Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Quality Audit (Inspection)Документ3 страницыQuality Audit (Inspection)Crescent OsamuОценок пока нет

- The UN Charter: The 70th Anniversary: Trusteeship CouncilДокумент6 страницThe UN Charter: The 70th Anniversary: Trusteeship CouncilCrescent OsamuОценок пока нет

- I. Accounting Methods For By-Products: Exercise 3Документ2 страницыI. Accounting Methods For By-Products: Exercise 3Crescent OsamuОценок пока нет

- The Only OneДокумент1 страницаThe Only OneCrescent OsamuОценок пока нет

- SSHistoryДокумент38 страницSSHistoryCrescent OsamuОценок пока нет

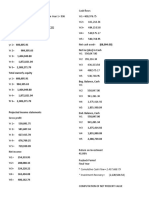

- Net Inc (Dec) in Cash: Investment Recovery (2,220,504.54)Документ2 страницыNet Inc (Dec) in Cash: Investment Recovery (2,220,504.54)Crescent OsamuОценок пока нет

- DocumentДокумент1 страницаDocumentCrescent OsamuОценок пока нет

- ReminiscenceДокумент2 страницыReminiscenceCrescent OsamuОценок пока нет

- Contemporary PhilosophyДокумент46 страницContemporary PhilosophyCrescent OsamuОценок пока нет

- Examples in SentencesДокумент3 страницыExamples in SentencesCrescent OsamuОценок пока нет

- Get A Driver's License: Finish My BookДокумент2 страницыGet A Driver's License: Finish My BookCrescent OsamuОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Stock Market Basics: What Beginner Investors Should KnowДокумент95 страницStock Market Basics: What Beginner Investors Should KnowPANKAJ SHUKLA100% (1)

- Swing Trading Simplified Larry D Spears PDFДокумент115 страницSwing Trading Simplified Larry D Spears PDFAmine Elghazi100% (4)

- MC 9 Equity A201 StudentДокумент4 страницыMC 9 Equity A201 StudentKkk.sssОценок пока нет

- Equity Valuation Models and Target Price Accuray in EuropeДокумент11 страницEquity Valuation Models and Target Price Accuray in EuropeHS Maika Duong NguyenОценок пока нет

- Demat AccountДокумент82 страницыDemat AccountJASONM2250% (4)

- Idx Statistics 2009 - q4Документ109 страницIdx Statistics 2009 - q4kusumo_bongsoОценок пока нет

- Name: Theng Kimay Class: Year: T204Документ4 страницыName: Theng Kimay Class: Year: T204ALex LimОценок пока нет

- Dividend Policy at Linear Technology - Case Analysis - G05Документ2 страницыDividend Policy at Linear Technology - Case Analysis - G05Srikanth Kumar Konduri60% (5)

- Relative Valuations FINALДокумент44 страницыRelative Valuations FINALChinmay ShirsatОценок пока нет

- FORM 23-B: Securities and Exchange Commission Metro Manila, PhilippinesДокумент2 страницыFORM 23-B: Securities and Exchange Commission Metro Manila, PhilippinesJulius Mark Carinhay TolitolОценок пока нет

- Mutual Funds Correction PDFДокумент48 страницMutual Funds Correction PDFPrethesh JainОценок пока нет

- Quiz 3 CFS Subsequent To Date of AcquisitionДокумент3 страницыQuiz 3 CFS Subsequent To Date of AcquisitionJi Eun VinceОценок пока нет

- General Information About CompanyДокумент27 страницGeneral Information About CompanyVikaas ChouhanОценок пока нет

- Chapter 13 International Equity Markets Answers & Solutions To End-Of-Chapter Questions and ProblemsДокумент5 страницChapter 13 International Equity Markets Answers & Solutions To End-Of-Chapter Questions and ProblemsAnthony White0% (1)

- Floating A Company: Corporate Financial Strategy 4th Edition DR Ruth BenderДокумент20 страницFloating A Company: Corporate Financial Strategy 4th Edition DR Ruth BenderAin roseОценок пока нет

- 37 Key Basic Stock Market TermsДокумент6 страниц37 Key Basic Stock Market TermsArlen Mae RayosОценок пока нет

- Chapter 10 Shareholders EquityДокумент10 страницChapter 10 Shareholders EquityMarine De CocquéauОценок пока нет

- Analisis Rasio PT Nippon Indosari Corpindo TBKДокумент3 страницыAnalisis Rasio PT Nippon Indosari Corpindo TBKAkilОценок пока нет

- Capital MarketДокумент32 страницыCapital MarketAppan Kandala Vasudevachary80% (5)

- Abhinav Mansingh KaДокумент18 страницAbhinav Mansingh Kaarif420_999Оценок пока нет

- Intraday & Investment: Multi-Beggars StocksДокумент5 страницIntraday & Investment: Multi-Beggars StocksNchdhrfОценок пока нет

- Angel Broking - Wikipedia Hsushsb Jsis Enthi SunДокумент20 страницAngel Broking - Wikipedia Hsushsb Jsis Enthi SunYuga NayakОценок пока нет

- Stock MarketДокумент3 страницыStock MarketUPPULAОценок пока нет

- ANALYSIS OF SELECT FMCG COMPANIESâ ™ STOCK PERFORMANCE WITH MARKET-2Документ8 страницANALYSIS OF SELECT FMCG COMPANIESâ ™ STOCK PERFORMANCE WITH MARKET-2AravindTimeTravellerОценок пока нет

- Assignment On Corporation (Najeeb)Документ5 страницAssignment On Corporation (Najeeb)Najeeb KhanОценок пока нет

- IDX Fact Book 2009Документ166 страницIDX Fact Book 2009Mhd FadilОценок пока нет

- Accounting For Treasury SharesДокумент2 страницыAccounting For Treasury SharesCharles Reginald K. Hwang100% (1)

- SP Capital IQДокумент11 страницSP Capital IQemirav2100% (1)

- Bhanu 10809861Документ127 страницBhanu 10809861bhanuguptaОценок пока нет

- Online TradingДокумент76 страницOnline TradingTech YuvaОценок пока нет