Вам также может понравиться

- Toward Inclusive Access to Trade Finance: Lessons from the Trade Finance Gaps, Growth, and Jobs SurveyОт EverandToward Inclusive Access to Trade Finance: Lessons from the Trade Finance Gaps, Growth, and Jobs SurveyОценок пока нет

- Sai NathДокумент6 страницSai NathLinda MartinОценок пока нет

- MWiI TOC and SummДокумент10 страницMWiI TOC and Summaartig333Оценок пока нет

- Icici CaseДокумент2 страницыIcici CaseDebi PrasannaОценок пока нет

- Case Study Global Crossing Services Assignment 1 GDSДокумент5 страницCase Study Global Crossing Services Assignment 1 GDSGaurav DuttОценок пока нет

- HDFC Bank Summer ReportДокумент55 страницHDFC Bank Summer Reportilover_140085% (20)

- BANKING Sector India and Swot AnalysisДокумент16 страницBANKING Sector India and Swot AnalysisPrateek Rastogi93% (14)

- Chapter - 1: 1.1 General Introduction About The SectorДокумент23 страницыChapter - 1: 1.1 General Introduction About The SectorAnkur ChopraОценок пока нет

- Professional Wealth ManagementДокумент4 страницыProfessional Wealth ManagementAbhinav JainОценок пока нет

- Nishi Gupta - Idbi BankДокумент40 страницNishi Gupta - Idbi BankNitinAgnihotriОценок пока нет

- Group No. 37 - CRДокумент28 страницGroup No. 37 - CRsoumyaОценок пока нет

- Top of Form Bottom of FormДокумент44 страницыTop of Form Bottom of FormKrishna RajuОценок пока нет

- Project On HDFC BankДокумент72 страницыProject On HDFC Banksunit2658Оценок пока нет

- A Project Report On Comparison Between HDFC Bank Amp Icici BankДокумент75 страницA Project Report On Comparison Between HDFC Bank Amp Icici BankSAHIL AGNIHOTRIОценок пока нет

- A Project Report On Comparison Between HDFC Bank & ICICI BankДокумент75 страницA Project Report On Comparison Between HDFC Bank & ICICI Bankvarun_bawa25191592% (12)

- SM DraftДокумент20 страницSM DraftAnoushka GhorpadeОценок пока нет

- TOI - Corporate Foreign Debt Not A WorryДокумент5 страницTOI - Corporate Foreign Debt Not A Worrykarthik sОценок пока нет

- Project Report BobДокумент30 страницProject Report Bobmegha rathore100% (1)

- Indian Banking Sector ReportДокумент59 страницIndian Banking Sector Reportraviawade100% (2)

- Submitted in Partial Fulfillment For The Degree Of: Project Study Report OnДокумент37 страницSubmitted in Partial Fulfillment For The Degree Of: Project Study Report OnUsha GiriОценок пока нет

- Introduction of Banking IndustryДокумент15 страницIntroduction of Banking IndustryArchana Mishra100% (1)

- Nitu Tybbi ProjectДокумент64 страницыNitu Tybbi ProjectRupal Rohan DalalОценок пока нет

- Project Vijaya Bank FinalДокумент62 страницыProject Vijaya Bank FinalNalina Gs G100% (1)

- UntitledДокумент8 страницUntitledJohnson VaidyaОценок пока нет

- Tag Dbs Treasury Management India PDFДокумент27 страницTag Dbs Treasury Management India PDFDipak DwivediОценок пока нет

- Final Project of Indusind BankДокумент104 страницыFinal Project of Indusind Banknikhil chikhaleОценок пока нет

- Comparative Study of Top 5 Banks in IndiaДокумент11 страницComparative Study of Top 5 Banks in Indiajakharpardeepjakhar_Оценок пока нет

- Internationalization Challenges For Companies in Emerging Markets PDFДокумент4 страницыInternationalization Challenges For Companies in Emerging Markets PDFjainashish1008Оценок пока нет

- Investment Theory and AnalysisДокумент8 страницInvestment Theory and AnalysisJinky Bago AcapuyanОценок пока нет

- A Project Report On Employees Satisfaction Regarding HDFC BankДокумент77 страницA Project Report On Employees Satisfaction Regarding HDFC Bankvarun_bawa25191578% (23)

- Project Report Bank of Baroda: Holy Family Junior CollegeДокумент14 страницProject Report Bank of Baroda: Holy Family Junior CollegeFloydCorreaОценок пока нет

