Вам также может понравиться

- BFM Assignment 2: Submitted By: Adhiraj Rathore E-02 20020441015Документ14 страницBFM Assignment 2: Submitted By: Adhiraj Rathore E-02 20020441015Tabrej AlamОценок пока нет

- Company Analysis of Unitech LimitedДокумент21 страницаCompany Analysis of Unitech LimitedashwiniabhaykordeОценок пока нет

- CECДокумент4 страницыCECJyoti Berwal0% (3)

- Fin402 AssignmentДокумент8 страницFin402 AssignmentAl MamunОценок пока нет

- Q1. Define Leasing Companies and How Many Companies Are Working in Pakistan?Документ7 страницQ1. Define Leasing Companies and How Many Companies Are Working in Pakistan?Rashid ShahzadОценок пока нет

- Adani Enterprises FPO Note Sushil Finance LTDДокумент3 страницыAdani Enterprises FPO Note Sushil Finance LTDsmack tripathiОценок пока нет

- IPO Note Sena Kalyan Insurance Company LimitedДокумент3 страницыIPO Note Sena Kalyan Insurance Company LimitedquickincometipsОценок пока нет

- India Consumer Fund PortfolioДокумент1 страницаIndia Consumer Fund PortfolioNitish KumarОценок пока нет

- 2010 Sept Participation Banks PresentationДокумент26 страниц2010 Sept Participation Banks PresentationisfinturkОценок пока нет

- Fin 402 DemoДокумент9 страницFin 402 DemoAl MamunОценок пока нет

- Retail Research: Changes in Shareholding in Listed Companies by MF Industry During June '16 QuarterДокумент8 страницRetail Research: Changes in Shareholding in Listed Companies by MF Industry During June '16 QuarterDinesh ChoudharyОценок пока нет

- 10 07 23 Q22010AnalystsMeetingДокумент87 страниц10 07 23 Q22010AnalystsMeetingdanimetricsОценок пока нет

- The Company: Vodafone Idea Limited Is An Indian Telecom OperatorДокумент6 страницThe Company: Vodafone Idea Limited Is An Indian Telecom OperatorSaurabh SinghОценок пока нет

- Assignment - 2: Akshita Shekhawat Division: E Roll No.: 05 PRN: 20020441032Документ15 страницAssignment - 2: Akshita Shekhawat Division: E Roll No.: 05 PRN: 20020441032Mandira PantОценок пока нет

- Fra - Project - Group No.1 - Sec BДокумент105 страницFra - Project - Group No.1 - Sec BAkshita PaulОценок пока нет

- Final Project For Marketing PuneetДокумент21 страницаFinal Project For Marketing PuneetSankalp KayathОценок пока нет

- Narendra Prajapati Bba Sem 5Документ23 страницыNarendra Prajapati Bba Sem 5Rahul Rahul AhirОценок пока нет

- Online Summer Report BBAДокумент20 страницOnline Summer Report BBARahul Rahul AhirОценок пока нет

- Fa ProjectДокумент16 страницFa Projecttapas_kbОценок пока нет

- Bank of MaharashtraДокумент5 страницBank of MaharashtraShivesh KumarОценок пока нет

- 20-Jul 15-OPT-Company Factsheet-FinalДокумент2 страницы20-Jul 15-OPT-Company Factsheet-FinalMRimauakaОценок пока нет

- Financial Aspects of Kotak Mahindra BankДокумент6 страницFinancial Aspects of Kotak Mahindra Bankajeetkumarverma 2k21dmba20Оценок пока нет

- Equity Investment Strategy: A T P: TДокумент46 страницEquity Investment Strategy: A T P: TSushilОценок пока нет

- Intimation Letter-Anchor AllocationДокумент3 страницыIntimation Letter-Anchor AllocationThe KevinОценок пока нет

- MFIN Q2 FY21 Investor PresentationДокумент74 страницыMFIN Q2 FY21 Investor PresentationANJALI MADANANОценок пока нет

- Mishkin Fmi09 PPT 20Документ56 страницMishkin Fmi09 PPT 20lashia.williams69Оценок пока нет

- ĐỊNH GIÁ SO SÁNHДокумент4 страницыĐỊNH GIÁ SO SÁNHAn HoaiОценок пока нет

- Prof. D. C. Pai: Submitted ToДокумент17 страницProf. D. C. Pai: Submitted ToGirish PalkarОценок пока нет

