Вам также может понравиться

- Stating The Acquisition Process Part 1Документ3 страницыStating The Acquisition Process Part 1BhuwanОценок пока нет

- Valuation Part 1Документ3 страницыValuation Part 1BhuwanОценок пока нет

- Not A Single Employee of Zerodha Works With A Revenue Target - CEO - The Hindu BusinessLine PDFДокумент5 страницNot A Single Employee of Zerodha Works With A Revenue Target - CEO - The Hindu BusinessLine PDFDhiraj NemadeОценок пока нет

- M&A: Concepts and Theories: New York Institute of FinanceДокумент2 страницыM&A: Concepts and Theories: New York Institute of FinanceBhuwanОценок пока нет

- Going Public - DIY IPO'sДокумент6 страницGoing Public - DIY IPO'sThomas HoyОценок пока нет

- TABB Prop TradingДокумент5 страницTABB Prop TradingZerohedgeОценок пока нет

- The $100 Million Exit: Your Roadmap to the Ultimate PaydayОт EverandThe $100 Million Exit: Your Roadmap to the Ultimate PaydayРейтинг: 4 из 5 звезд4/5 (1)

- Ipo - SMCДокумент84 страницыIpo - SMCsaiyuvatechОценок пока нет

- Sequoia Transcript 2012Документ20 страницSequoia Transcript 2012EnterprisingInvestorОценок пока нет

- TranscriptДокумент4 страницыTranscriptMuhammad Saleh Masaud80% (5)

- Fig Gold Man 120611 Final2Документ27 страницFig Gold Man 120611 Final2aadricapitalОценок пока нет

- Your First Government Contract: Capture and Proposal WritingОт EverandYour First Government Contract: Capture and Proposal WritingОценок пока нет

- Insurance Industry Current Trends and DirectionsДокумент10 страницInsurance Industry Current Trends and DirectionsCheong Yook HarОценок пока нет

- IPO Basics Tutorial: (Page 1 of 7)Документ7 страницIPO Basics Tutorial: (Page 1 of 7)Naoo AlbaloshiОценок пока нет

- Saurabh MukherjeaДокумент8 страницSaurabh MukherjeaGurjeevОценок пока нет

- InvestopediaДокумент7 страницInvestopediaakhaveОценок пока нет

- Deloitte IPO GuidebookДокумент112 страницDeloitte IPO GuidebookmaoyangОценок пока нет

- The Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseОт EverandThe Small-Business Guide to Government Contracts: How to Comply with the Key Rules and Regulations . . . and Avoid Terminated Agreements, Fines, or WorseОценок пока нет

- ESP EssayДокумент2 страницыESP EssayHuong Lien NguyenОценок пока нет

- Three Ways M A Vallue Part TwoДокумент5 страницThree Ways M A Vallue Part TwoBhuwanОценок пока нет

- Survival Investing: How to Prosper Amid Thieving Banks and Corrupt GovernmentsОт EverandSurvival Investing: How to Prosper Amid Thieving Banks and Corrupt GovernmentsРейтинг: 3.5 из 5 звезд3.5/5 (3)

- Interview Reveals Private Equity's Dependence on Tax CodeДокумент5 страницInterview Reveals Private Equity's Dependence on Tax CodeBradley EvansОценок пока нет

- Choosing The Right Entity For Your Emerging Growth CompanyДокумент24 страницыChoosing The Right Entity For Your Emerging Growth CompanyflastergreenbergОценок пока нет

- Implied Terms and Good Faith in ContractsДокумент3 страницыImplied Terms and Good Faith in ContractsLena WassilianОценок пока нет

- INEG Questions on Wall Street FilmsДокумент4 страницыINEG Questions on Wall Street FilmsAmayaMeloJuanPabloОценок пока нет

- SubtitleДокумент2 страницыSubtitleBlack LotusОценок пока нет

- Subject 1: Human Resource ManagementДокумент6 страницSubject 1: Human Resource Managementsaurav jhaОценок пока нет