- Bank of IndiaДокумент22 страницыBank of IndiaLeeladhar Nagar100% (1)

- AmalgamationДокумент50 страницAmalgamationNikesh KothariОценок пока нет

- Banking & Finance Sector-OpportunityforHitachiДокумент25 страницBanking & Finance Sector-OpportunityforHitachiNeeraj KumarОценок пока нет

- Thesis Topic On Banking SectorДокумент4 страницыThesis Topic On Banking Sectorstaceycruzwashington100% (1)

- Spellchecked - Mba - Project - Mergers and AquisitionsДокумент107 страницSpellchecked - Mba - Project - Mergers and AquisitionsDanturthi RamachandruduОценок пока нет

- Banking at HDFCДокумент68 страницBanking at HDFCramОценок пока нет

- FK 3039Документ24 страницыFK 3039psy mediaОценок пока нет

- Indian Financial SystemsДокумент6 страницIndian Financial SystemsParang MehtaОценок пока нет

- Synopsis ON Credit Risk Management IN: Pooja Arora 140423533Документ6 страницSynopsis ON Credit Risk Management IN: Pooja Arora 140423533Pooja AroraОценок пока нет

- Sam College of Management and Technology BhopalДокумент48 страницSam College of Management and Technology Bhopalvidhya associateОценок пока нет

- Banking Term PaperДокумент18 страницBanking Term PaperSangeeta ChakiОценок пока нет

- CC CCC CCCCCCCCC CCCC CC C CДокумент42 страницыCC CCC CCCCCCCCC CCCC CC C CYuvraj KharchaneОценок пока нет

- Public Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesОт EverandPublic Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesОценок пока нет

- Guidance Note on State-Owned Enterprise Reform for Nonsovereign and One ADB ProjectsОт EverandGuidance Note on State-Owned Enterprise Reform for Nonsovereign and One ADB ProjectsОценок пока нет

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexОт EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexОценок пока нет

- The Bankable SOE: Commercial Financing for State-Owned EnterprisesОт EverandThe Bankable SOE: Commercial Financing for State-Owned EnterprisesОценок пока нет

- Financing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesОт EverandFinancing Small and Medium-Sized Enterprises in Asia and the Pacific: Credit Guarantee SchemesОценок пока нет

- Inclusive Business in Financing: Where Commercial Opportunity and Sustainability ConvergeОт EverandInclusive Business in Financing: Where Commercial Opportunity and Sustainability ConvergeОценок пока нет

- Inclusive Business Market Scoping Study in the People's Republic of ChinaОт EverandInclusive Business Market Scoping Study in the People's Republic of ChinaОценок пока нет

- Summary of Saurabh Mukherjea, Rakshit Ranjan & Salil Desai's Diamonds in the DustОт EverandSummary of Saurabh Mukherjea, Rakshit Ranjan & Salil Desai's Diamonds in the DustОценок пока нет

- Banking India: Accepting Deposits for the Purpose of LendingОт EverandBanking India: Accepting Deposits for the Purpose of LendingОценок пока нет

- Green Bond Market Survey for the Lao People's Democratic Republic: Insights on the Perspectives of Institutional Investors and UnderwritersОт EverandGreen Bond Market Survey for the Lao People's Democratic Republic: Insights on the Perspectives of Institutional Investors and UnderwritersОценок пока нет

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume I: Country and Regional ReviewsОт EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume I: Country and Regional ReviewsОценок пока нет

- Securitization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsОт EverandSecuritization in India: Managing Capital Constraints and Creating Liquidity to Fund Infrastructure AssetsОценок пока нет

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume III: Thematic Chapter—Fintech Loans to Tricycle Drivers in the PhilippinesОт EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume III: Thematic Chapter—Fintech Loans to Tricycle Drivers in the PhilippinesОценок пока нет

- Demystifying Venture Capital: How It Works and How to Get ItОт EverandDemystifying Venture Capital: How It Works and How to Get ItОценок пока нет

- The Asian Bond Markets Initiative: Policy Maker Achievements and ChallengesОт EverandThe Asian Bond Markets Initiative: Policy Maker Achievements and ChallengesОценок пока нет

- Chandragupt Institute of Management PatnaДокумент8 страницChandragupt Institute of Management PatnaTanu SinghОценок пока нет

- Senior Profile Merged - 190920 - 16Документ1 страницаSenior Profile Merged - 190920 - 16Tanu SinghОценок пока нет

