Вам также может понравиться

- Alpine High Gloss Bed and Furniture CollectionДокумент70 страницAlpine High Gloss Bed and Furniture CollectionAnkita ChaudharyОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Roles Liabilities and Responsibilities of Directors in IndiaДокумент31 страницаRoles Liabilities and Responsibilities of Directors in IndiatenglumlowОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- WritsДокумент18 страницWritsAnkita ChaudharyОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- 13mfin010710 FДокумент83 страницы13mfin010710 FAnkita ChaudharyОценок пока нет

- Analyze SPSE Firm for InvestmentДокумент9 страницAnalyze SPSE Firm for Investmentmusuota0% (1)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Commonwealth Bank Financial AnalysisДокумент11 страницCommonwealth Bank Financial AnalysisMuhammad MubeenОценок пока нет

- Part1 SU1 2015 Rev2Документ86 страницPart1 SU1 2015 Rev2Mustafa Tevfik ÖzkanОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- FM NotesДокумент200 страницFM NotesRonit RoyОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- DellДокумент2 страницыDellJuhiОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- MenahilДокумент4 страницыMenahilsaudoryxОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Chapter Summary 2Документ28 страницChapter Summary 2Nimdorje SherpaОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Investment Scenario ExplainedДокумент37 страницInvestment Scenario ExplainedLokesh GowdaОценок пока нет

- 2784 PDFДокумент90 страниц2784 PDFemraan KhanОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- Kamco Dec 2015Документ7 страницKamco Dec 2015Waleed EhsanОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- 2019-20 Project ListДокумент20 страниц2019-20 Project ListPradeep KumarОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- When Markets Attack PDFДокумент228 страницWhen Markets Attack PDFYvan Ehouman100% (2)

- SharesДокумент26 страницSharesnaineshmuthaОценок пока нет

- Chapter 11 Solutions ManualДокумент52 страницыChapter 11 Solutions ManualJehan ZebОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Secondary Market Trading MechanicsДокумент13 страницSecondary Market Trading MechanicsDhushor SalimОценок пока нет

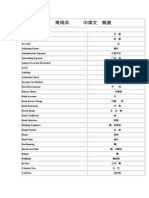

- 常用会计词汇中英文对照表Документ8 страниц常用会计词汇中英文对照表Owen ZhangОценок пока нет

- Exercise - Dilutive Securities - AdillaikhsaniДокумент4 страницыExercise - Dilutive Securities - Adillaikhsaniaidil fikri ikhsanОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Chapter 8 Stock ValuationДокумент35 страницChapter 8 Stock ValuationHamza KhalidОценок пока нет

- ABCDДокумент28 страницABCDAnonymous RUjsBRNMz100% (1)

- (PDF) APC - Ch9solДокумент11 страниц(PDF) APC - Ch9solAdam SmithОценок пока нет

- 03FM SM Ch3 1LPДокумент6 страниц03FM SM Ch3 1LPjoebloggs18880% (1)

- Key CH 7 HomeworkДокумент3 страницыKey CH 7 HomeworkCedrickBuenaventuraОценок пока нет

- Harsh Khandelwal - 21361 - Finance - Agile Capital Services PDFДокумент58 страницHarsh Khandelwal - 21361 - Finance - Agile Capital Services PDFChikun MarriageОценок пока нет

- Debabrata Mohanty, M.com, Sec A, (B.F), Regd - No-13351019 (Pondicherry University)Документ12 страницDebabrata Mohanty, M.com, Sec A, (B.F), Regd - No-13351019 (Pondicherry University)Andrew TaylorОценок пока нет

- Absolute Return Investing Strategies PDFДокумент8 страницAbsolute Return Investing Strategies PDFswopguruОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Financial Management Project of Askari BankДокумент32 страницыFinancial Management Project of Askari BankUsman Ali100% (1)

- Real Estate Buyer GuideДокумент18 страницReal Estate Buyer GuideJustin Huynh0% (1)

- Analysis of Value Destruction in ATT Acquisition of NCRДокумент26 страницAnalysis of Value Destruction in ATT Acquisition of NCRpektopОценок пока нет

- Analysing Profitability of Opening A Subway Sandwiches Franchise in StockbridgeДокумент23 страницыAnalysing Profitability of Opening A Subway Sandwiches Franchise in StockbridgeMonali PardeshiОценок пока нет

- Real Estate Investing EbookДокумент45 страницReal Estate Investing EbookQuang NguyenОценок пока нет