Вам также может понравиться

- Tata Focused Equity Fund KimДокумент40 страницTata Focused Equity Fund KimMohit GandhiОценок пока нет

- Monthly Dividend Distribution HKДокумент58 страницMonthly Dividend Distribution HKwayne.ilearnacadhkОценок пока нет

- Ameritrade Decker Feb 2020Документ3 страницыAmeritrade Decker Feb 2020Patty Morrarty24Оценок пока нет

- Etsy Investor-Presentation-1Q20 - Final-VersionДокумент47 страницEtsy Investor-Presentation-1Q20 - Final-VersionOleksandr YaroshenkoОценок пока нет

- 21 ACR Series L Series M and Series N CP Final Prospectus DTD 08202020Документ128 страниц21 ACR Series L Series M and Series N CP Final Prospectus DTD 08202020MisshtaCОценок пока нет

- Investments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsОт EverandInvestments Profitability, Time Value & Risk Analysis: Guidelines for Individuals and CorporationsОценок пока нет

- Covid-19-Financial-Reporting-And-Disclosures GTДокумент12 страницCovid-19-Financial-Reporting-And-Disclosures GTDhruba AdhikariОценок пока нет

- Zerodha Nifty LargeMidcap 250 Index Fund - SIDДокумент100 страницZerodha Nifty LargeMidcap 250 Index Fund - SIDBALAJiОценок пока нет

- SBR Revision (Analysis)Документ41 страницаSBR Revision (Analysis)Ling Xuan ChinОценок пока нет

- Bluechip FundDC58F14BAF2FДокумент56 страницBluechip FundDC58F14BAF2Fharpreet singhОценок пока нет

- IE00BL643144 en KIIDs 0Документ2 страницыIE00BL643144 en KIIDs 0duc anhОценок пока нет

- TriQuint RFMD Merger Investor PresentationДокумент11 страницTriQuint RFMD Merger Investor PresentationspeedybitsОценок пока нет

- PRI InvestingwithSDGoutcomes Afive-PartframeworkДокумент34 страницыPRI InvestingwithSDGoutcomes Afive-Partframeworktradingjournal888Оценок пока нет

- Kiidoc 2020 02 24 en Lu 2020 02 24 Lu1744468221 YcapfundДокумент2 страницыKiidoc 2020 02 24 en Lu 2020 02 24 Lu1744468221 Ycapfundmatthieu massieОценок пока нет

- Canara Robeco InDiGo Fund NFO FormДокумент8 страницCanara Robeco InDiGo Fund NFO Formrkdgr87880Оценок пока нет

- NALUPTA, Raoul Arnaldo P. - K32 - ACYAVA2 - TermPaperДокумент7 страницNALUPTA, Raoul Arnaldo P. - K32 - ACYAVA2 - TermPaperRaoul Arnaldo Primicias NaluptaОценок пока нет

- DSP Blackrock Tax Saver Fund KimДокумент22 страницыDSP Blackrock Tax Saver Fund KimPRANUОценок пока нет

- Analytical VaR VaR MappingДокумент13 страницAnalytical VaR VaR MappingFuad SheikhОценок пока нет

- The Management 10 KgsДокумент14 страницThe Management 10 KgsskimbryОценок пока нет

- Apec AssignmentДокумент17 страницApec AssignmentHOPE MAKAUОценок пока нет

- Kiid Emqq IE00BFYN8Y92 en GBДокумент2 страницыKiid Emqq IE00BFYN8Y92 en GBMónica CletoОценок пока нет

- Key Investor Information: Vanguard Lifestrategy® 20% Equity Fund (The "Fund")Документ2 страницыKey Investor Information: Vanguard Lifestrategy® 20% Equity Fund (The "Fund")Cristian GherghiţăОценок пока нет

- MUKUNDДокумент10 страницMUKUNDMukund SharmaОценок пока нет

- Prumill at Age 50Документ5 страницPrumill at Age 50Robert RОценок пока нет

- WASTE-TO-ENERGY Information Memerandum DT 12 Apr, 2020Документ42 страницыWASTE-TO-ENERGY Information Memerandum DT 12 Apr, 2020RST0% (1)

- Project Power Announcement Deck - VFДокумент45 страницProject Power Announcement Deck - VFKamilo ArtmandОценок пока нет

- Saratoga Investor Relation Presentation 9M19 Final - PublicДокумент15 страницSaratoga Investor Relation Presentation 9M19 Final - Publicsigitsutoko8765Оценок пока нет

- Data For DevelopmentДокумент6 страницData For DevelopmentJigar DesaiОценок пока нет