- Ipo PDFДокумент7 страницIpo PDFGoutam ReddyОценок пока нет

- Market Not Very Far From New HighДокумент5 страницMarket Not Very Far From New HighshahpinkalОценок пока нет

- Valuation Thesis: Target Corp.: Corporate Finance IIДокумент22 страницыValuation Thesis: Target Corp.: Corporate Finance IIagusОценок пока нет

- Case Study Joint VentureДокумент8 страницCase Study Joint VentureShanta IslamОценок пока нет

- Where Have All The Startup Hedgehogs Gone - OcrДокумент6 страницWhere Have All The Startup Hedgehogs Gone - OcrApoorv SarveshОценок пока нет

- Factors That Contributed To Growth of Indian LeasingДокумент5 страницFactors That Contributed To Growth of Indian LeasingRAKESH SHARMA100% (3)

- Buffett and Munger On MoatsДокумент18 страницBuffett and Munger On MoatsSaksham SinhaОценок пока нет

- Lesson 11 (8th) National RegulationДокумент5 страницLesson 11 (8th) National Regulationsayo akandeОценок пока нет

- To Innovate or Not to Innovate: A blueprint for the law firm of the futureОт EverandTo Innovate or Not to Innovate: A blueprint for the law firm of the futureОценок пока нет

- A Perspective On InnovationДокумент16 страницA Perspective On InnovationqoriahОценок пока нет

- Comparable AcquisitionsДокумент4 страницыComparable AcquisitionsBhuwanОценок пока нет

- Pocket Book On FinanceДокумент131 страницаPocket Book On FinancerajasekharОценок пока нет

- IB Interview Guide, Module 3: Deal Discussion Example - ADT (Leveraged Buyout)Документ3 страницыIB Interview Guide, Module 3: Deal Discussion Example - ADT (Leveraged Buyout)Sofia MouraОценок пока нет

- Setting Retention Limits For LifeДокумент18 страницSetting Retention Limits For LifeIvana TodorovОценок пока нет

- Bruce Greenwald On Value Investing - US News - 11-7-2008Документ4 страницыBruce Greenwald On Value Investing - US News - 11-7-2008Luiz SobrinhoОценок пока нет

- Income Secutrities Español Clase 2Документ30 страницIncome Secutrities Español Clase 2Nacho Guzmán FaríasОценок пока нет

- Finance KeyДокумент37 страницFinance KeyTrần Lan AnhОценок пока нет

- IB Transactions Questions AnswersДокумент8 страницIB Transactions Questions Answerskirihara95Оценок пока нет

- Money Losing CompaniesДокумент4 страницыMoney Losing CompaniesBhuwanОценок пока нет

- Your Great Book Of Tax Liens And Deeds Investing - The Beginner's Real Estate Guide To Earning Sustainable Passive IncomeОт EverandYour Great Book Of Tax Liens And Deeds Investing - The Beginner's Real Estate Guide To Earning Sustainable Passive IncomeРейтинг: 5 из 5 звезд5/5 (1)

- 86 06 CapturingNewMarkets PDFДокумент11 страниц86 06 CapturingNewMarkets PDFMilton Fonseca ZuritaОценок пока нет

- Sanford C. Bernstein Strategic Decisions Conference: TranscriptДокумент12 страницSanford C. Bernstein Strategic Decisions Conference: TranscriptMark ReinhardtОценок пока нет

- Thesis On Insider TradingДокумент8 страницThesis On Insider Tradingdwns3cx2100% (2)

- Corporate governance rules and processes explainedДокумент10 страницCorporate governance rules and processes explainedBhuwan GulatiОценок пока нет

- IB Interview Guide, Module 4: Leveraged Buyouts and LBO ModelsДокумент119 страницIB Interview Guide, Module 4: Leveraged Buyouts and LBO ModelsjohnОценок пока нет

