Вам также может понравиться

- Case Study - Stella JonesДокумент7 страницCase Study - Stella JonesLai Kok WeiОценок пока нет

- CNBC Transcript 2006 2019 02Документ1 575 страницCNBC Transcript 2006 2019 02N BОценок пока нет

- Washington PostBuffett Analysis1Документ2 страницыWashington PostBuffett Analysis1Calvin ChangОценок пока нет

- Mark Yusko's Presentation at iCIO: Year of The AlligatorДокумент123 страницыMark Yusko's Presentation at iCIO: Year of The AlligatorValueWalkОценок пока нет

- Ruane, Cunniff & Goldfarb Investor Day 2009 - TranscriptДокумент24 страницыRuane, Cunniff & Goldfarb Investor Day 2009 - TranscriptThe Manual of IdeasОценок пока нет

- Geico Case Study PDFДокумент22 страницыGeico Case Study PDFMichael Cano LombardoОценок пока нет

- Investing in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketОт EverandInvesting in Credit Hedge Funds: An In-Depth Guide to Building Your Portfolio and Profiting from the Credit MarketОценок пока нет

- Blackbook Project On Foreign Exchange and Its Risk Management - 237312993Документ61 страницаBlackbook Project On Foreign Exchange and Its Risk Management - 237312993Aman Tiwari75% (4)

- Bruce Berkowitz On WFC 90sДокумент4 страницыBruce Berkowitz On WFC 90sVu Latticework PoetОценок пока нет

- 1976 Buffett Letter About Geico - FutureBlindДокумент4 страницы1976 Buffett Letter About Geico - FutureBlindPradeep RaghunathanОценок пока нет

- BerkshireHandout2012Final 0 PDFДокумент4 страницыBerkshireHandout2012Final 0 PDFHermes TristemegistusОценок пока нет

- Interviews Value Investing Guru Roger Montgomery About ValueableДокумент3 страницыInterviews Value Investing Guru Roger Montgomery About Valueableqwerqwer123100% (1)

- The 400 Richest Americans" List, and What Is The Source of His WealthДокумент16 страницThe 400 Richest Americans" List, and What Is The Source of His WealthCindy MingОценок пока нет

- RV Capital June 2015 LetterДокумент8 страницRV Capital June 2015 LetterCanadianValueОценок пока нет

- Distressed Debt InvestingДокумент5 страницDistressed Debt Investingjt322Оценок пока нет

- Michael L Riordan, The Founder and CEO of Gilead Sciences, and Warren E Buffett, Berkshire Hathaway Chairman: CorrespondenceДокумент5 страницMichael L Riordan, The Founder and CEO of Gilead Sciences, and Warren E Buffett, Berkshire Hathaway Chairman: CorrespondenceOpenSquareCommons100% (27)

- Berkshire Hathaway Audit Committee Report On Trading in Lubrizol Corporation Shares by David L. SokolДокумент18 страницBerkshire Hathaway Audit Committee Report On Trading in Lubrizol Corporation Shares by David L. SokolCNBCОценок пока нет

- SchlossДокумент188 страницSchlossEduardo FreitasОценок пока нет

- Three Hours With Warren - Complete Transcript - 2008-08-22Документ62 страницыThree Hours With Warren - Complete Transcript - 2008-08-22drunkdealmasterОценок пока нет

- Letter About Carl IcahnДокумент4 страницыLetter About Carl IcahnCNBC.com100% (1)

- Bridge With BuffetДокумент12 страницBridge With BuffetTraderCat SolarisОценок пока нет

- Profiles in Investing - Marty Whitman (Bottom Line 2004)Документ1 страницаProfiles in Investing - Marty Whitman (Bottom Line 2004)tatsrus1Оценок пока нет

- 1 L I LL I: WWW EscДокумент4 страницы1 L I LL I: WWW EscforexmastertanОценок пока нет

- Profit Guru Bill NygrenДокумент5 страницProfit Guru Bill NygrenekramcalОценок пока нет

- Value Investor Insight Play Your GameДокумент4 страницыValue Investor Insight Play Your Gamevouzvouz7127100% (1)

- Warren Buffett CNBC Transcript Feb-29-2016 PDFДокумент92 страницыWarren Buffett CNBC Transcript Feb-29-2016 PDFAndri ChandraОценок пока нет

- Schloss 2006Документ2 страницыSchloss 2006Logic Gate Capital100% (1)

- Value Investing Review of Warren Buffetts Investment Philosophy and PracticeДокумент13 страницValue Investing Review of Warren Buffetts Investment Philosophy and PracticeRoberto GonzasОценок пока нет

