Вам также может понравиться

- Federal Income Tax 1040 Activity PDFДокумент14 страницFederal Income Tax 1040 Activity PDFRobert Brant100% (1)

- Cheesecakefacory PDFДокумент1 страницаCheesecakefacory PDFTate YatesОценок пока нет

- DateДокумент4 страницыDatechatiresОценок пока нет

- Final Paycheck Acknowledgment-KHДокумент2 страницыFinal Paycheck Acknowledgment-KHJennifer CooperriderОценок пока нет

- PCДокумент1 страницаPCtpsroxОценок пока нет

- SVG Tax Tables-2018Документ16 страницSVG Tax Tables-2018Tamara Wilson0% (1)

- Senator Murray Budget Memo 1-24Документ12 страницSenator Murray Budget Memo 1-24Ezra Klein100% (1)

- The Economists' Voice 2.0: The Financial Crisis, Health Care Reform, and MoreОт EverandThe Economists' Voice 2.0: The Financial Crisis, Health Care Reform, and MoreОценок пока нет

- Bangladesh TIN Certificate OnlineДокумент1 страницаBangladesh TIN Certificate Onlinearman_27727627150% (2)

- House Budget Control ActДокумент9 страницHouse Budget Control ActMichael Robert HusseyОценок пока нет

- CBO Letter of 7/27/2011 On Revised Boehner PlanДокумент10 страницCBO Letter of 7/27/2011 On Revised Boehner PlanDoug MataconisОценок пока нет

- The Budget Control Act of 2011: The Effects On Spending and The Budget Deficit When The Automatic Spending Cuts Are ImplementedДокумент19 страницThe Budget Control Act of 2011: The Effects On Spending and The Budget Deficit When The Automatic Spending Cuts Are ImplementedcaseywootenОценок пока нет

- CBO Analysis Obama's Budget 2012 3/18Документ22 страницыCBO Analysis Obama's Budget 2012 3/18Darla DawaldОценок пока нет

- FY 13 OMB JC Sequestration ReportДокумент83 страницыFY 13 OMB JC Sequestration ReportCeleste KatzОценок пока нет

- Budget Update March 142006Документ10 страницBudget Update March 142006Committee For a Responsible Federal BudgetОценок пока нет

- CBO Letter March 5Документ18 страницCBO Letter March 5ZerohedgeОценок пока нет

- Budget Update August 2005Документ6 страницBudget Update August 2005Committee For a Responsible Federal BudgetОценок пока нет

- Us Cbo Budget DeficitsДокумент18 страницUs Cbo Budget Deficitswmartin46Оценок пока нет

- J What Is SequestrationДокумент3 страницыJ What Is SequestrationDanica BalinasОценок пока нет

- CBO Debt Deal EstimateДокумент17 страницCBO Debt Deal EstimateAustin DeneanОценок пока нет

- Rep Paul Ryan On Obamas 2012 Budget and BeyondДокумент19 страницRep Paul Ryan On Obamas 2012 Budget and BeyondKim HedumОценок пока нет

- CBO Score and Assessment To Repeal ObamacareДокумент10 страницCBO Score and Assessment To Repeal ObamacareDarla DawaldОценок пока нет

- DeficitReduction ScreenДокумент46 страницDeficitReduction ScreenPeggy W SatterfieldОценок пока нет

- US CBO Report: Fiscal Restraint That Is Scheduled To Occur in 2013 (May, 2012)Документ10 страницUS CBO Report: Fiscal Restraint That Is Scheduled To Occur in 2013 (May, 2012)wmartin46Оценок пока нет

- 2013 CB Sfaff OverviewДокумент79 страниц2013 CB Sfaff OverviewChris Capper LiebenthalОценок пока нет

- Sequestration and The Super Committee: Background On The Budget Control ActДокумент4 страницыSequestration and The Super Committee: Background On The Budget Control Actwatton1217Оценок пока нет

- DeficitReduction PrintДокумент35 страницDeficitReduction PrintPeggy W SatterfieldОценок пока нет

- CBO Report On The Cost of The Breast Cancer Research Semi Postal StampДокумент4 страницыCBO Report On The Cost of The Breast Cancer Research Semi Postal StampPostalReporter.comОценок пока нет

- 2010 Budget Perspective: The Real Deficit Effect of The Health BillДокумент5 страниц2010 Budget Perspective: The Real Deficit Effect of The Health BillWashington ExaminerОценок пока нет

- Democratic Budget Framework: A Balanced, Pro-Growth, and Fair Deficit Reduction PlanДокумент4 страницыDemocratic Budget Framework: A Balanced, Pro-Growth, and Fair Deficit Reduction PlanInterActionОценок пока нет

- GNYHA Memo New York State Budget 2012Документ12 страницGNYHA Memo New York State Budget 2012ahawkins2865Оценок пока нет

