Вам также может понравиться

- IMF (FinTech Notes) Blockchain Consensus Mechanisms - A Primer For SupervisorsДокумент18 страницIMF (FinTech Notes) Blockchain Consensus Mechanisms - A Primer For SupervisorsMuning AnОценок пока нет

- Digitalisation of Payment Services-ZunzuneguiДокумент30 страницDigitalisation of Payment Services-Zunzuneguihotbackup2018Оценок пока нет

- Clear 2 PayДокумент2 страницыClear 2 PayJyoti KumarОценок пока нет

- Global ATM Market Report: 2013 Edition - Koncept AnalyticsДокумент11 страницGlobal ATM Market Report: 2013 Edition - Koncept AnalyticsKoncept AnalyticsОценок пока нет

- 2017 McKinsey Payments Report PDFДокумент16 страниц2017 McKinsey Payments Report PDFnihar shethОценок пока нет

- Akanksha Gupta - XML Interface For NEFTДокумент17 страницAkanksha Gupta - XML Interface For NEFTatularvin23184Оценок пока нет

- IBM Banking: Our Payments Framework Solution For Financial Services Helps Simplify Payments OperationsДокумент4 страницыIBM Banking: Our Payments Framework Solution For Financial Services Helps Simplify Payments OperationsIBMBankingОценок пока нет

- Cashless+Mobile PaymentsДокумент21 страницаCashless+Mobile PaymentsAnkit SajayaОценок пока нет

- BASE24 DR With AutoTMF and RDF WhitepaperДокумент38 страницBASE24 DR With AutoTMF and RDF WhitepaperMohan RajОценок пока нет

- POS DynmCurrConvДокумент58 страницPOS DynmCurrConvPaulo LewisОценок пока нет

- Pssbooklet PDFДокумент142 страницыPssbooklet PDFForkLogОценок пока нет

- RRBs IN AEPSДокумент20 страницRRBs IN AEPSKáúśtúbhÇóólОценок пока нет

- Cisp What To Do If CompromisedДокумент60 страницCisp What To Do If CompromisedkcchenОценок пока нет

- SOP BC Interoperability - Interface SpecificationsДокумент90 страницSOP BC Interoperability - Interface SpecificationsutnfrbaОценок пока нет

- ArticleforPaymentsSystemsMagazine-13 11 05Документ14 страницArticleforPaymentsSystemsMagazine-13 11 05Syed RazviОценок пока нет

- Coding Rules: Section A: Linux Kernel Style Based Coding For C ProgramsДокумент8 страницCoding Rules: Section A: Linux Kernel Style Based Coding For C ProgramsAyonyaPrabhakaranОценок пока нет

- Guide To Payment Services in SLДокумент86 страницGuide To Payment Services in SLTharuka WijesingheОценок пока нет

- UPI QR Code AcceptanceДокумент22 страницыUPI QR Code AcceptanceIssaОценок пока нет

- J-Secure 2.0 Acquirer Implementation Guide - v1.2Документ32 страницыJ-Secure 2.0 Acquirer Implementation Guide - v1.2mitxael83Оценок пока нет

- Bank Portfolio ManagementДокумент6 страницBank Portfolio ManagementAbhay VelayudhanОценок пока нет

- Unisys + C2P OPFДокумент4 страницыUnisys + C2P OPFdebajyotiguhaОценок пока нет

- Packetlogic 21 62 00 Virtual KVM Platform GuideДокумент49 страницPacketlogic 21 62 00 Virtual KVM Platform GuideTrkОценок пока нет

- Aci PRM Enterprise RiskДокумент23 страницыAci PRM Enterprise RiskRajesh VasudevanОценок пока нет

- Aeps XML H-H Specification Version 1.2Документ23 страницыAeps XML H-H Specification Version 1.2Krishna TelgaveОценок пока нет

- Standard Chartered BankДокумент28 страницStandard Chartered BankRajni YadavОценок пока нет

- SWIFT messaging network enables global bank fund transfers & paymentsДокумент2 страницыSWIFT messaging network enables global bank fund transfers & paymentsDeen Mohammed ProtikОценок пока нет

- Proje QT orДокумент213 страницProje QT orEleazar BrionesОценок пока нет

- Agent Banking in Mobile Applicationv.4 - WithcommentsДокумент25 страницAgent Banking in Mobile Applicationv.4 - WithcommentsCielo CuisiaОценок пока нет

- Swift Whitepaper Supply Chain Finance 201304Документ8 страницSwift Whitepaper Supply Chain Finance 201304Rami Al-SabriОценок пока нет

