Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Statement of Management's Responsibility For Annual Income TaxДокумент2 страницыStatement of Management's Responsibility For Annual Income TaxJohn Heil96% (25)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- MH0ihh081h6754910230616041100202 PDFДокумент2 страницыMH0ihh081h6754910230616041100202 PDFLogan GoadОценок пока нет

- A. Gross Monthly Salary: Certificate of Employment and CompensationДокумент1 страницаA. Gross Monthly Salary: Certificate of Employment and CompensationMary Rose LlameraОценок пока нет

- Paystub Golden Limousine, Inc 20210906 20210919Документ2 страницыPaystub Golden Limousine, Inc 20210906 20210919Alexander Weir-WitmerОценок пока нет

- Salary Certificate Format 2Документ1 страницаSalary Certificate Format 2Haritechnosoft67% (3)

- US Internal Revenue Service: I1040 - 1991Документ80 страницUS Internal Revenue Service: I1040 - 1991IRS100% (2)

- Non-Members With Accumulated Reserves and Undivided Net Savings of Not More Than Ten Million Pesos (P10,000,000.00)Документ2 страницыNon-Members With Accumulated Reserves and Undivided Net Savings of Not More Than Ten Million Pesos (P10,000,000.00)Fairy Ann PeñanoОценок пока нет

- The Different Classification of Taxes in The PhilippinesДокумент2 страницыThe Different Classification of Taxes in The PhilippinesShane Martin100% (1)

- 1208payweek (1) JerryДокумент1 страница1208payweek (1) Jerryesteysi775Оценок пока нет

- W2 & Earnings: Emma MimsДокумент1 страницаW2 & Earnings: Emma MimsIsaiah MimsОценок пока нет

- Quiz 9 FABM 2 Income Taxation WO Answers 1Документ1 страницаQuiz 9 FABM 2 Income Taxation WO Answers 1Gelai BatadОценок пока нет

- Calculation of ATV, AV, CD, RD, SD, VAT, and AIT at Import StageДокумент3 страницыCalculation of ATV, AV, CD, RD, SD, VAT, and AIT at Import StageAccounts Pivot Engg50% (2)

- Dtaa AnnexureДокумент4 страницыDtaa AnnexureAkansha SharmaОценок пока нет

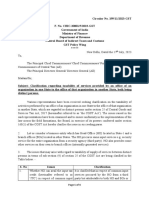

- Circular CGST 199Документ4 страницыCircular CGST 199Jaipur-B Gr-2Оценок пока нет

- Prepaid: Avenue E-Commerce LimitedДокумент1 страницаPrepaid: Avenue E-Commerce LimitedKavya shahОценок пока нет

- US Internal Revenue Service: I1040aДокумент80 страницUS Internal Revenue Service: I1040aIRS100% (1)

- August 2023Документ1 страницаAugust 2023Pradeep G NairОценок пока нет

- Additional Identified Skills Shortage Payment FactsheetДокумент2 страницыAdditional Identified Skills Shortage Payment FactsheetNick SalomoneОценок пока нет

- Tax HW 1Документ3 страницыTax HW 1lexyramdeoОценок пока нет

- 80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensДокумент1 страница80TTB - Provides Deduction Benefit On Interest Income For Senior CitizensArjun VermaОценок пока нет

- Income Tax PPT 4Документ19 страницIncome Tax PPT 4RachnaОценок пока нет

- 2014 TaxReturnДокумент25 страниц2014 TaxReturnNguyen Vu CongОценок пока нет

- Positive Effects of Train Law On The PhilippinesДокумент1 страницаPositive Effects of Train Law On The PhilippinesRHIANA SMILE LOPEZОценок пока нет

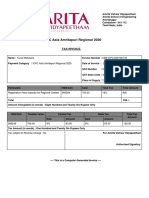

- ICPC Asia Amritapuri Regional 2020: Tax InvoiceДокумент1 страницаICPC Asia Amritapuri Regional 2020: Tax InvoiceKUNAL MAKWANAОценок пока нет

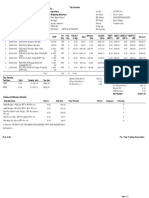

- Pedigree BillДокумент5 страницPedigree BillpeerarslanОценок пока нет

- Declaration DetailsДокумент1 страницаDeclaration DetailsIRADUKUNDA EnockОценок пока нет

- 18 - Royalty Payment ScheduleДокумент2 страницы18 - Royalty Payment ScheduleDJ DogasОценок пока нет

- Alaska: Articles of IncorporationДокумент2 страницыAlaska: Articles of IncorporationFinally Home RescueОценок пока нет

- Sworn Declaration: Annex DДокумент1 страницаSworn Declaration: Annex Djanice corderoОценок пока нет