- Investing With SDG Outcomes:: A Five-Part FrameworkДокумент34 страницыInvesting With SDG Outcomes:: A Five-Part FrameworkMichele AzevedoОценок пока нет

- Presentation For Mix Use FinДокумент5 страницPresentation For Mix Use FinalvahОценок пока нет

- A First Look at The Impact of COVID-19 oДокумент47 страницA First Look at The Impact of COVID-19 oMajid Shahzaad KharralОценок пока нет

- TFMP Series 34 BДокумент16 страницTFMP Series 34 BdevangbpОценок пока нет

- RM-MTP M22Документ10 страницRM-MTP M22Mani ganesanОценок пока нет

- Mohan's Task-3Документ5 страницMohan's Task-3Pampana Bala Sai Saroj RamОценок пока нет

- 1624021914-Scheme Information Document ITI Dynamic Bond FundДокумент82 страницы1624021914-Scheme Information Document ITI Dynamic Bond FundAishwarya ShindeОценок пока нет

- Public-Private Investing - Fixed Income at A Crossroads - Neuberger Berman (2021)Документ7 страницPublic-Private Investing - Fixed Income at A Crossroads - Neuberger Berman (2021)sherОценок пока нет

- Reitbz WhitepaperДокумент37 страницReitbz WhitepaperDanz HolandezОценок пока нет

- Konkrete Information Memorandum v2.5Документ54 страницыKonkrete Information Memorandum v2.5Estate BaronОценок пока нет

- Farmland Investment Report 2012 - DGC Asset ManagementДокумент39 страницFarmland Investment Report 2012 - DGC Asset ManagementTrang NguyenОценок пока нет

- Villa Green Investment PackageДокумент51 страницаVilla Green Investment Packagegarry435Оценок пока нет

- (ACYFAR2) Toribio Critique PaperДокумент11 страниц(ACYFAR2) Toribio Critique PaperHannah Jane ToribioОценок пока нет

- BPI Global Equity Fund of Funds - September 2023 v2Документ4 страницыBPI Global Equity Fund of Funds - September 2023 v2Ramon VinzonОценок пока нет

- Iti Liquid Fund: Key Information Memorandum Cum Application FormДокумент32 страницыIti Liquid Fund: Key Information Memorandum Cum Application FormspeedenquiryОценок пока нет

- Interest Rate Model and Gradation of RiskДокумент8 страницInterest Rate Model and Gradation of Riskiam streetdog7Оценок пока нет

- Citigroup Research PaperДокумент4 страницыCitigroup Research Paperzqbyvtukg100% (1)

- 2020 Cat DatabookДокумент21 страница2020 Cat DatabookshivОценок пока нет

- Essentials of Private Markets Brochure InternationalДокумент12 страницEssentials of Private Markets Brochure Internationalrahul raiОценок пока нет

- Kotak Technology Fund FAQsДокумент4 страницыKotak Technology Fund FAQsjayalekshmicvОценок пока нет

- Key Information and Investment Disclosure Statement: Metro World Equity Feeder FundДокумент3 страницыKey Information and Investment Disclosure Statement: Metro World Equity Feeder FundMartin MartelОценок пока нет

- TrucostIFC Emerging Markets ReportДокумент20 страницTrucostIFC Emerging Markets ReportIFC SustainabilityОценок пока нет

- 1up1 - IShares - SandP500Документ2 страницы1up1 - IShares - SandP500Antonio MaticОценок пока нет

- Equity ManagementДокумент20 страницEquity ManagementHazel HizoleОценок пока нет

- Impact Frontier Case Study Publication 1Документ33 страницыImpact Frontier Case Study Publication 1barkeshlimoОценок пока нет

- Dhiraagu IPO Prospectus - English EditionДокумент110 страницDhiraagu IPO Prospectus - English EditionDhiraagu Marcoms100% (2)

- Key Investor Information: Vanguard S&P 500 UCITS ETF (The "Fund")Документ2 страницыKey Investor Information: Vanguard S&P 500 UCITS ETF (The "Fund")Antonio Rodríguez de la TorreОценок пока нет

- Investments TheoryДокумент8 страницInvestments TheoryralphalonzoОценок пока нет

- Bravo Cross Asset Manager Presentation PDFДокумент32 страницыBravo Cross Asset Manager Presentation PDFakarastОценок пока нет

- 1st Midterm Quiz QuestionnaireДокумент11 страниц1st Midterm Quiz QuestionnaireAthena Fatmah AmpuanОценок пока нет

- LDK Solar Co., LTD.: Research ReportДокумент8 страницLDK Solar Co., LTD.: Research ReportXiong LinОценок пока нет