- OMB Sequestration Update Report To The President and Congress For Fiscal Year 2013 August 20, 2012Документ22 страницыOMB Sequestration Update Report To The President and Congress For Fiscal Year 2013 August 20, 2012Peggy W SatterfieldОценок пока нет

- CBO January 2015 Outlook On ObamacareДокумент15 страницCBO January 2015 Outlook On ObamacareZenger NewsОценок пока нет

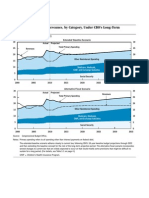

- Primary Spending and Revenues, by Category, Under CBO's Long-Term Budget ScenariosДокумент25 страницPrimary Spending and Revenues, by Category, Under CBO's Long-Term Budget ScenariosPeggy W SatterfieldОценок пока нет

- Spending Review 2Документ25 страницSpending Review 2Hendro Try WidiantoОценок пока нет

- Long-Term Fiscal Projections NotesДокумент6 страницLong-Term Fiscal Projections NotesLokiОценок пока нет

- A Message To The PublicДокумент24 страницыA Message To The Publicthe kingfishОценок пока нет

- Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Документ50 страницDouglas W. Elmendorf, Director U.S. Congress Washington, DC 20515josephragoОценок пока нет

- Omb Sequestration ReportДокумент394 страницыOmb Sequestration ReportJake GrovumОценок пока нет

- Budget Analysis 2011 12Документ7 страницBudget Analysis 2011 12s lalithaОценок пока нет

- 2020 HB30 ReconvenedExecAmendHalfsheets 04112020Документ159 страниц2020 HB30 ReconvenedExecAmendHalfsheets 04112020Lowell FeldОценок пока нет

- Testimony On The 2013 Long-Term Budget OutlookДокумент8 страницTestimony On The 2013 Long-Term Budget OutlookSteven HansenОценок пока нет

- Legislative Fiscal Office Analysis of HB 1 Reengrossed (Updated 5/25/15)Документ135 страницLegislative Fiscal Office Analysis of HB 1 Reengrossed (Updated 5/25/15)RepNLandryОценок пока нет

- Congressional Budget Office U.S. Congress Washington, DC 20515Документ17 страницCongressional Budget Office U.S. Congress Washington, DC 20515api-26139761Оценок пока нет

- Economic Impacts of Waiting To Resolve The Long Term Budget ImbalanceДокумент12 страницEconomic Impacts of Waiting To Resolve The Long Term Budget ImbalanceMilton RechtОценок пока нет

- Budget 2021-22Документ57 страницBudget 2021-22sathsihОценок пока нет

- 2014-2015 City of Sacramento Budget OverviewДокумент34 страницы2014-2015 City of Sacramento Budget OverviewCapital Public RadioОценок пока нет

- PDF TestДокумент9 страницPDF TestPhillip EllisОценок пока нет

- Analysis of CBO's August 2011 Baseline and Update of CRFB Realistic Baseline August 24, 2011Документ6 страницAnalysis of CBO's August 2011 Baseline and Update of CRFB Realistic Baseline August 24, 2011Committee For a Responsible Federal BudgetОценок пока нет

- Fy 2013 July UpdateДокумент281 страницаFy 2013 July UpdateNick ReismanОценок пока нет

- Congressional Budget Office: Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Документ25 страницCongressional Budget Office: Douglas W. Elmendorf, Director U.S. Congress Washington, DC 20515Zim VicomОценок пока нет

- Addressing The Long-Run Budget Deficit - A Comparison of Approaches - August 25, 2011 - (CRS)Документ38 страницAddressing The Long-Run Budget Deficit - A Comparison of Approaches - August 25, 2011 - (CRS)QuantDev-MОценок пока нет

- Enacted Budget Report 2020-21Документ22 страницыEnacted Budget Report 2020-21Luke ParsnowОценок пока нет

- Introduction To The Historical Tables: Structure, Coverage, and ConceptsДокумент25 страницIntroduction To The Historical Tables: Structure, Coverage, and ConceptsimplyingnopeОценок пока нет

- WA Senate Proposed Operating BudgetДокумент34 страницыWA Senate Proposed Operating BudgetKING 5 NewsОценок пока нет

- Eroding Our Foundation: Sequestration, R&D, Innovation and U.S. Economic GrowthДокумент34 страницыEroding Our Foundation: Sequestration, R&D, Innovation and U.S. Economic GrowthAlex FitzpatrickОценок пока нет

- Budget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018От EverandBudget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018Оценок пока нет

- Strengthening Fiscal Decentralization in Nepal’s Transition to FederalismОт EverandStrengthening Fiscal Decentralization in Nepal’s Transition to FederalismОценок пока нет

- The Debt Ceiling Dilemma: Balancing Act of Politics, Policy, and FinanceОт EverandThe Debt Ceiling Dilemma: Balancing Act of Politics, Policy, and FinanceОценок пока нет

