Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiДокумент71 страницаTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiДокумент71 страницаTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- US Internal Revenue Service: 2290rulesty2007v4 0Документ6 страницUS Internal Revenue Service: 2290rulesty2007v4 0IRSОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Objectives Report To Congress v2Документ153 страницы2008 Objectives Report To Congress v2IRSОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiДокумент71 страницаTratamentul Total Al CanceruluiAntal98% (98)

- 2008 Credit Card Bulk Provider RequirementsДокумент112 страниц2008 Credit Card Bulk Provider RequirementsIRSОценок пока нет

- 2008 Data DictionaryДокумент260 страниц2008 Data DictionaryIRSОценок пока нет

- Tratamentul Total Al CanceruluiДокумент71 страницаTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiДокумент71 страницаTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (120)

- Toppan Merrill Technology ListДокумент2 страницыToppan Merrill Technology ListKilty ONealОценок пока нет

- This Study Resource WasДокумент2 страницыThis Study Resource WasAron Rabino ManaloОценок пока нет

- CH 05Документ37 страницCH 05Janna KarapetyanОценок пока нет

- Sample Business Impact AssessmentДокумент2 страницыSample Business Impact AssessmentbdfbgrdfbbuiwefОценок пока нет

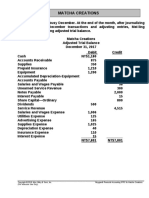

- MC4 Matcha Creations: (For Instructor Use Only)Документ2 страницыMC4 Matcha Creations: (For Instructor Use Only)Reza eka PutraОценок пока нет

- Oilsafe Identification LabelsДокумент12 страницOilsafe Identification LabelsHesham MahdyОценок пока нет

- Understanding The Leadership Spectrum - Developing The SkillsДокумент46 страницUnderstanding The Leadership Spectrum - Developing The SkillsSam PoliasОценок пока нет

- Problems On Ages Questions Specially For Sbi Po PrelimsДокумент18 страницProblems On Ages Questions Specially For Sbi Po Prelimsabinusundaram0Оценок пока нет

- Business Interruption Insurance Notes-Final 2023Документ12 страницBusiness Interruption Insurance Notes-Final 2023tshililo mbengeniОценок пока нет

- FLIPKART Research ReportДокумент18 страницFLIPKART Research ReportHabib RahmanОценок пока нет

- Kosovo Subject Area Code Final For Public Discussion 3Документ17 страницKosovo Subject Area Code Final For Public Discussion 3alban maliqiОценок пока нет

- Uhura Company Has Decided To Expand Its Operations The BookkeepДокумент1 страницаUhura Company Has Decided To Expand Its Operations The BookkeepM Bilal SaleemОценок пока нет

- Fundamental Analysis of StocksДокумент34 страницыFundamental Analysis of StocksPrajwal nayakОценок пока нет

- The Rise of NFT FundraisingДокумент36 страницThe Rise of NFT FundraisingTrader CatОценок пока нет

- 19 07 31 DCDC Cred HandbookДокумент24 страницы19 07 31 DCDC Cred HandbookJAIME CHAVEZОценок пока нет

- Module 3Документ79 страницModule 3kakimog738Оценок пока нет

- Letter Request Waiver On Penalty InterestДокумент2 страницыLetter Request Waiver On Penalty InterestHayati Ahmad56% (18)

- QUIZ1Документ1 страницаQUIZ1Janysse CalderonОценок пока нет

- 5.tender Process N DocumentationДокумент35 страниц5.tender Process N DocumentationDilanka MJ Dassanayake100% (1)

- IHG® Frontline - GM Implementation Guide (Americas)Документ20 страницIHG® Frontline - GM Implementation Guide (Americas)Julie AnnaОценок пока нет

- Manila City - Ordinance No. 8330 s.2013Документ5 страницManila City - Ordinance No. 8330 s.2013Franco SenaОценок пока нет

- Wiley CFA Test Bank 180527 (20 Preguntas)Документ12 страницWiley CFA Test Bank 180527 (20 Preguntas)rafav10Оценок пока нет

- Tenant Verification Form PDFДокумент2 страницыTenant Verification Form PDFmohit kumarОценок пока нет

- Role of Artificial Intelligence in Banking SectorДокумент45 страницRole of Artificial Intelligence in Banking Sectorsamyak gangwal86% (7)

- Research Methods For Architecture Ebook - Lucas, Ray - Kindle StoreДокумент1 страницаResearch Methods For Architecture Ebook - Lucas, Ray - Kindle StoreMohammed ShriamОценок пока нет

- Actividad 19 Evidencia 7 Taller "Talking About Logistics, Workshop"Документ5 страницActividad 19 Evidencia 7 Taller "Talking About Logistics, Workshop"claudia gomezОценок пока нет

- Loreto School FeesДокумент4 страницыLoreto School FeesLaltu KarmakarОценок пока нет

- Great To Have You On Board!Документ36 страницGreat To Have You On Board!jondraxdОценок пока нет

- MicroeconomicsДокумент40 страницMicroeconomicsananyadadhwal13Оценок пока нет

- Assistant AccountantДокумент4 страницыAssistant AccountantfahadОценок пока нет