- AN2949Документ7 страницAN2949archiealfitrosdОценок пока нет

- MC - InterchangeManualMEACustomer (1) 2Документ2 031 страницаMC - InterchangeManualMEACustomer (1) 2hanane eddahoumiОценок пока нет

- E-Banking: by Gaurav SinghДокумент23 страницыE-Banking: by Gaurav SinghDeepak SharmaОценок пока нет

- EPIS Merchant AcquiringДокумент3 страницыEPIS Merchant AcquiringyadbhavishyaОценок пока нет

- Operational Guidelines For Open Banking in NigeriaДокумент68 страницOperational Guidelines For Open Banking in NigeriaCYNTHIA Jumoke100% (1)

- Under The Guidance Of: A Summer Training Report ONДокумент50 страницUnder The Guidance Of: A Summer Training Report ONAnil BatraОценок пока нет

- Guidelines On Operations of Electronic Payment Channels in GhanaДокумент33 страницыGuidelines On Operations of Electronic Payment Channels in GhanashanrimazОценок пока нет

- Distributed ledgers transform paymentsДокумент14 страницDistributed ledgers transform paymentsYitian LiОценок пока нет

- A Research Paper On RBI Branch Licensing Policy: "Branching" The Gap Between FinancialДокумент13 страницA Research Paper On RBI Branch Licensing Policy: "Branching" The Gap Between Financialgayatrimohanty05Оценок пока нет

- Generation Gap!!: Presented by Group 1 Minu, Krithika, Rahul, Suraj & AjithДокумент21 страницаGeneration Gap!!: Presented by Group 1 Minu, Krithika, Rahul, Suraj & Ajithm_dattaias100% (2)

- Customer Information File User Manual PDFДокумент314 страницCustomer Information File User Manual PDFFahim KaziОценок пока нет

- Dovetail Research - 2016 Value of InstantДокумент19 страницDovetail Research - 2016 Value of InstantHitesh ThakkarОценок пока нет

- Hyperledger Besu: An Overview of Features and Use CasesДокумент19 страницHyperledger Besu: An Overview of Features and Use CasesPatricio Ibarra GuzmánОценок пока нет

- If SwitchДокумент51 страницаIf Switchxfirelove12Оценок пока нет

- Standard Chartered Bank ATM FlowДокумент11 страницStandard Chartered Bank ATM FlowJayavant MaliОценок пока нет

- PayflowGateway GuideДокумент238 страницPayflowGateway Guiderobert2370Оценок пока нет

- Electronic Delivery of Financial ServicesДокумент19 страницElectronic Delivery of Financial ServicesShailesh ShettyОценок пока нет

- Cards and Payment Industry in Vietnam 2013Документ23 страницыCards and Payment Industry in Vietnam 2013alcy2793100% (2)

- Banking Enquiry: Payment Cards and Interchange Fee HearingsДокумент18 страницBanking Enquiry: Payment Cards and Interchange Fee HearingssanjayjogsОценок пока нет

- 3.11 Changes To Visa Settlement Service Reporting For Load and Reload TransactionsДокумент15 страниц3.11 Changes To Visa Settlement Service Reporting For Load and Reload TransactionsYasir RoniОценок пока нет

- Jcard Internals PDFДокумент27 страницJcard Internals PDFAshu ChaudharyОценок пока нет

- VisaДокумент16 страницVisaMasud RanaОценок пока нет

- Payments Hub Redefining Payments InfrastructureДокумент10 страницPayments Hub Redefining Payments InfrastructureRishi SrivastavaОценок пока нет

- ISO 20022 and the Evolution of Standards in European Card PaymentsДокумент20 страницISO 20022 and the Evolution of Standards in European Card PaymentsLuis F JaureguiОценок пока нет

- Tax Challenges Digitalisation Part 1 Comments On Request For Input 2017Документ180 страницTax Challenges Digitalisation Part 1 Comments On Request For Input 2017Rajeev ShuklaОценок пока нет

- RTGS, A Payment SystemДокумент7 страницRTGS, A Payment SystemShrishailamalikarjunОценок пока нет

- Chapter 1 - Introduction To Digital Banking - V1.0Документ17 страницChapter 1 - Introduction To Digital Banking - V1.0prabhjinderОценок пока нет

- Distribution Channels For Travel and TourismДокумент13 страницDistribution Channels For Travel and TourismAliОценок пока нет

- Emergence of Payment Systems in the Digital AgeДокумент6 страницEmergence of Payment Systems in the Digital AgeThulhaj ParveenОценок пока нет

