Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- AuditingДокумент13 страницAuditingVenilyn Valencia75% (4)

- Investor Agreement ContractДокумент4 страницыInvestor Agreement ContractGian Joaquin0% (1)

- Jesse Livermore 25 Regole Di TradingДокумент19 страницJesse Livermore 25 Regole Di TradingFabio ColomboОценок пока нет

- Answers Risk Management and Financial Institutions 4th EditionДокумент58 страницAnswers Risk Management and Financial Institutions 4th EditionMincong ZhouОценок пока нет

- Investment Banking Deal ProcessДокумент25 страницInvestment Banking Deal Processdkgrinder100% (1)

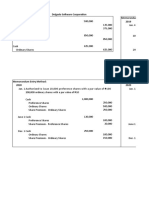

- Memorandum and Journal Entry Methods for Share Capital TransactionsДокумент3 страницыMemorandum and Journal Entry Methods for Share Capital TransactionsFeiya Liu100% (1)

- GoldmanДокумент244 страницыGoldmanC.Оценок пока нет

- Mba Project - Finance, Marketing, Human ResourceДокумент4 страницыMba Project - Finance, Marketing, Human ResourceN.MUTHUKUMARAN67% (18)

- Equitable PCI Bank Liable for Manager's CheckДокумент2 страницыEquitable PCI Bank Liable for Manager's CheckAntonJohnVincentFrias100% (2)

- A Study of e S in HMT MTL KalamasseryДокумент93 страницыA Study of e S in HMT MTL KalamasserySAMDAVIDCBОценок пока нет

- Smu Mba-4 2011 Assignment Mu0006-Set2Документ6 страницSmu Mba-4 2011 Assignment Mu0006-Set2SAMDAVIDCBОценок пока нет

- Smu Mba-4 2011 Assignment Mb0037-Set1Документ14 страницSmu Mba-4 2011 Assignment Mb0037-Set1SAMDAVIDCBОценок пока нет

- Smu Mba HR 2011 Assignment Mb0036-Set2Документ9 страницSmu Mba HR 2011 Assignment Mb0036-Set2SAMDAVIDCBОценок пока нет

- Smu Mba-4 2011 Assignment Mu0006-Set1Документ7 страницSmu Mba-4 2011 Assignment Mu0006-Set1SAMDAVIDCBОценок пока нет

- Smu Mba 4 HR Assignment Mb0036-Set1Документ24 страницыSmu Mba 4 HR Assignment Mb0036-Set1SAMDAVIDCB100% (1)

- Smu Mba-4 2011 Assignment Mb0037-Set1Документ14 страницSmu Mba-4 2011 Assignment Mb0037-Set1SAMDAVIDCBОценок пока нет

- Smu Mba HR 2011 Assignment Mb0036-Set2Документ9 страницSmu Mba HR 2011 Assignment Mb0036-Set2SAMDAVIDCBОценок пока нет

- Smu Mba 4 HR Assignment Mb0036-Set1Документ24 страницыSmu Mba 4 HR Assignment Mb0036-Set1SAMDAVIDCB100% (1)

- Butterfly That Never FlewДокумент11 страницButterfly That Never FlewSAMDAVIDCBОценок пока нет

- Story of AppreciationДокумент2 страницыStory of AppreciationSandeep TawareОценок пока нет

- MU0001-Manpower Planning and Model - PaperДокумент10 страницMU0001-Manpower Planning and Model - PaperSujeet R SinghОценок пока нет

- Smu Mba Question PaperДокумент17 страницSmu Mba Question PaperSAMDAVIDCBОценок пока нет

- Patel Engineering AGM NoticeДокумент165 страницPatel Engineering AGM NoticeArunesh SinghОценок пока нет

- 2012 Starwood Proxy Statement & 2011 Annual ReportДокумент169 страниц2012 Starwood Proxy Statement & 2011 Annual ReportHuy MaiОценок пока нет

- 3.overview of NHAIДокумент5 страниц3.overview of NHAIBharat Reddy100% (1)

- Coco Life Audited Financial Statement 2014Документ95 страницCoco Life Audited Financial Statement 2014Angel PortosaОценок пока нет

- Investment in Allied UndertakingsДокумент4 страницыInvestment in Allied Undertakingssop_pologОценок пока нет

- CalPERS Annual Investment Report SummaryДокумент296 страницCalPERS Annual Investment Report SummaryChris WatkinsОценок пока нет

- HealthSouth Scandal and Accounting Fraud ExplainedДокумент11 страницHealthSouth Scandal and Accounting Fraud ExplainedAnshak KumarОценок пока нет

- Notheren MotorsДокумент10 страницNotheren MotorsA Paula Cruz FranciscoОценок пока нет

- Chapter 5Документ28 страницChapter 5Shoaib ZaheerОценок пока нет

- Consumer Financing in Pakistan Issues & Challenges - PROJECTДокумент88 страницConsumer Financing in Pakistan Issues & Challenges - PROJECTFarman Memon100% (1)

- 2016-FAC611S-Chapter 15 Property Plant and Equipment 2013Документ32 страницы2016-FAC611S-Chapter 15 Property Plant and Equipment 2013Bol Sab SachОценок пока нет

- LATAM AIRLINES GROUP S A 09-2012 (Inglés)Документ172 страницыLATAM AIRLINES GROUP S A 09-2012 (Inglés)chequeadoОценок пока нет

- City of London LSE David KynastonДокумент2 страницыCity of London LSE David Kynastonmary engОценок пока нет

- International Valuation Standards - 2020 MCQДокумент18 страницInternational Valuation Standards - 2020 MCQNikhil Tidke100% (2)

- PNB Vs Andrada ElectricДокумент14 страницPNB Vs Andrada ElectricYe Seul DvngrcОценок пока нет

- Accounting 5008 Ch18 SolutionsДокумент4 страницыAccounting 5008 Ch18 Solutionsferoz_bilalОценок пока нет

- Fdnacct 3-18 To 3-19 FS TemplateДокумент4 страницыFdnacct 3-18 To 3-19 FS TemplateFAFAFAОценок пока нет

- Claw PPT - ProspectusДокумент27 страницClaw PPT - Prospectusitika DhawanОценок пока нет

- APC313 Assessment Brief January19Документ3 страницыAPC313 Assessment Brief January19Hoài Sơn VũОценок пока нет

- Financial Year: 2020-21 Assessment Year: 2021-22: TDS RATE CHART FY: 2020-21 (AY: 2021-22)Документ2 страницыFinancial Year: 2020-21 Assessment Year: 2021-22: TDS RATE CHART FY: 2020-21 (AY: 2021-22)Mahesh Shinde100% (1)

- International Capital BudgetingДокумент28 страницInternational Capital BudgetingMatt ToothacreОценок пока нет

- Cash Flow Statement Kotak Mahindra 2016Документ80 страницCash Flow Statement Kotak Mahindra 2016Nagireddy Kalluri100% (2)