Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Assignment III-LGS311-12th-DECДокумент2 страницыAssignment III-LGS311-12th-DECMohammad Iqbal SekandariОценок пока нет

- Pengaruh Marketing Public Relations Dan Kualitas Pelayanan Terhadap Citra Rumah Sakit Syafira PekanbaruДокумент14 страницPengaruh Marketing Public Relations Dan Kualitas Pelayanan Terhadap Citra Rumah Sakit Syafira PekanbaruRahmaОценок пока нет

- Manager Training Outline and Checklist: OrientationДокумент3 страницыManager Training Outline and Checklist: OrientationHuu Thanh TranОценок пока нет

- Practical Accounting Problem 2Документ18 страницPractical Accounting Problem 2JimmyChao100% (2)

- Tariq Zahid Bhurgari-1411561-BBA 4BДокумент4 страницыTariq Zahid Bhurgari-1411561-BBA 4BAbdul Moiz YousfaniОценок пока нет

- Business Proposal HCL AceДокумент2 страницыBusiness Proposal HCL AceSaurabh KadamОценок пока нет

- Banyan TreeДокумент36 страницBanyan Treeabhi4u.kumar67% (3)

- Ferrell 12e PPT Ch02 RevДокумент39 страницFerrell 12e PPT Ch02 RevmichaelОценок пока нет

- Andreessen Horowitz FinalДокумент4 страницыAndreessen Horowitz FinalYuqin ChenОценок пока нет

- HDFC Bank Report MbaДокумент82 страницыHDFC Bank Report Mba8542ish83% (18)

- Go-To-Market Strategies - The Ultimate Playbook For Startup Expansion To International MarketsДокумент40 страницGo-To-Market Strategies - The Ultimate Playbook For Startup Expansion To International MarketsLivia EllenОценок пока нет

- S 8-Category Driver Analysis-Dr PlaviniДокумент19 страницS 8-Category Driver Analysis-Dr PlaviniPallav JainОценок пока нет

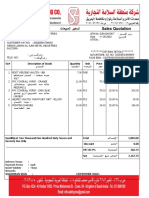

- Sales Quotation: Salesman Sign: Customer SignДокумент1 страницаSales Quotation: Salesman Sign: Customer SignjacobОценок пока нет

- Takehome - Quiz - Manac - Docx Filename - UTF-8''Takehome Quiz Manac-1Документ3 страницыTakehome - Quiz - Manac - Docx Filename - UTF-8''Takehome Quiz Manac-1Sharmaine SurОценок пока нет

- Engagement & Quality Control Standards: CA Sarthak JainДокумент48 страницEngagement & Quality Control Standards: CA Sarthak Jainzayn mallikОценок пока нет

- Who Is An Entrepreneur. Timothy MaheaДокумент21 страницаWho Is An Entrepreneur. Timothy MaheaMaheaОценок пока нет

- Ais ReportДокумент2 страницыAis ReportMarianne Angelica AndaquigОценок пока нет

- Answer - Tutorial - CorporationДокумент3 страницыAnswer - Tutorial - CorporationBanulekaОценок пока нет

- Effective SME Family Business Succession StrategiesДокумент9 страницEffective SME Family Business Succession StrategiesPatricia MonteferranteОценок пока нет

- Use of Social Media in The Marketing of Agricultural Products and Efficiency in The Cost of Advertisement of Agricultural Products in South West NigeriaДокумент10 страницUse of Social Media in The Marketing of Agricultural Products and Efficiency in The Cost of Advertisement of Agricultural Products in South West NigeriaEditor IJTSRDОценок пока нет

- Meetings and ProceedingsДокумент11 страницMeetings and ProceedingssreeОценок пока нет

- Fundamental and Technical Analysis of Mutual FundsДокумент52 страницыFundamental and Technical Analysis of Mutual FundsAnnu PariharОценок пока нет

- End User License Agreement BOOM LIBRARY For Single Users IMPORTANT-READ CAREFULLY: This BOOM Library End-User License Agreement (Or "EULA")Документ3 страницыEnd User License Agreement BOOM LIBRARY For Single Users IMPORTANT-READ CAREFULLY: This BOOM Library End-User License Agreement (Or "EULA")jumoОценок пока нет

- SAP Manager SD/OTC in USA Resume Sheetal KothariДокумент7 страницSAP Manager SD/OTC in USA Resume Sheetal KothariSheetalKothari0% (1)

- 05 Quiz 1Документ2 страницы05 Quiz 1lunaОценок пока нет

- Accounting Rate of ReturnДокумент16 страницAccounting Rate of Returnshanky631Оценок пока нет

- Business Policy SyllabusДокумент2 страницыBusiness Policy SyllabusMubashair Rafi Sheikh rollno 1Оценок пока нет

- Amity University, Noida: Semester-1Документ4 страницыAmity University, Noida: Semester-1SANCHIT VERMAОценок пока нет

- PPT-Posting To The Ledger, Preparing Trial Balance & AJEДокумент22 страницыPPT-Posting To The Ledger, Preparing Trial Balance & AJEela cagsОценок пока нет

- Demand and Analysis NumericalsДокумент31 страницаDemand and Analysis NumericalsRajan BhadoriyaОценок пока нет