- The Project BackgroundДокумент6 страницThe Project BackgroundTanu SinghОценок пока нет

- Chandragupt Institute of Management Patna PGDM:2019-2021 BatchДокумент1 страницаChandragupt Institute of Management Patna PGDM:2019-2021 BatchTanu SinghОценок пока нет

- Creative Management: Shilpi Kumari Roll-120102 Section-BДокумент4 страницыCreative Management: Shilpi Kumari Roll-120102 Section-BTanu SinghОценок пока нет

- Chandrayaan-2 Mission: India's Mission To MoonДокумент12 страницChandrayaan-2 Mission: India's Mission To MoonTanu SinghОценок пока нет

- Chandrayaan-2 Mission: India's Mission To MoonДокумент12 страницChandrayaan-2 Mission: India's Mission To MoonTanu SinghОценок пока нет

- Group Discussion Group No Applicant ID Candidate NameДокумент8 страницGroup Discussion Group No Applicant ID Candidate NameTanu SinghОценок пока нет

- Https WWW - Finlatics.com Pdfs Certificates 16328 CertificateДокумент1 страницаHttps WWW - Finlatics.com Pdfs Certificates 16328 CertificateTanu SinghОценок пока нет

- It For Managers: Analysis of MotorolaДокумент13 страницIt For Managers: Analysis of MotorolaTanu SinghОценок пока нет

- Sector Project 1: Telcom: Bargaining Power of Buyers - Generally The Two Types of Buyer in Telecom Industry IncludesДокумент2 страницыSector Project 1: Telcom: Bargaining Power of Buyers - Generally The Two Types of Buyer in Telecom Industry IncludesTanu SinghОценок пока нет

- Research Insight: 1: A Research Report of Telecom Sector ON Bharti Airtel LimitedДокумент16 страницResearch Insight: 1: A Research Report of Telecom Sector ON Bharti Airtel LimitedTanu SinghОценок пока нет

- Career Objective Academic Credentials: TH THДокумент1 страницаCareer Objective Academic Credentials: TH THTanu SinghОценок пока нет

- Make in India Initiative: A Key For Sustainable Growth: December 2017Документ9 страницMake in India Initiative: A Key For Sustainable Growth: December 2017Tanu SinghОценок пока нет

- Research Insight: 2: A Research Report of Telecom Sector ON Tata Communications LimitedДокумент9 страницResearch Insight: 2: A Research Report of Telecom Sector ON Tata Communications LimitedTanu SinghОценок пока нет

- Career Objective: TH THДокумент1 страницаCareer Objective: TH THTanu SinghОценок пока нет

- J1103015962 PDFДокумент4 страницыJ1103015962 PDFTanu SinghОценок пока нет

- Porter'S Five Forces (Banking and Finance)Документ2 страницыPorter'S Five Forces (Banking and Finance)Tanu SinghОценок пока нет

- Eshghi Kamran Finalsubmission2018december PHDДокумент295 страницEshghi Kamran Finalsubmission2018december PHDTanu SinghОценок пока нет

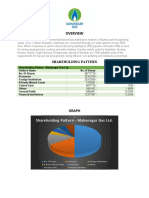

- Shareholding Patt Ern - Mahanagar Gas LTDДокумент4 страницыShareholding Patt Ern - Mahanagar Gas LTDTanu SinghОценок пока нет

- Consumers Product Preference & Perceived RiskДокумент2 страницыConsumers Product Preference & Perceived RiskTanu SinghОценок пока нет

- TMTCP Team 45 DenmarkДокумент16 страницTMTCP Team 45 DenmarkTanu SinghОценок пока нет

- Consumers Product Preference & Perceived RiskДокумент2 страницыConsumers Product Preference & Perceived RiskTanu SinghОценок пока нет

- A Case Study On QTДокумент8 страницA Case Study On QTTanu SinghОценок пока нет

- My: Optima SecureДокумент4 страницыMy: Optima SecureDr Ankit PardhiОценок пока нет

- PROBLEMSДокумент19 страницPROBLEMSlalalalaОценок пока нет

- Fee Voucher Fee Voucher Fee Voucher Voucher # 499276 Voucher # 499276 Voucher # 499276Документ1 страницаFee Voucher Fee Voucher Fee Voucher Voucher # 499276 Voucher # 499276 Voucher # 499276M Irfan IqbalОценок пока нет

- O o o O: Kulsuma Akter, 213571403364Документ8 страницO o o O: Kulsuma Akter, 213571403364azharul_islam_19Оценок пока нет

