Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- Service MRKTG 03Документ17 страницService MRKTG 03annie4321Оценок пока нет

- Service MRKTG 03Документ17 страницService MRKTG 03annie4321Оценок пока нет

- Plant Location Factors & TypesДокумент40 страницPlant Location Factors & Typesannie4321Оценок пока нет

- Globalisation in Indian EconomyДокумент6 страницGlobalisation in Indian Economyannie4321Оценок пока нет

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Tutorial - The Time Value of MoneyДокумент6 страницTutorial - The Time Value of MoneyFahmi CAОценок пока нет

- Performance Appraisal System of AB Bank LTDДокумент67 страницPerformance Appraisal System of AB Bank LTDMahmud Abdullah100% (1)

- Plastene India Ltd.Документ326 страницPlastene India Ltd.Ganesh100% (1)

- Basic Sales TrainingДокумент36 страницBasic Sales TrainingManraj Singh100% (1)

- Export Finance: Presented By: Tamanna M.FTECH 2010-12 NIFT, GandhinagarДокумент19 страницExport Finance: Presented By: Tamanna M.FTECH 2010-12 NIFT, Gandhinagartamanna88Оценок пока нет

- CashBook (SEM2)Документ4 страницыCashBook (SEM2)Xavier University- Economics SocietyОценок пока нет

- June 14 PDFДокумент4 страницыJune 14 PDFSusan Romdenne100% (1)

- World Retail Banking Report 2020 PDFДокумент36 страницWorld Retail Banking Report 2020 PDFBui Hoang Giang100% (1)

- Running Errands #2: Lesson 16Документ14 страницRunning Errands #2: Lesson 16Camila ReyesОценок пока нет

- Implied Authority of A Partner: A Comparative Study: Assistant Professor of LawДокумент20 страницImplied Authority of A Partner: A Comparative Study: Assistant Professor of LawHimanshuОценок пока нет

- Diamond Bank: Makes A Success Story ofДокумент36 страницDiamond Bank: Makes A Success Story ofGaurav Shashi SaxenaОценок пока нет

- High Sea Sales Agreement FormatДокумент2 страницыHigh Sea Sales Agreement FormatMradul Bansal43% (7)

- R DJVFuh 3 Ri LB 7 Ep RДокумент13 страницR DJVFuh 3 Ri LB 7 Ep RKondayya JuttigaОценок пока нет

- IcotermsДокумент3 страницыIcotermsMiguel Estrada DíazОценок пока нет

- 21.) UCPB V Samuel and BelusoДокумент2 страницы21.) UCPB V Samuel and BelusojoyceОценок пока нет

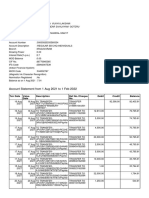

- Statement of Axis Account No:919010012738847 For The Period (From: 08-09-2020 To: 07-09-2021)Документ2 страницыStatement of Axis Account No:919010012738847 For The Period (From: 08-09-2020 To: 07-09-2021)Sayan SarkarОценок пока нет

- Transforming Rural YouthДокумент340 страницTransforming Rural Youthudi9690% (2)

- Maphar Constructions Private LimitedДокумент2 страницыMaphar Constructions Private LimitedSWARUPAОценок пока нет

- Sumit Black BookДокумент51 страницаSumit Black BookSuraj BenbansiОценок пока нет

- Resume-Sherry ThayerДокумент2 страницыResume-Sherry Thayerapi-315331717Оценок пока нет

- Proof of Cash: Intermediate Accounting Part 1Документ1 страницаProof of Cash: Intermediate Accounting Part 1Steffanie Olivar0% (1)

- Insurance Law-ContributionДокумент5 страницInsurance Law-ContributionDavid FongОценок пока нет

- CEO Analysis of Cherat Cement CompanyДокумент30 страницCEO Analysis of Cherat Cement Companyfaisal aminОценок пока нет

- Performance of Mutual FundsДокумент79 страницPerformance of Mutual FundsSrujan KadarlaОценок пока нет

- Phil Guaranty v. CIR DigestsДокумент2 страницыPhil Guaranty v. CIR Digestspinkblush717100% (1)

- VW Approved Used Cover BookletДокумент18 страницVW Approved Used Cover BookletagathianОценок пока нет

- 05DEC2023Документ4 страницы05DEC2023Fakruul HaZminОценок пока нет

- EB Rainer wl11 IIS3 WM PDFДокумент580 страницEB Rainer wl11 IIS3 WM PDFran_chanОценок пока нет

- Isa 805Документ13 страницIsa 805baabasaamОценок пока нет

- Suite Talk Web Services Records GuideДокумент194 страницыSuite Talk Web Services Records GuideZettoX0% (1)