- KYC Policy-Internet Version-Updated Upto 10.05.2021-CompressedДокумент73 страницыKYC Policy-Internet Version-Updated Upto 10.05.2021-CompressedAmaanОценок пока нет

- United States District Court Southern District of New York United States of America - v. - James Zhong, Defendant. 22 Cr. 606 (PGG)Документ37 страницUnited States District Court Southern District of New York United States of America - v. - James Zhong, Defendant. 22 Cr. 606 (PGG)ForkLogОценок пока нет

- ATMДокумент71 страницаATMForkLogОценок пока нет

- Daaml Act of 2022Документ7 страницDaaml Act of 2022ForkLogОценок пока нет

- VoyagerДокумент13 страницVoyagerForkLogОценок пока нет

- United States Securities and Exchange Commission Schedule 14AДокумент239 страницUnited States Securities and Exchange Commission Schedule 14AForkLogОценок пока нет

- Daaml Act of 2022Документ7 страницDaaml Act of 2022ForkLogОценок пока нет

- Daaml Act of 2022Документ7 страницDaaml Act of 2022ForkLogОценок пока нет

- The Cosmos HubДокумент27 страницThe Cosmos HubForkLogОценок пока нет

- COM 2022 552 1 EN ACT Part1 v6Документ23 страницыCOM 2022 552 1 EN ACT Part1 v6ForkLogОценок пока нет

- Commission Sets Out Actions To Digitalise The Energy Sector To Improve Efficiency and Renewables IntegrationДокумент2 страницыCommission Sets Out Actions To Digitalise The Energy Sector To Improve Efficiency and Renewables IntegrationForkLogОценок пока нет

- TexasДокумент11 страницTexasForkLogОценок пока нет

- LawsuitДокумент16 страницLawsuitForkLogОценок пока нет

- U S D C: Nited Tates Istrict OurtДокумент1 страницаU S D C: Nited Tates Istrict OurtForkLogОценок пока нет

- United States District Court Eastern District of Kentucky Lexington DivisionДокумент71 страницаUnited States District Court Eastern District of Kentucky Lexington DivisionForkLogОценок пока нет

- In Re Celsius Network LLCДокумент20 страницIn Re Celsius Network LLCForkLogОценок пока нет

- Updated Guidance VA VASPДокумент111 страницUpdated Guidance VA VASPForkLogОценок пока нет

- Terra LawsuitДокумент72 страницыTerra LawsuitForkLogОценок пока нет

- Economic Well-Being of U.S. Households in 2021: Research & AnalysisДокумент98 страницEconomic Well-Being of U.S. Households in 2021: Research & AnalysisForkLogОценок пока нет

- MHH 026 XML SignedДокумент7 страницMHH 026 XML SignedForkLogОценок пока нет

- Treasury Letter On Broker DefinitionДокумент3 страницыTreasury Letter On Broker DefinitionForkLogОценок пока нет

- United States Strategy On Countering CorruptionДокумент38 страницUnited States Strategy On Countering CorruptionForkLogОценок пока нет

- A Bill: 117 Congress 2 SДокумент9 страницA Bill: 117 Congress 2 SForkLogОценок пока нет

- Pub Semiannual Risk Perspective Fall 2021Документ32 страницыPub Semiannual Risk Perspective Fall 2021ForkLogОценок пока нет

- 34 93489Документ3 страницы34 93489ForkLogОценок пока нет

- Compensation Framework Review: Discussion PaperДокумент48 страницCompensation Framework Review: Discussion PaperForkLogОценок пока нет

- TSLA Q3 2021 Quarterly UpdateДокумент27 страницTSLA Q3 2021 Quarterly UpdateFred LamertОценок пока нет

- Yellen Responses To Toomey QfrsДокумент8 страницYellen Responses To Toomey QfrsForkLogОценок пока нет

- Financial Trend Analysis - Ransomware 508 FINALДокумент17 страницFinancial Trend Analysis - Ransomware 508 FINALForkLogОценок пока нет

- Tesla, Inc.: United States Securities and Exchange Commission FORM 10-QДокумент66 страницTesla, Inc.: United States Securities and Exchange Commission FORM 10-QForkLogОценок пока нет

- G7 Public Policy Principles For Retail CBDC FINALДокумент27 страницG7 Public Policy Principles For Retail CBDC FINALForkLogОценок пока нет

- Accounts Receivables OracleДокумент76 страницAccounts Receivables OracleDhananjay KasthuriОценок пока нет