- Leases Part 2: Name: Date: Professor: Section: Score: Quiz 1Документ2 страницыLeases Part 2: Name: Date: Professor: Section: Score: Quiz 1Jamie Rose AragonesОценок пока нет

- A Guide To Help You Successfully Originate A New Loan in Encompass360Документ51 страницаA Guide To Help You Successfully Originate A New Loan in Encompass360Liang Wang100% (1)

- Hadiza Bala Usman's Access Bank Account StatementДокумент1 страницаHadiza Bala Usman's Access Bank Account StatementSahara ReportersОценок пока нет

- {89BA8282-2A04-42F1-8AA7-DD8575E809B3}Документ3 страницы{89BA8282-2A04-42F1-8AA7-DD8575E809B3}AlinaОценок пока нет

- BookdebtformatДокумент3 страницыBookdebtformatAnkit SoniОценок пока нет

- BAFL Audited Report For Dec 2020Документ98 страницBAFL Audited Report For Dec 2020MdZahidul IslamОценок пока нет

- The Essential Financial ToolkitДокумент12 страницThe Essential Financial ToolkitDr Abenet YohannesОценок пока нет

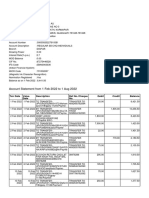

- Account Statement From 1 Feb 2022 To 1 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент11 страницAccount Statement From 1 Feb 2022 To 1 Aug 2022: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceFIRDUS ALIОценок пока нет

- Chapter5 IA Problems1 9Документ16 страницChapter5 IA Problems1 9Anonn100% (1)

- Accounting Paper 1Документ12 страницAccounting Paper 1Tenzin ChoekyОценок пока нет

- Summary Notes LiabilitiesДокумент2 страницыSummary Notes LiabilitiesCRISANGELОценок пока нет

- (A) Pancho Asked The Payor Bank To Recredit His Account. Should The Bank Comply? Explain Fully. (3%)Документ5 страниц(A) Pancho Asked The Payor Bank To Recredit His Account. Should The Bank Comply? Explain Fully. (3%)zhoy26Оценок пока нет

- HA3032 AuditingДокумент9 страницHA3032 AuditingAayam SubediОценок пока нет

- What Are Commercial BanksДокумент3 страницыWhat Are Commercial BanksShyam BahlОценок пока нет

- RED Academy: LedgerДокумент6 страницRED Academy: LedgerDila Ram PaudelОценок пока нет

- Pas 10 - Events After The Reporting PeriodДокумент11 страницPas 10 - Events After The Reporting PeriodBritnys Nim100% (1)

- Comparative Study On Mutual Funds and Fixed Deposits: An OverviewДокумент5 страницComparative Study On Mutual Funds and Fixed Deposits: An Overviewmaau DhawaleОценок пока нет

- Icici History of Industrial Credit and Investment Corporation of India (ICICI)Документ4 страницыIcici History of Industrial Credit and Investment Corporation of India (ICICI)Saadhana MuthuОценок пока нет

- The Accounting Cycle: Double Entry Book KeepingДокумент7 страницThe Accounting Cycle: Double Entry Book KeepingJunaid IslamОценок пока нет

- Exercise 4-6 Review Questions - Accounting Cycle and Accounting For Merchandising Part 1-10 Points Part 2 - 20 Points Part 3 - 10 PointsДокумент9 страницExercise 4-6 Review Questions - Accounting Cycle and Accounting For Merchandising Part 1-10 Points Part 2 - 20 Points Part 3 - 10 PointsAaron HuangОценок пока нет

- LIC AAO 2016 Capsule by AffairscloudДокумент84 страницыLIC AAO 2016 Capsule by AffairscloudRamesh RyОценок пока нет

- Proficiency - TheoryДокумент3 страницыProficiency - TheoryMJ YaconОценок пока нет

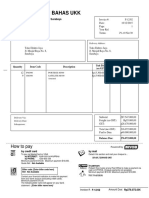

- Invoice Contoh PDFДокумент1 страницаInvoice Contoh PDFadebsbОценок пока нет

- Investment Calculator - SmartAssetДокумент1 страницаInvestment Calculator - SmartAssetSulemanОценок пока нет

- Principles of LendingДокумент2 страницыPrinciples of LendingWaqas TariqОценок пока нет

- FA1 NotesДокумент57 страницFA1 NotesellaОценок пока нет