Вам также может понравиться

- Catalysing Finance and Insurance For NBSДокумент57 страницCatalysing Finance and Insurance For NBSL Prakash JenaОценок пока нет

- The Climate Risk Tool Landscape 2022 SupplementДокумент123 страницыThe Climate Risk Tool Landscape 2022 SupplementL Prakash JenaОценок пока нет

- Report Blended Finance For Climate Investments in IndiaДокумент28 страницReport Blended Finance For Climate Investments in IndiaL Prakash JenaОценок пока нет

- SSRN Id3684926Документ17 страницSSRN Id3684926L Prakash JenaОценок пока нет

- Charging Infra Report JMK Research April 2021 2Документ35 страницCharging Infra Report JMK Research April 2021 2L Prakash JenaОценок пока нет

- Imperial - India Energy Transition Report - 10 Dec 2020Документ29 страницImperial - India Energy Transition Report - 10 Dec 2020L Prakash JenaОценок пока нет

- Market Efficiency and Event StudyДокумент30 страницMarket Efficiency and Event StudyL Prakash JenaОценок пока нет

- G20 Energy Transitions Ministers' Meeting Outcome Document and Chair's SummaryДокумент16 страницG20 Energy Transitions Ministers' Meeting Outcome Document and Chair's SummaryL Prakash JenaОценок пока нет

- Child-Friendly Climate Change HandbookДокумент84 страницыChild-Friendly Climate Change HandbookBibliophileZhenMeiОценок пока нет

- 2020 - Climate Risk - The Price of Drought - JCF - Dec2020Документ26 страниц2020 - Climate Risk - The Price of Drought - JCF - Dec2020L Prakash JenaОценок пока нет

- Energy Taxes and Transition in India WorkingZPaper 9thZFebZ2021Документ28 страницEnergy Taxes and Transition in India WorkingZPaper 9thZFebZ2021L Prakash JenaОценок пока нет

- China - 'S Green Bond Market Jan 2017 - 110117Документ2 страницыChina - 'S Green Bond Market Jan 2017 - 110117L Prakash JenaОценок пока нет

- Impact Investment PolicyДокумент4 страницыImpact Investment PolicyL Prakash JenaОценок пока нет

- Energy Taxes and Transition in India WorkingZPaper 9thZFebZ2021Документ28 страницEnergy Taxes and Transition in India WorkingZPaper 9thZFebZ2021L Prakash JenaОценок пока нет

- Toolkit To Enhance Access To Climate Finance UPDFДокумент72 страницыToolkit To Enhance Access To Climate Finance UPDFL Prakash JenaОценок пока нет

- China's Municipal Finance: Issues and Options: October 2019Документ17 страницChina's Municipal Finance: Issues and Options: October 2019L Prakash JenaОценок пока нет

- Principles of Sustainable Finance book summaryДокумент36 страницPrinciples of Sustainable Finance book summaryL Prakash JenaОценок пока нет

- 10-09 GreenBldg PPTДокумент72 страницы10-09 GreenBldg PPTherokaboss1987Оценок пока нет

- SSRN Id3640706Документ36 страницSSRN Id3640706L Prakash JenaОценок пока нет

- IFC Climate Investment Opportunity Report Dec FINALДокумент140 страницIFC Climate Investment Opportunity Report Dec FINALL Prakash JenaОценок пока нет

- Deloitte Presentation - Solar Rooftop From Discom Perspective - 14092017 PDFДокумент10 страницDeloitte Presentation - Solar Rooftop From Discom Perspective - 14092017 PDFL Prakash JenaОценок пока нет

- MIT Sloan Working Paper Examines Divergence of ESG RatingsДокумент64 страницыMIT Sloan Working Paper Examines Divergence of ESG RatingsL Prakash JenaОценок пока нет

- Agricultural Supply Chain Adaptation Facility Lab Phase 3 Analysis SummaryДокумент14 страницAgricultural Supply Chain Adaptation Facility Lab Phase 3 Analysis SummaryL Prakash JenaОценок пока нет

- Getting To Indias Renewable Energy Targets A Business Case For Institutional InvestmentДокумент35 страницGetting To Indias Renewable Energy Targets A Business Case For Institutional InvestmentL Prakash JenaОценок пока нет

- ERP 2016 LearningObjectives FinalV4 2Документ35 страницERP 2016 LearningObjectives FinalV4 2L Prakash JenaОценок пока нет

- 2009-09-09 Revised RETI Levelized Cost of EnergyДокумент12 страниц2009-09-09 Revised RETI Levelized Cost of EnergyL Prakash JenaОценок пока нет

- Blackrock Essentials Guide To LdiДокумент52 страницыBlackrock Essentials Guide To LdiL Prakash JenaОценок пока нет

- Fundamental Factor of InvestingДокумент18 страницFundamental Factor of InvestingL Prakash JenaОценок пока нет

- KBRA ABS SolarCity LMC Series IV LLC Series 2015-1 New Issue ReportДокумент38 страницKBRA ABS SolarCity LMC Series IV LLC Series 2015-1 New Issue ReportL Prakash JenaОценок пока нет