- The Tax Analects of Li Fei Lao: Navigating Taxes, Business and Life In Asia: Including Taxation for US ExpatsОт EverandThe Tax Analects of Li Fei Lao: Navigating Taxes, Business and Life In Asia: Including Taxation for US ExpatsОценок пока нет

- The State of Legal Pricing 2013 - by Toby BrownДокумент8 страницThe State of Legal Pricing 2013 - by Toby BrownRyan McCleadОценок пока нет

- Bruce Greenwald InterviewДокумент9 страницBruce Greenwald Interviewkirit0Оценок пока нет

- M&A: Concepts and Theories: New York Institute of FinanceДокумент6 страницM&A: Concepts and Theories: New York Institute of FinanceBhuwanОценок пока нет

- Startup FundingДокумент19 страницStartup FundingTheScienceOfTimeОценок пока нет

- 2012 JP Morgan Whistle Blower 3-14-2012Документ6 страниц2012 JP Morgan Whistle Blower 3-14-2012sammysmithaztОценок пока нет

- Foreign Direct Investment and Multinational Enterprises-Palgrave Macmillan (1995)Документ275 страницForeign Direct Investment and Multinational Enterprises-Palgrave Macmillan (1995)BhuwanОценок пока нет

- International Trade, Foreign Direct Investment and The Economic EnvironmentДокумент254 страницыInternational Trade, Foreign Direct Investment and The Economic EnvironmentBhuwanОценок пока нет

- Foreign Direct Investment in A Changing Global Political EconomyДокумент261 страницаForeign Direct Investment in A Changing Global Political EconomyBhuwanОценок пока нет

- The Role of Foreign Direct Investment in The Croatian EconomyДокумент58 страницThe Role of Foreign Direct Investment in The Croatian EconomyBhuwanОценок пока нет

- Foreign Direct Investment in Kazakhstan Politico-Legal Aspects of Post-Communist TransitionДокумент248 страницForeign Direct Investment in Kazakhstan Politico-Legal Aspects of Post-Communist TransitionBhuwanОценок пока нет

- Global Regulation of Foreign Direct InvestmentДокумент275 страницGlobal Regulation of Foreign Direct InvestmentBhuwanОценок пока нет

- The International Operations of National Firms - A Study of Direct Foreign Investment-MIT Press (MA) (Документ288 страницThe International Operations of National Firms - A Study of Direct Foreign Investment-MIT Press (MA) (Bhuwan100% (1)

- Foreign Direct Investment Versus Other Flows To Latin America-OECD (2001)Документ181 страницаForeign Direct Investment Versus Other Flows To Latin America-OECD (2001)BhuwanОценок пока нет

- Foreign Direct Investment in Central andДокумент352 страницыForeign Direct Investment in Central andBhuwanОценок пока нет

- Foreign Direct Investment in Central andДокумент352 страницыForeign Direct Investment in Central andBhuwanОценок пока нет

- Corporate Links and Foreign Direct Investment in Asia and The PacificДокумент319 страницCorporate Links and Foreign Direct Investment in Asia and The PacificBhuwanОценок пока нет

- The Role of Foreign Direct Investment in The Croatian EconomyДокумент58 страницThe Role of Foreign Direct Investment in The Croatian EconomyBhuwanОценок пока нет

- Dp56 Fdi in South AsiaДокумент76 страницDp56 Fdi in South AsiaDanish ZakiОценок пока нет

- A Sectoral Analysis of Foreign Direct InvestmentДокумент14 страницA Sectoral Analysis of Foreign Direct InvestmentBhuwanОценок пока нет

- Trade Facilitation in Selected Landlocked Countries in Asia (Studies in Trade and Investment) (2007)Документ160 страницTrade Facilitation in Selected Landlocked Countries in Asia (Studies in Trade and Investment) (2007)BhuwanОценок пока нет

