Вам также может понравиться

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiДокумент71 страницаTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Data DictionaryДокумент260 страниц2008 Data DictionaryIRSОценок пока нет

- US Internal Revenue Service: 2290rulesty2007v4 0Документ6 страницUS Internal Revenue Service: 2290rulesty2007v4 0IRSОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Credit Card Bulk Provider RequirementsДокумент112 страниц2008 Credit Card Bulk Provider RequirementsIRSОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Objectives Report To Congress v2Документ153 страницы2008 Objectives Report To Congress v2IRSОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Chapter 5 - TBTДокумент8 страницChapter 5 - TBTKatKat Olarte100% (2)

- f1040s8 2021Документ3 страницыf1040s8 2021さくら樱花Оценок пока нет

- Bir Ruling (Da 533 07)Документ2 страницыBir Ruling (Da 533 07)Jeffrey JosolОценок пока нет

- Sales Quotation - 221692 - 20230110 - 165855Документ1 страницаSales Quotation - 221692 - 20230110 - 165855Mukesh Krishna VeniОценок пока нет

- The Archewell Foundation 2022 Public DisclosureДокумент47 страницThe Archewell Foundation 2022 Public DisclosureJustin VallejoОценок пока нет

- Marubeni Corp. vs. CIR, G.R. No. 76573, March 7, 1990Документ1 страницаMarubeni Corp. vs. CIR, G.R. No. 76573, March 7, 1990Jacinto Jr Jamero0% (1)

- 1 Disposition of ProceedsДокумент8 страниц1 Disposition of ProceedsFrancis LОценок пока нет

- Amol Srivastava April Income TaxДокумент1 страницаAmol Srivastava April Income TaxRemruata FanaiОценок пока нет

- GST ChallanДокумент1 страницаGST ChallanWilfred DsouzaОценок пока нет

- 3 Collector V de LaraДокумент5 страниц3 Collector V de LaraAngelie ManingasОценок пока нет

- Practice Problems - Transfer TaxesДокумент2 страницыPractice Problems - Transfer TaxesuchishaiОценок пока нет

- Agosto 25Документ1 страницаAgosto 25dakpi479Оценок пока нет

- P&A - Taxation of Retirement BenefitsДокумент2 страницыP&A - Taxation of Retirement BenefitsCkey ArОценок пока нет

- Chapter 6 Donor S TaxДокумент9 страницChapter 6 Donor S Taxkatniss0013Оценок пока нет

- August 2022Документ1 страницаAugust 2022amitdesai92Оценок пока нет

- IcilДокумент2 страницыIcilMuhammad WaseemОценок пока нет

- Description: 1) Who Are Required To File Documentary Stamp Tax Declaration Return?Документ2 страницыDescription: 1) Who Are Required To File Documentary Stamp Tax Declaration Return?cristinatubleОценок пока нет

- BIR Ruling 133-13Документ2 страницыBIR Ruling 133-13Kyra DiolaОценок пока нет

- Working With The Client: CHAPTER 24: Canadian TaxationДокумент36 страницWorking With The Client: CHAPTER 24: Canadian Taxationlily northОценок пока нет

- Ajio 1662606230415Документ1 страницаAjio 1662606230415Subbi ReddyОценок пока нет

- Form 16 AДокумент2 страницыForm 16 ANitya NarayananОценок пока нет

- Aaykar Bhawan, Ist Floor, Kawdiar Po, Thiruvananthapuram, Kerala, 695003 Email: TVM - DCIT.IT@INCOMETAX - GOV.IN, Office Phone:04712566715Документ1 страницаAaykar Bhawan, Ist Floor, Kawdiar Po, Thiruvananthapuram, Kerala, 695003 Email: TVM - DCIT.IT@INCOMETAX - GOV.IN, Office Phone:04712566715vijuОценок пока нет

- Foxwood Company Data For 2014Документ2 страницыFoxwood Company Data For 2014Vermuda VermudaОценок пока нет

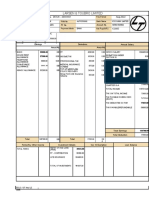

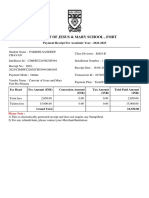

- Convent of Jesus & Mary School, Fort: Payment Receipt For Academic Year - 2022-2023Документ2 страницыConvent of Jesus & Mary School, Fort: Payment Receipt For Academic Year - 2022-2023KDОценок пока нет

- Reinforced Earth India PVT LTD E-11, B1 EXTN, Mcie Mathura Road, New Delhi NEW DELHI - 110044 Delhi Payslip For April - 2019Документ1 страницаReinforced Earth India PVT LTD E-11, B1 EXTN, Mcie Mathura Road, New Delhi NEW DELHI - 110044 Delhi Payslip For April - 2019Kaushik BiswasОценок пока нет

- U.S. Individual Income Tax Return: Filing StatusДокумент5 страницU.S. Individual Income Tax Return: Filing Statuskristen kindleОценок пока нет

- Income Tax Return Online - WEB ONLINE CAДокумент56 страницIncome Tax Return Online - WEB ONLINE CAwebonlineca2024Оценок пока нет

- 1701Q BIR Form PDFДокумент3 страницы1701Q BIR Form PDFJihani A. SalicОценок пока нет

- Flexible Budget ExampleДокумент2 страницыFlexible Budget Examplebrenica_2000Оценок пока нет

- Various Income Taxes & Income Tax Returns Forms: Group 3 Ortega Angel Duterte Dela Cruz Argonsola Marquez AgustinДокумент26 страницVarious Income Taxes & Income Tax Returns Forms: Group 3 Ortega Angel Duterte Dela Cruz Argonsola Marquez AgustinTophe ProvidoОценок пока нет