Вам также может понравиться

- Areas Off-Limits To Mining (NTDP - List of Cluster Destinations and TDAs)Документ3 страницыAreas Off-Limits To Mining (NTDP - List of Cluster Destinations and TDAs)akosistellaОценок пока нет

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Academy of Television Arts & Sciences 64th Primetime Emmy Award NominationsДокумент64 страницыAcademy of Television Arts & Sciences 64th Primetime Emmy Award NominationsakosistellaОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Letter of Narzalina Lim To DOT U/Sec. Daniel CorpuzДокумент2 страницыLetter of Narzalina Lim To DOT U/Sec. Daniel CorpuzakosistellaОценок пока нет

- Muntinlupa City Council Overrules Ayala Alabang Ordinance On CondomsДокумент2 страницыMuntinlupa City Council Overrules Ayala Alabang Ordinance On CondomsakosistellaОценок пока нет

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- ST James The Great Parish's Statement On Brgy. Ayala Alabang's Ordinance Vs CondomsДокумент1 страницаST James The Great Parish's Statement On Brgy. Ayala Alabang's Ordinance Vs CondomsakosistellaОценок пока нет

- Anyone For Filipino Food? (Tom Parker Bowles, Esquire Aug. 2011)Документ9 страницAnyone For Filipino Food? (Tom Parker Bowles, Esquire Aug. 2011)akosistellaОценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Brgy. Ayala Alabang's Ordinance No. 01 (Series of 2011) Banning Sale of ContraceptivesДокумент9 страницBrgy. Ayala Alabang's Ordinance No. 01 (Series of 2011) Banning Sale of ContraceptivesakosistellaОценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- What Went On in The Making of 'Pilipinas Kay Ganda'Документ9 страницWhat Went On in The Making of 'Pilipinas Kay Ganda'akosistellaОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- SC Ruling Vizconde Massacre (G.R. No. 176389) 12/14/2010Документ36 страницSC Ruling Vizconde Massacre (G.R. No. 176389) 12/14/2010akosistellaОценок пока нет

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Interpol Alert AssangeДокумент3 страницыInterpol Alert AssangeakosistellaОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

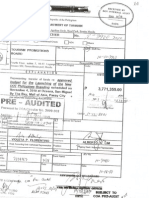

- 'Pilipinas Kay Ganda' Disbursement VoucherДокумент6 страниц'Pilipinas Kay Ganda' Disbursement VoucherakosistellaОценок пока нет

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Top 500 Individual and Corp. Taxpayers 2009Документ18 страницTop 500 Individual and Corp. Taxpayers 2009akosistellaОценок пока нет

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- PAL Salary, Benefits of Cabin CrewДокумент1 страницаPAL Salary, Benefits of Cabin CrewakosistellaОценок пока нет

- Memorandum Circular No. 1Документ2 страницыMemorandum Circular No. 1Coolbuster.NetОценок пока нет

- Charman's Report On Automated Elections (Complete Document)Документ47 страницCharman's Report On Automated Elections (Complete Document)akosistellaОценок пока нет

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Observations, Conclusions and RecommendationsДокумент7 страницObservations, Conclusions and RecommendationsakosistellaОценок пока нет

- On Types of BanksДокумент14 страницOn Types of BanksRahulTikoo100% (1)

- Quaid e Azam Solar ParkДокумент8 страницQuaid e Azam Solar ParkShahzad TabassumОценок пока нет

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Borden Knight Trading Columbia SeminarДокумент16 страницBorden Knight Trading Columbia Seminarpurumi77Оценок пока нет

- ©2011 Pearson Education, Inc. Publishing As Prentice HallДокумент72 страницы©2011 Pearson Education, Inc. Publishing As Prentice HallSimon SebastianОценок пока нет

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- SBI Project ReportДокумент14 страницSBI Project ReportNick IvanОценок пока нет

- CH 08Документ54 страницыCH 08Chang Chan ChongОценок пока нет

- Public Procurement Regulatory Authority (PPRA)Документ14 страницPublic Procurement Regulatory Authority (PPRA)Salu Shigri100% (1)

- Spectra Foods & Beverages PVT LTD 2006 29697Документ10 страницSpectra Foods & Beverages PVT LTD 2006 29697Bhavana PrettyОценок пока нет

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- DRM-5 Options BasicsДокумент22 страницыDRM-5 Options BasicsqazxswОценок пока нет

- Direct Tax Article Taxation of Agricultural LandДокумент7 страницDirect Tax Article Taxation of Agricultural LandmanishdgОценок пока нет

- Arpita MAJOR RESEARCH PROJECTДокумент31 страницаArpita MAJOR RESEARCH PROJECTSukhvinder SinghОценок пока нет

- Understanding Investment ObjectivesДокумент5 страницUnderstanding Investment ObjectivesDas RandhirОценок пока нет

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- How Mintoff Killed The NBMДокумент4 страницыHow Mintoff Killed The NBMsevee2081Оценок пока нет

- Materi 3 Materi 3 Rerangka Konseptual IASBДокумент20 страницMateri 3 Materi 3 Rerangka Konseptual IASBgadi3szzОценок пока нет

- Asset and Liability Management ModelДокумент32 страницыAsset and Liability Management ModelSuccess BnОценок пока нет

- Sample QCD With Life EstateДокумент2 страницыSample QCD With Life Estatemarioma12Оценок пока нет

- Johnson Elevator Case StudyДокумент5 страницJohnson Elevator Case StudyPJОценок пока нет

- Ebook How To Become The FTMO Trader PDFДокумент28 страницEbook How To Become The FTMO Trader PDFJohn KaraОценок пока нет

- Project Financing StructuresДокумент17 страницProject Financing StructuresarjunpguptaОценок пока нет

- BIR Form 1700 - Income Tax Return FilingДокумент1 страницаBIR Form 1700 - Income Tax Return FilingMarriz Bustaliño TanОценок пока нет

- Investments in Financial Instruments CompleteДокумент34 страницыInvestments in Financial Instruments CompleteDenise CruzОценок пока нет

- Financial ServicesДокумент12 страницFinancial ServicesarmailgmОценок пока нет

- Compound InterestДокумент16 страницCompound InterestJin ChorОценок пока нет

- Financial Inclusion and Information TechnologyДокумент8 страницFinancial Inclusion and Information TechnologydhawanmayurОценок пока нет

- Equity Derivatives NCFM Ver 1.5Документ148 страницEquity Derivatives NCFM Ver 1.5sanky23Оценок пока нет

- Accounting Standard 1 PDFДокумент4 страницыAccounting Standard 1 PDFChristopher Jacob MurmuОценок пока нет

- 10.1016@S2212 56711300194 9 PDFДокумент5 страниц10.1016@S2212 56711300194 9 PDFsajid bhattiОценок пока нет

- Tax Revenue Performance in KenyaДокумент47 страницTax Revenue Performance in KenyaMwangi MburuОценок пока нет

- Best Practice in Inventory Management Oliver Wight Manufacturing PDFДокумент234 страницыBest Practice in Inventory Management Oliver Wight Manufacturing PDFantehen100% (3)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorОт EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorРейтинг: 4.5 из 5 звезд4.5/5 (132)