- In Search of The "Buffett Premium" - Free SampleДокумент22 страницыIn Search of The "Buffett Premium" - Free SampleRationalWalkОценок пока нет

- Mohnish Pabrai Chicago Meeting 2009 NotesДокумент3 страницыMohnish Pabrai Chicago Meeting 2009 NotesalexprywesОценок пока нет

- Bruce BerkowitzДокумент35 страницBruce BerkowitznewbietraderОценок пока нет

- Warren Buffett and GEICO Case StudyДокумент18 страницWarren Buffett and GEICO Case StudyReymond Jude PagcoОценок пока нет

- Buffett On ValuationДокумент7 страницBuffett On ValuationAyush AggarwalОценок пока нет

- BH 2015 AmДокумент14 страницBH 2015 Amva.apg.90100% (2)

- Graham and Doddsville - Issue 9 - Spring 2010Документ33 страницыGraham and Doddsville - Issue 9 - Spring 2010g4nz0Оценок пока нет

- Daily Journal Meeting Detailed Notes From Charlie MungerДокумент29 страницDaily Journal Meeting Detailed Notes From Charlie MungerGary Ribe100% (1)

- How David Sokol Lost His WayДокумент3 страницыHow David Sokol Lost His WayBisto MasiloОценок пока нет

- Buffett in Hindsight Foresight (2002)Документ8 страницBuffett in Hindsight Foresight (2002)MWGENERALОценок пока нет

- The Playing Field - Graham Duncan - MediumДокумент11 страницThe Playing Field - Graham Duncan - MediumPradeep RaghunathanОценок пока нет

- David Einhorn MSFT Speech-2006Документ5 страницDavid Einhorn MSFT Speech-2006mikesfbayОценок пока нет

- Vinall 2014 - ValuationДокумент19 страницVinall 2014 - ValuationOmar MalikОценок пока нет

- Summary New Venture ManagementДокумент57 страницSummary New Venture Managementbetter.bambooОценок пока нет

- Bibliophile Warren Buffett's Letter 1957-2017Документ165 страницBibliophile Warren Buffett's Letter 1957-2017Vishal Kedia0% (1)

- Schloss-10 11 06Документ3 страницыSchloss-10 11 06Logic Gate CapitalОценок пока нет

- Boyar ValueInvestingCongress 131609Документ71 страницаBoyar ValueInvestingCongress 131609vikramb1Оценок пока нет

- Warren Buffett - PetrochinaДокумент2 страницыWarren Buffett - PetrochinaJohn ReedОценок пока нет

- The Future of Common Stocks Benjamin Graham PDFДокумент8 страницThe Future of Common Stocks Benjamin Graham PDFPrashant AgarwalОценок пока нет

- To: From: Christopher M. Begg, CFA - CEO, Chief Investment Officer, and Co-Founder Date: July 16, 2012 ReДокумент13 страницTo: From: Christopher M. Begg, CFA - CEO, Chief Investment Officer, and Co-Founder Date: July 16, 2012 Recrees25Оценок пока нет

- Amitabh Singhvi L MOI Interview L JUNE-2011Документ6 страницAmitabh Singhvi L MOI Interview L JUNE-2011Wayne GonsalvesОценок пока нет

- Arithmetic of EquitiesДокумент5 страницArithmetic of Equitiesrwmortell3580Оценок пока нет

- Osmium Partners Presentation - Spark Networks IncДокумент86 страницOsmium Partners Presentation - Spark Networks IncCanadianValue100% (1)

- Steve Romick SpeechДокумент28 страницSteve Romick SpeechCanadianValueОценок пока нет

- PremWatsaFairfaxNewsletter7 12-20-11Документ6 страницPremWatsaFairfaxNewsletter7 12-20-11able1Оценок пока нет

- Financial Fine Print: Uncovering a Company's True ValueОт EverandFinancial Fine Print: Uncovering a Company's True ValueРейтинг: 3 из 5 звезд3/5 (3)

- To the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioОт EverandTo the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioОценок пока нет

- Competitive Advantage in Investing: Building Winning Professional PortfoliosОт EverandCompetitive Advantage in Investing: Building Winning Professional PortfoliosОценок пока нет

- Pilgrimage to Warren Buffett's Omaha: A Hedge Fund Manager's Dispatches from Inside the Berkshire Hathaway Annual MeetingОт EverandPilgrimage to Warren Buffett's Omaha: A Hedge Fund Manager's Dispatches from Inside the Berkshire Hathaway Annual MeetingРейтинг: 4 из 5 звезд4/5 (2)