- Statement of Account: Date Particulars CHQ - No. Withdrawals Deposits BalanceДокумент3 страницыStatement of Account: Date Particulars CHQ - No. Withdrawals Deposits BalanceDeepak Raj KumarОценок пока нет

- Extra-Week 10 IMF and International Monetary SystemДокумент25 страницExtra-Week 10 IMF and International Monetary SystemOv NomaanОценок пока нет

- Ratio Analysis of Bank of BarodaДокумент14 страницRatio Analysis of Bank of BarodaSimran MehrotraОценок пока нет

- Euroization of The Albanian Economy An Alternative To Be ConsideredДокумент42 страницыEuroization of The Albanian Economy An Alternative To Be ConsideredDesada LleshanakuОценок пока нет

- Icici Partnership ModelДокумент11 страницIcici Partnership ModelMit SinhaОценок пока нет

- Challan FormДокумент1 страницаChallan Formishaq0786Оценок пока нет

- Prudential Norms On Income Recognition, Asset ClassificationДокумент13 страницPrudential Norms On Income Recognition, Asset Classificationyogesh wadikhayeОценок пока нет

- Syllabus of CDCSДокумент4 страницыSyllabus of CDCSShawn Barnes100% (4)

- Vsla Financial and Monitoring Reporting Tool For December (Mikuini)Документ2 страницыVsla Financial and Monitoring Reporting Tool For December (Mikuini)Christopher Subano100% (2)

- Document PDFДокумент7 страницDocument PDFPeña MotorОценок пока нет

- Mohammadpur Model School & College Mohammadpur Model School & College Mohammadpur Model School & CollegeДокумент1 страницаMohammadpur Model School & College Mohammadpur Model School & College Mohammadpur Model School & CollegeSahadot Hasan EthonОценок пока нет

- Metlife Meeting 20130819Документ16 страницMetlife Meeting 20130819Ta NyaОценок пока нет

- Varanasi - Sugam Darshan - 1121232Документ1 страницаVaranasi - Sugam Darshan - 1121232raj1602Оценок пока нет

- Bank of Baroda HomeloanДокумент63 страницыBank of Baroda HomeloansantoshОценок пока нет

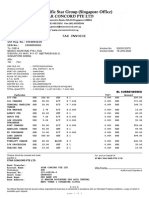

- Invoice SII22012979Документ2 страницыInvoice SII22012979Summersky9333Оценок пока нет

- Enquiry Regarding Token Numbers of Outstanding Pre-Check BillsДокумент3 страницыEnquiry Regarding Token Numbers of Outstanding Pre-Check BillsARAVIND K100% (1)

- Stanbic Mini Diclosure Tarrif GuideДокумент2 страницыStanbic Mini Diclosure Tarrif GuideOMARYОценок пока нет

- Types in BankingДокумент17 страницTypes in Bankingdevendrachoudhary_upscОценок пока нет

- Ops Converted - R - 2021Документ323 страницыOps Converted - R - 2021knowledge musendekwaОценок пока нет

- India's Central Bank Reserve Bank of India Regional Office, Delhi, Foreign Remittance Department. New Delhi: 110 001, India, 6, Sansad MargДокумент2 страницыIndia's Central Bank Reserve Bank of India Regional Office, Delhi, Foreign Remittance Department. New Delhi: 110 001, India, 6, Sansad MargvnkatОценок пока нет

- Hc-Si22120057 Db-JeelytonДокумент1 страницаHc-Si22120057 Db-JeelytonHanh Nguyen KhacОценок пока нет

- Foreclosure Actions and Cases Lawfully Dismissed (Not Letting Bank Foreclose Without Lawful Validation and Production)Документ25 страницForeclosure Actions and Cases Lawfully Dismissed (Not Letting Bank Foreclose Without Lawful Validation and Production)PhilОценок пока нет

- Desember 2022Документ2 страницыDesember 2022Vieny AyuznaОценок пока нет

- Nonstate Institutions-Banks and CorporationsДокумент20 страницNonstate Institutions-Banks and CorporationsEisenhower SabaОценок пока нет

- Fee Information Document: General Account ServicesДокумент7 страницFee Information Document: General Account Servicesdaryl30011996Оценок пока нет

- Composition of cash and petty cash fundsДокумент7 страницComposition of cash and petty cash fundsRyou ShinodaОценок пока нет

- Template - Branch Enrollment Form v2Документ6 страницTemplate - Branch Enrollment Form v2Enrry SebastianОценок пока нет

- LC PresentationДокумент20 страницLC Presentationnarasimhan_caОценок пока нет

- Investors FormДокумент1 страницаInvestors FormJustus CyrilОценок пока нет