- AARS Practice QuestionsДокумент211 страницAARS Practice QuestionsChaudhury Ahmed HabibОценок пока нет

- Civic and Ethical Education Lesson Note Prepared For Grade 11Документ3 страницыCivic and Ethical Education Lesson Note Prepared For Grade 11Bereket MekonnenОценок пока нет

- Hazard and Risk Assessment PDFДокумент99 страницHazard and Risk Assessment PDFjanisha11Оценок пока нет

- Long Term Care Facilities Final ReportДокумент157 страницLong Term Care Facilities Final ReportPeter YankowskiОценок пока нет

- HIRARC On ConstructionДокумент33 страницыHIRARC On ConstructionMohd Zulhaidy85% (33)

- Jurnal Dinda SalsabilaДокумент13 страницJurnal Dinda SalsabilaFebrianti NatasyaОценок пока нет

- The Political Economy of UHCДокумент44 страницыThe Political Economy of UHCMuhammad HasbiОценок пока нет

- AWS Auditing Security Checklist PDFДокумент28 страницAWS Auditing Security Checklist PDFnandaanujОценок пока нет

- Insider Threat Report May 2020 SecuronixДокумент13 страницInsider Threat Report May 2020 SecuronixDebarati GuptaОценок пока нет

- Nature and The Insurance Industry - Taking Action Towards A Nature-Positive EconomyДокумент64 страницыNature and The Insurance Industry - Taking Action Towards A Nature-Positive EconomycaranpaimaОценок пока нет

- Aqap 2310 2017 Eng en DataДокумент34 страницыAqap 2310 2017 Eng en Data신동득Оценок пока нет

- Guideline For Preparing Comprehensive Extension of Time (EoT) ClaimДокумент9 страницGuideline For Preparing Comprehensive Extension of Time (EoT) Claimgrtuna100% (1)

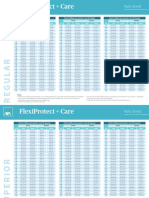

- Flexi+Care Rate SheetДокумент3 страницыFlexi+Care Rate SheetNeil MijaresОценок пока нет

- Wake Up Call El Nino Unicef Report FinalДокумент8 страницWake Up Call El Nino Unicef Report FinalsofiabloemОценок пока нет

- CM in T.L.E 7-9Документ20 страницCM in T.L.E 7-9Rio Eden AntopinaОценок пока нет

- 1624 - Corporate Transfer PolicyДокумент16 страниц1624 - Corporate Transfer PolicySyamsul ArifinОценок пока нет

- BS 9997 2019 - Fire Risk Management SystemsДокумент54 страницыBS 9997 2019 - Fire Risk Management SystemsLauryn Amara83% (12)

- Ameg - 212 - 003 - Course OutlineДокумент9 страницAmeg - 212 - 003 - Course OutlineAlex ChrisОценок пока нет

- RISK ASESSMENT For Grit Blasting and PaintingДокумент18 страницRISK ASESSMENT For Grit Blasting and Paintingadeoye Adeyemi100% (1)

- Requirements ElicitationДокумент26 страницRequirements ElicitationAfifa AzamОценок пока нет

- Madness, Inc.: How College Sports Leave Athletes Broken and AbandonedДокумент21 страницаMadness, Inc.: How College Sports Leave Athletes Broken and AbandonedLia AlbiniОценок пока нет

- Drilling Process Safety 101Документ10 страницDrilling Process Safety 101Saad GhouriОценок пока нет

- Financi Al Instrum Ents: Financial Market: Trends and IssuesДокумент41 страницаFinanci Al Instrum Ents: Financial Market: Trends and IssuesEunice Dimple CaliwagОценок пока нет

- Portfolio Monitoring (JOIM)Документ14 страницPortfolio Monitoring (JOIM)Nicolas Lefevre-LaumonierОценок пока нет

- Measuring ResilienceДокумент51 страницаMeasuring ResilienceLogmanОценок пока нет

- Austrian Practice of - Tunnelling Contracts - Engl PDFДокумент42 страницыAustrian Practice of - Tunnelling Contracts - Engl PDFMilan UljarevicОценок пока нет

- CRM Bangladeh Bank-2015Документ54 страницыCRM Bangladeh Bank-2015sayedrushdiОценок пока нет

- Communication Management Plan Template1Документ24 страницыCommunication Management Plan Template1Abdulrahman AlnasharОценок пока нет

- 5 Risk Based AuditДокумент93 страницы5 Risk Based AuditAnonymous jlLBRMAr3OОценок пока нет

- Chapter 6 Contemporary Issues in EngineeringДокумент43 страницыChapter 6 Contemporary Issues in EngineeringsantoshОценок пока нет