- Foreign Investment in Nepal in The 1980s A Cost Benefit EvaluationДокумент23 страницыForeign Investment in Nepal in The 1980s A Cost Benefit EvaluationBhuwanОценок пока нет

- The Determinants of Foreign Direct Investment Flows To The Federal Region of KurdistanДокумент64 страницыThe Determinants of Foreign Direct Investment Flows To The Federal Region of KurdistanBhuwanОценок пока нет

- 1-SOAL LATIHAN Larutan Dan Sifat Fisik LarutanДокумент53 страницы1-SOAL LATIHAN Larutan Dan Sifat Fisik LarutanRicky HuОценок пока нет

- OECD Reviews On Foreign Direct Investment.Документ83 страницыOECD Reviews On Foreign Direct Investment.BhuwanОценок пока нет

- Foreign Direct Investment, Black Economic Empowerment and Labour Productivity in South AfricaДокумент37 страницForeign Direct Investment, Black Economic Empowerment and Labour Productivity in South AfricaBhuwanОценок пока нет

- Foreign Direct Investment Policy and Promotion in Latin AmericaДокумент131 страницаForeign Direct Investment Policy and Promotion in Latin AmericaBhuwanОценок пока нет

- 23457-Article Text-72575-1-10-20190403 PDFДокумент8 страниц23457-Article Text-72575-1-10-20190403 PDFSenapati Prabhupada DasОценок пока нет

- Foreign Direct Investment Policy and Promotion in Latin AmericaДокумент131 страницаForeign Direct Investment Policy and Promotion in Latin AmericaBhuwanОценок пока нет

- Foreign Investment in A Least Developed Country The Nepalese ExperienceДокумент19 страницForeign Investment in A Least Developed Country The Nepalese ExperienceBhuwanОценок пока нет

- Foreign Direct Investment and Domestic Entrepreneurship Blessing or CurseДокумент40 страницForeign Direct Investment and Domestic Entrepreneurship Blessing or CurseBhuwanОценок пока нет

- OECD Benchmark Definition of Foreign Direct Investment Third Edition-OECD Publishing (1996)Документ51 страницаOECD Benchmark Definition of Foreign Direct Investment Third Edition-OECD Publishing (1996)BhuwanОценок пока нет

- Foreign Direct Investment in Nepal A Trend AnalysisДокумент80 страницForeign Direct Investment in Nepal A Trend AnalysisBijendra Malla100% (13)

- Foreign Direct Investment in NepalДокумент15 страницForeign Direct Investment in NepalBhuwanОценок пока нет

- OECD Benchmark Definition of Foreign Direct Investment Third Edition-OECD Publishing (1996)Документ51 страницаOECD Benchmark Definition of Foreign Direct Investment Third Edition-OECD Publishing (1996)BhuwanОценок пока нет

- Human Capital Development and FDI in Developing CountriesДокумент22 страницыHuman Capital Development and FDI in Developing CountriesBhuwanОценок пока нет

- Terra Firma 2007 Annual ReviewДокумент120 страницTerra Firma 2007 Annual ReviewAsiaBuyouts100% (2)

- Investment Banking Valuation Leveraged Buyouts and Mergers and Acquisitions 2nd Edition Rosenbaum Test BankДокумент12 страницInvestment Banking Valuation Leveraged Buyouts and Mergers and Acquisitions 2nd Edition Rosenbaum Test Bankkarakulichth.yic5f100% (28)

- Sgilson@hbs - Edu: Done? Answering This Question Can Be Difficult Because The Issues Involved Are Often PoliticallyДокумент3 страницыSgilson@hbs - Edu: Done? Answering This Question Can Be Difficult Because The Issues Involved Are Often PoliticallyvicentescardosoОценок пока нет

- Acquisition and Restructuring StrategiesДокумент72 страницыAcquisition and Restructuring StrategiesMahmudur Rahman100% (2)