- Muthoot Finance LTD.: Business OverviewДокумент5 страницMuthoot Finance LTD.: Business OverviewAvinash ThakurОценок пока нет

- Amity School of Business Amity University, Noida, Uttar PradeshДокумент11 страницAmity School of Business Amity University, Noida, Uttar PradeshGautam TandonОценок пока нет

- Finance Secondary MarketДокумент12 страницFinance Secondary MarketTabrej AlamОценок пока нет

- IKE - What Is It?Документ17 страницIKE - What Is It?Tomasz SzerzadОценок пока нет

- MFIN Q2 FY20 Investor PresentationДокумент68 страницMFIN Q2 FY20 Investor PresentationNikunj AgrawallaОценок пока нет

- Submitted To: Ms Sukhwinder Kaur Submitted By: Megha Tah (T1901B46)Документ34 страницыSubmitted To: Ms Sukhwinder Kaur Submitted By: Megha Tah (T1901B46)vijaybaliyanОценок пока нет

- Bachelor Thesis: School of Advanced Education ProgramsДокумент20 страницBachelor Thesis: School of Advanced Education ProgramsĐặng Thị Tuyết MaiОценок пока нет

- Diwali Picks October - Fundamental DeskДокумент16 страницDiwali Picks October - Fundamental DeskSenthil KumarОценок пока нет

- Project 2 - Financial Leverage Case StudyДокумент9 страницProject 2 - Financial Leverage Case StudyChirag Maheshwari100% (1)

- Group9 - SecB - Dabur India LTDДокумент19 страницGroup9 - SecB - Dabur India LTDswapnil anandОценок пока нет

- EquityInvestmentStrategy 06052020 PDFДокумент41 страницаEquityInvestmentStrategy 06052020 PDFg_ayyanarОценок пока нет

- Chapter 4Документ6 страницChapter 4Seemab KanwalОценок пока нет

- Research Insight On Automotive Industry: 165 Million Tyres / Year ProductionДокумент8 страницResearch Insight On Automotive Industry: 165 Million Tyres / Year ProductionShilpi KumariОценок пока нет

- Titan CF EMBA Part 1-FinalДокумент16 страницTitan CF EMBA Part 1-FinalNagendra PattiОценок пока нет

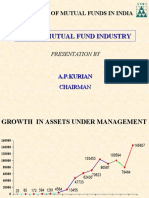

- Indian Mutual Fund IndustryДокумент25 страницIndian Mutual Fund Industryravijha_1984Оценок пока нет

- CFMitonUKSmallerCompanies FactsheetДокумент2 страницыCFMitonUKSmallerCompanies Factsheetmissteeray 1Оценок пока нет

- Irp Adani FinalДокумент4 страницыIrp Adani Finalharsh kaushikОценок пока нет

- JSTREET Volume 351Документ10 страницJSTREET Volume 351JhaveritradeОценок пока нет

- What's in What's Out AMC Holdings: Mutual FundsДокумент292 страницыWhat's in What's Out AMC Holdings: Mutual FundsRudra GoudОценок пока нет

- 2019 11 20 PH D PDFДокумент5 страниц2019 11 20 PH D PDFJОценок пока нет

- LKP Moldtek 01feb08Документ2 страницыLKP Moldtek 01feb08nillchopraОценок пока нет

- Mba-Ii Section - A Week 4 Report: Annaam Bin Muhammad Haris Amir Hira Naeem Muggo Kinza AdnanДокумент10 страницMba-Ii Section - A Week 4 Report: Annaam Bin Muhammad Haris Amir Hira Naeem Muggo Kinza AdnanHaris AmirОценок пока нет

- Presentation To Analysts: June 2016 (In INR)Документ39 страницPresentation To Analysts: June 2016 (In INR)anasОценок пока нет

- Bharti Airtel Annual Report 2009 10Документ172 страницыBharti Airtel Annual Report 2009 10narin_19910% (1)

- Top 17 Stocks BuyДокумент13 страницTop 17 Stocks BuySushilОценок пока нет

- WEL COM EYO U in TH IS PRE SEN Tati ONДокумент19 страницWEL COM EYO U in TH IS PRE SEN Tati ONhaseeb zainОценок пока нет

- Report On Financial Analysis of National Buildings Construction Corporation Ltd. (NBCC) .Документ19 страницReport On Financial Analysis of National Buildings Construction Corporation Ltd. (NBCC) .arnabgogoiОценок пока нет