- S.15 FINTECH Fintech and The City Sandbox 2 0 Policy and Regulatory Reform Proposals PDFДокумент34 страницыS.15 FINTECH Fintech and The City Sandbox 2 0 Policy and Regulatory Reform Proposals PDFNicolás J. Baquero M.Оценок пока нет

- HW#10 11.2 and 11.5 Implicit Diff and Application - MATH 104 - Fall 2023, Fall 2023 WebAssignДокумент1 страницаHW#10 11.2 and 11.5 Implicit Diff and Application - MATH 104 - Fall 2023, Fall 2023 WebAssignAbdullah AlaamОценок пока нет

- This Prospectus Is Important and Requires Your Immediate AttentionДокумент67 страницThis Prospectus Is Important and Requires Your Immediate Attentionmartin shineОценок пока нет

- Lecture 33 Credit+Analysis+-+Corporate+Credit+Analysis+ (Ratios)Документ33 страницыLecture 33 Credit+Analysis+-+Corporate+Credit+Analysis+ (Ratios)Taan100% (1)

- Investment AlternativesДокумент32 страницыInvestment AlternativesMadihaBhattiОценок пока нет

- Universiti Teknologi Mara Common Test 1: Confidential AC/AUG 2015/MAF253Документ6 страницUniversiti Teknologi Mara Common Test 1: Confidential AC/AUG 2015/MAF253Bonna Della TianamОценок пока нет

- Application of Fibonacci Numbers On Technical Analysis of Eur/Usd Currency PairДокумент10 страницApplication of Fibonacci Numbers On Technical Analysis of Eur/Usd Currency PairMohammad ArnoldОценок пока нет

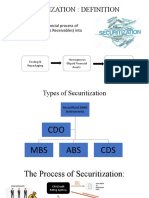

- SECURITIZATIONДокумент5 страницSECURITIZATIONASHISH KUMARОценок пока нет

- Pointers MKTG60Документ3 страницыPointers MKTG60Shan Sai BuladoОценок пока нет

- Rule of 69 - Meaning, Benefits, Limitations and MoreДокумент4 страницыRule of 69 - Meaning, Benefits, Limitations and MoreCandy DollОценок пока нет

- Farming AafsДокумент178 страницFarming AafsKezza Marie LuengoОценок пока нет

- AmatsДокумент3 страницыAmatsAldrin LiwanagОценок пока нет

- Aaafx Bonus T&C v1Документ3 страницыAaafx Bonus T&C v1alvin allesandroОценок пока нет

- E StatementДокумент10 страницE StatementMahendra LakkavaramОценок пока нет

- Clifford Chance Client Briefing IIFM MCM Agreement 16-Nov-2014Документ3 страницыClifford Chance Client Briefing IIFM MCM Agreement 16-Nov-2014karim meddebОценок пока нет

- MFM Chap-01Документ17 страницMFM Chap-01VEDANT XОценок пока нет

- Dabba TradingДокумент2 страницыDabba Tradingkushal90Оценок пока нет

- A Study On Portfolio ManagementДокумент3 страницыA Study On Portfolio ManagementEditor IJTSRDОценок пока нет

- Relevant Provisions of Companies ActДокумент19 страницRelevant Provisions of Companies Actrthi04Оценок пока нет

- Sol. Man. - Chapter 10 She 1Документ5 страницSol. Man. - Chapter 10 She 1Nikky Bless LeonarОценок пока нет

- NNFX Strategy Flow ChartДокумент2 страницыNNFX Strategy Flow ChartruwanzОценок пока нет

- Case Study AnswerДокумент3 страницыCase Study AnswerJAY MARK TANOОценок пока нет

- Quiz Black Scholes ModelДокумент3 страницыQuiz Black Scholes ModelMark AdrianОценок пока нет

- A2 Form MotherДокумент1 страницаA2 Form MotherStarОценок пока нет

- Impact of Latency On Forex TradingДокумент4 страницыImpact of Latency On Forex TradingalirahebiОценок пока нет

- Reliance Industries DCFДокумент35 страницReliance Industries DCFChirag SharmaОценок пока нет

- 506B Legal Aspects of Finance and Security LawsДокумент2 страницы506B Legal Aspects of Finance and Security LawsManthanОценок пока нет

- Basel II Capital Accord Report at SBPДокумент48 страницBasel II Capital Accord Report at SBPAamir Raza100% (1)

- Resume Joana de S Saad 1688571509Документ2 страницыResume Joana de S Saad 1688571509Hola HoolaОценок пока нет