- InternshipsДокумент24 страницыInternshipsMohammed Zakir HussainОценок пока нет

- Merger Waves Toronto LiptonДокумент21 страницаMerger Waves Toronto LiptonVesna Simonovik PavicevicОценок пока нет

- Jazmin Medina ResumeДокумент2 страницыJazmin Medina ResumeJohn HanОценок пока нет

- Private Capital Investing - The Handbook of Private Debt and Private Equity - Roberto IppolitoДокумент319 страницPrivate Capital Investing - The Handbook of Private Debt and Private Equity - Roberto IppolitoRunyah KisauniMPCampaign67% (3)

- Asset Deals, Share Deals and Financing M&AsДокумент49 страницAsset Deals, Share Deals and Financing M&AsAnna LinОценок пока нет

- What Drives Private Equity Fund PerformanceДокумент30 страницWhat Drives Private Equity Fund PerformanceGAO KevinОценок пока нет

- Private Equity FinalДокумент13 страницPrivate Equity FinalDeepti PiplaniОценок пока нет

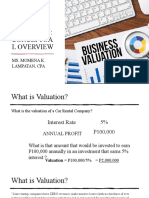

- CAR RENTAL VALUATION OVERVIEWДокумент23 страницыCAR RENTAL VALUATION OVERVIEWHazraphine Linso100% (1)

- Corporate Restructuring MCQsДокумент48 страницCorporate Restructuring MCQsJeffОценок пока нет

- Marriott Corporation Case Analysis: Project Chariot RisksДокумент6 страницMarriott Corporation Case Analysis: Project Chariot RisksChahat ShahОценок пока нет

- Kohlberg Kravis Roberts (KKR)Документ20 страницKohlberg Kravis Roberts (KKR)jim1234uОценок пока нет

- Corporate Restructuring GuideДокумент21 страницаCorporate Restructuring GuideDivyansh PareekОценок пока нет

- Public To Private Equity in The United States: A Long-Term LookДокумент82 страницыPublic To Private Equity in The United States: A Long-Term LookYog MehtaОценок пока нет

- RJR Nabisco Case - Group 4 - PPTДокумент8 страницRJR Nabisco Case - Group 4 - PPTMeghna Saluja100% (1)

- Berkshire Partners HBR CaseДокумент15 страницBerkshire Partners HBR CaseHimanshu Shekhar33% (3)

- PP CH 4 Options For Organizing BusinessДокумент33 страницыPP CH 4 Options For Organizing BusinessLenna BkОценок пока нет

- All Chapters Final2 PDFДокумент182 страницыAll Chapters Final2 PDFshiva karnatiОценок пока нет

- IBS Hyderabad : Program Course Code Course Title Faculty Name Consultation Hours (Day/time)Документ42 страницыIBS Hyderabad : Program Course Code Course Title Faculty Name Consultation Hours (Day/time)Adil D CoolestОценок пока нет

- Capital Structure Self Correction ProblemsДокумент53 страницыCapital Structure Self Correction ProblemsTamoor BaigОценок пока нет

- KKR Annual Review 2006Документ53 страницыKKR Annual Review 2006AsiaBuyoutsОценок пока нет

- Vault Guide To Private EquityДокумент336 страницVault Guide To Private Equitydosikeow50% (2)

- LboДокумент31 страницаLboAitorzinho Pepin100% (2)

- Mergers & Other Forms of Corporate RestructuringДокумент47 страницMergers & Other Forms of Corporate RestructuringNauman ChaudaryОценок пока нет

- CHAPTER - 7 Managing Growth and TransactionДокумент25 страницCHAPTER - 7 Managing Growth and TransactionTesfahun TegegnОценок пока нет

- History of Merger Waves in the USДокумент5 страницHistory of Merger Waves in the USLoan NguyễnОценок пока нет

- Six Merger Waves in The Historical MergersДокумент6 страницSix Merger Waves in The Historical MergersMei YunОценок пока нет