79)

- Mastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsОт EverandMastering Private Equity: Transformation via Venture Capital, Minority Investments and BuyoutsОценок пока нет

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisОт EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisРейтинг: 5 из 5 звезд5/5 (6)

- Startup CEO: A Field Guide to Scaling Up Your Business (Techstars)От EverandStartup CEO: A Field Guide to Scaling Up Your Business (Techstars)Рейтинг: 4.5 из 5 звезд4.5/5 (4)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialОт EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialОценок пока нет

- Financial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityОт EverandFinancial Modeling and Valuation: A Practical Guide to Investment Banking and Private EquityРейтинг: 4.5 из 5 звезд4.5/5 (4)

- Note Brokering for Profit: Your Complete Work At Home Success ManualОт EverandNote Brokering for Profit: Your Complete Work At Home Success ManualОценок пока нет

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursОт EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursРейтинг: 4.5 из 5 звезд4.5/5 (34)

- Financial Risk Management: A Simple IntroductionОт EverandFinancial Risk Management: A Simple IntroductionРейтинг: 4.5 из 5 звезд4.5/5 (7)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNОт Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNРейтинг: 4.5 из 5 звезд4.5/5 (3)

- These Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaОт EverandThese Are the Plunderers: How Private Equity Runs—and Wrecks—AmericaРейтинг: 3.5 из 5 звезд3.5/5 (8)

- Add Then Multiply: How small businesses can think like big businesses and achieve exponential growthОт EverandAdd Then Multiply: How small businesses can think like big businesses and achieve exponential growthОценок пока нет

- Warren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorОт EverandWarren Buffett Book of Investing Wisdom: 350 Quotes from the World's Most Successful InvestorОценок пока нет

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingОт EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingРейтинг: 4.5 из 5 звезд4.5/5 (17)

- Investment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionОт EverandInvestment Valuation: Tools and Techniques for Determining the Value of any Asset, University EditionРейтинг: 5 из 5 звезд5/5 (1)

- Burn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialОт EverandBurn the Boats: Toss Plan B Overboard and Unleash Your Full PotentialРейтинг: 4.5 из 5 звезд4.5/5 (32)