- Mature Marketing A Winning Formula For A New Era in TelecomsДокумент6 страницMature Marketing A Winning Formula For A New Era in TelecomsAnca MariaОценок пока нет

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5783)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Saic P 3311Документ7 страницSaic P 3311Arshad ImamОценок пока нет

- A Chat (GPT) About The Future of Scientific PublishingДокумент3 страницыA Chat (GPT) About The Future of Scientific Publishingraul kesumaОценок пока нет

- Cinema Urn NBN Si Doc-Z01y9afrДокумент24 страницыCinema Urn NBN Si Doc-Z01y9afrRyan BrandãoОценок пока нет

- Analyzing Transactions To Start A BusinessДокумент22 страницыAnalyzing Transactions To Start A BusinessPaula MabulukОценок пока нет

- Design Thinking SyllabusДокумент6 страницDesign Thinking Syllabussarbast piroОценок пока нет

- English FinalДокумент321 страницаEnglish FinalManuel Campos GuimeraОценок пока нет

- Mitanoor Sultana: Career ObjectiveДокумент2 страницыMitanoor Sultana: Career ObjectiveDebasish DasОценок пока нет

- Intermediate Unit 3bДокумент2 страницыIntermediate Unit 3bgallipateroОценок пока нет

- Voiceless Alveolar Affricate TsДокумент78 страницVoiceless Alveolar Affricate TsZomiLinguisticsОценок пока нет

- Chapter 1Документ30 страницChapter 1Sneha AgarwalОценок пока нет

- How To Make Wall Moulding Design For Rooms Accent Wall Video TutorialsДокумент15 страницHow To Make Wall Moulding Design For Rooms Accent Wall Video Tutorialsdonaldwhale1151Оценок пока нет

- Monson, Concilio Di TrentoДокумент38 страницMonson, Concilio Di TrentoFrancesca Muller100% (1)

- GeM Bidding 2920423 - 2Документ4 страницыGeM Bidding 2920423 - 2Sulvine CharlieОценок пока нет

- Industrial and Organizational PsychologyДокумент21 страницаIndustrial and Organizational PsychologyCris Ben Bardoquillo100% (1)

- Block 2 MVA 026Документ48 страницBlock 2 MVA 026abhilash govind mishraОценок пока нет

- Miriam Garcia Resume 2 1Документ2 страницыMiriam Garcia Resume 2 1api-548501562Оценок пока нет

- APP Eciation: Joven Deloma Btte - Fms B1 Sir. Decederio GaganteДокумент5 страницAPP Eciation: Joven Deloma Btte - Fms B1 Sir. Decederio GaganteJanjan ToscanoОценок пока нет

- BSD ReviewerДокумент17 страницBSD ReviewerMagelle AgbalogОценок пока нет

- Sky Education: Organisation of Commerce and ManagementДокумент12 страницSky Education: Organisation of Commerce and ManagementKiyaara RathoreОценок пока нет

- TOPIC 12 Soaps and DetergentsДокумент14 страницTOPIC 12 Soaps and DetergentsKaynine Kiko50% (2)

- Chapter 15-Writing3 (Thesis Sentence)Документ7 страницChapter 15-Writing3 (Thesis Sentence)Dehan Rakka GusthiraОценок пока нет

- Adjusted School Reading Program of Buneg EsДокумент7 страницAdjusted School Reading Program of Buneg EsGener Taña AntonioОценок пока нет

- Who Are The Prosperity Gospel Adherents by Bradley A KochДокумент46 страницWho Are The Prosperity Gospel Adherents by Bradley A KochSimon DevramОценок пока нет

- Accounting What The Numbers Mean 11th Edition Marshall Solutions Manual 1Документ36 страницAccounting What The Numbers Mean 11th Edition Marshall Solutions Manual 1amandawilkinsijckmdtxez100% (23)

- Presentations - Benefits of WalkingДокумент1 страницаPresentations - Benefits of WalkingEde Mehta WardhanaОценок пока нет

- Infinitive Clauses PDFДокумент3 страницыInfinitive Clauses PDFKatia LeliakhОценок пока нет

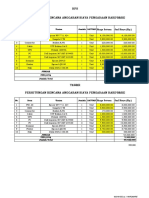

- HPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANДокумент2 страницыHPS Perhitungan Rencana Anggaran Biaya Pengadaan Hardware: No. Item Uraian Jumlah SATUANYanto AstriОценок пока нет

- Your Money Personality Unlock The Secret To A Rich and Happy LifeДокумент30 страницYour Money Personality Unlock The Secret To A Rich and Happy LifeLiz Koh100% (1)

- Test Bank For Understanding Pathophysiology 4th Edition Sue e HuetherДокумент36 страницTest Bank For Understanding Pathophysiology 4th Edition Sue e Huethercarotin.shallowupearp100% (41)

- NAME: - CLASS: - Describing Things Size Shape Colour Taste TextureДокумент1 страницаNAME: - CLASS: - Describing Things Size Shape Colour Taste TextureAnny GSОценок пока нет