- Report On Demerger - Tube Investment India LimitedДокумент8 страницReport On Demerger - Tube Investment India LimitedMithil DoshiОценок пока нет

- Reforms, Opportunities, and Challenges for State-Owned EnterprisesОт EverandReforms, Opportunities, and Challenges for State-Owned EnterprisesОценок пока нет

- A Comprehensive Project On: Consumers Perception Towards Titan Watches in Vadodara CityДокумент10 страницA Comprehensive Project On: Consumers Perception Towards Titan Watches in Vadodara Citykruti makvanaОценок пока нет

- Titan Company Industrial VisitДокумент18 страницTitan Company Industrial VisitVedant PawarОценок пока нет

- Linear Arrangement - 2Документ2 страницыLinear Arrangement - 2Hritik RawatОценок пока нет

- Project On TitanДокумент74 страницыProject On TitanMona Vyas0% (1)

- Citizen - FinalДокумент54 страницыCitizen - FinalReshma DhulapОценок пока нет

- Brand Impact TitanДокумент57 страницBrand Impact TitanMukesh ManwaniОценок пока нет

- TATA CSR AssignmentДокумент22 страницыTATA CSR AssignmentNISHANT SINGHОценок пока нет

- Tanishq Case StudyДокумент17 страницTanishq Case StudyasniОценок пока нет

- A Titan Industries Programme To Improve The Livelihood of Women Through Micro-Business and EducationДокумент2 страницыA Titan Industries Programme To Improve The Livelihood of Women Through Micro-Business and EducationNirmala VrОценок пока нет

- Q4FY23 Financial ResultsДокумент21 страницаQ4FY23 Financial ResultsRiya ThakurОценок пока нет

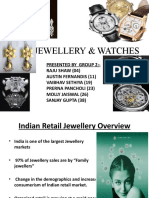

- JewelleryДокумент35 страницJewelleryoviyadsgОценок пока нет

- On Titan CompanyДокумент14 страницOn Titan CompanyAkriti JhaОценок пока нет

- Service Quality and CS of TanishqДокумент42 страницыService Quality and CS of TanishqVaishnavi PatelОценок пока нет

- Titan PPT On Consumer BehaviourДокумент32 страницыTitan PPT On Consumer Behaviourpramod_384871% (7)

- TANISHQ - Group 1 Corporate Communication M5th BatchДокумент26 страницTANISHQ - Group 1 Corporate Communication M5th BatchMausam SharmaОценок пока нет

- Titan Case StudyДокумент19 страницTitan Case StudyRohitSharmaОценок пока нет

- Fastrack Complete ResearchДокумент16 страницFastrack Complete ResearchAkhilesh Anjan50% (2)

- Segmentation of Indian ConsumerДокумент16 страницSegmentation of Indian Consumerdeepak asnora0% (1)

- Evaluating Quality Performance of The Titan Company: (Economics-Micro)Документ39 страницEvaluating Quality Performance of The Titan Company: (Economics-Micro)Hamza AjmeriОценок пока нет

- Fast TrackДокумент84 страницыFast TrackAnwar MohdОценок пока нет

- Day - 5 English 165717371117Документ55 страницDay - 5 English 165717371117canasОценок пока нет

- Final DocumentДокумент13 страницFinal DocumentMANASA SARVASETTYОценок пока нет

- Brand Study Advertising Plan For Titan Watches PDFДокумент43 страницыBrand Study Advertising Plan For Titan Watches PDFfftddfdsdОценок пока нет

- Indian Wrist Watch Industry - Marketing Mix of The Leading PlayersДокумент8 страницIndian Wrist Watch Industry - Marketing Mix of The Leading Playersvismay_soodОценок пока нет

- CASE STUDY - Titan Industries LTD PDFДокумент2 страницыCASE STUDY - Titan Industries LTD PDFSaurabh SethОценок пока нет

- Group 3 - Case Analysis - TitanДокумент3 страницыGroup 3 - Case Analysis - TitanRini RafiОценок пока нет

- TitanДокумент42 страницыTitanAnil NandyalaОценок пока нет

- Nisha Pandey PDF 1Документ71 страницаNisha Pandey PDF 1Ajay ThakurОценок пока нет

- Growth of Luxury Market Products in IndiaДокумент61 страницаGrowth of Luxury Market Products in IndiaSwarnim DobwalОценок пока нет

- TANISHQДокумент9 страницTANISHQkishayОценок пока нет