- The Federal Budget Process, 2E: A Description of the Federal and Congressional Budget Processes, Including TimelinesОт EverandThe Federal Budget Process, 2E: A Description of the Federal and Congressional Budget Processes, Including TimelinesОценок пока нет

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesОт EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesОценок пока нет

- Implementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesОт EverandImplementing Results-Based Budget Management Frameworks: An Assessment of Progress in Selected CountriesОценок пока нет

- Wiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsОт EverandWiley GAAP for Governments 2012: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsОценок пока нет

- Procurement and Supply Chain Management: Emerging Concepts, Strategies and ChallengesОт EverandProcurement and Supply Chain Management: Emerging Concepts, Strategies and ChallengesОценок пока нет

- Greenlight Capital Open Letter To AppleДокумент5 страницGreenlight Capital Open Letter To AppleZim VicomОценок пока нет

- President Barack Obama Deficit Reduction PlanДокумент80 страницPresident Barack Obama Deficit Reduction PlanZim VicomОценок пока нет

- What Putin Has To Say To Americans About SyriaДокумент3 страницыWhat Putin Has To Say To Americans About SyriaZim VicomОценок пока нет

- Avokado - Authentic Guacamole - Brochure English VersionДокумент5 страницAvokado - Authentic Guacamole - Brochure English VersionZim VicomОценок пока нет

- America Invents Act 2011 - Leahy-SmithДокумент58 страницAmerica Invents Act 2011 - Leahy-SmithZim VicomОценок пока нет

- Presidential Memorandum Infrastructure Development - (Environmental and Permitting)Документ4 страницыPresidential Memorandum Infrastructure Development - (Environmental and Permitting)Zim VicomОценок пока нет

- Governor Rick Perry - Cut Balance and Grow - Full Economic and Tax PlanДокумент24 страницыGovernor Rick Perry - Cut Balance and Grow - Full Economic and Tax PlanZim VicomОценок пока нет

- Supplemental Poverty Measure - USA - Census Bureau - November 2011 - 1 in 3 People in America Are Either Poor or in Near Poverty StatusДокумент24 страницыSupplemental Poverty Measure - USA - Census Bureau - November 2011 - 1 in 3 People in America Are Either Poor or in Near Poverty StatusZim VicomОценок пока нет

- Kr8: IAEA Iran 8nov2011Документ25 страницKr8: IAEA Iran 8nov2011shaulcОценок пока нет

- President Barack Obama 14 Infrastructure Projects Approved For Expedited ProcessДокумент7 страницPresident Barack Obama 14 Infrastructure Projects Approved For Expedited ProcessZim VicomОценок пока нет

- Mitt Romney - Believe in America - Plan For Jobs and Economic GrowthДокумент87 страницMitt Romney - Believe in America - Plan For Jobs and Economic GrowthZim VicomОценок пока нет

- The American Jobs Act - President Barack Obama Plan Delivered in Joint Session of Congress - September 8th 2011Документ3 страницыThe American Jobs Act - President Barack Obama Plan Delivered in Joint Session of Congress - September 8th 2011Zim VicomОценок пока нет

- Rick Perry's Tax FormДокумент1 страницаRick Perry's Tax FormThe State NewspaperОценок пока нет

- President Obama and President Lee of The Republic of Korea in A Joint Press ConferenceДокумент12 страницPresident Obama and President Lee of The Republic of Korea in A Joint Press ConferenceZim VicomОценок пока нет

- Troops and Vets Can Still File For Stop Loss PayДокумент2 страницыTroops and Vets Can Still File For Stop Loss PayZim VicomОценок пока нет

- The Open Government Partnership - US National Action PlanДокумент10 страницThe Open Government Partnership - US National Action PlanZim VicomОценок пока нет

- IMF Mexico Full Economic Status ReportДокумент56 страницIMF Mexico Full Economic Status ReportZim VicomОценок пока нет

- 11th Circuit OpinionДокумент304 страницы11th Circuit OpinionCatherine SnowОценок пока нет

- New EPA Fuel Economy Standards For Trucks (Medium and Heavy) - The White HouseДокумент9 страницNew EPA Fuel Economy Standards For Trucks (Medium and Heavy) - The White HouseZim VicomОценок пока нет

- IMF Mexico's Economic Indicators Versus USA's Economic IndicatorsДокумент2 страницыIMF Mexico's Economic Indicators Versus USA's Economic IndicatorsZim VicomОценок пока нет

- The American Jobs ActДокумент6 страницThe American Jobs ActZim VicomОценок пока нет

- EPA Final Regulatory Impact Analysis - Medium and Heavy TrucksДокумент552 страницыEPA Final Regulatory Impact Analysis - Medium and Heavy TrucksZim VicomОценок пока нет

- Sovereign Government Rating Methodology and Assumptions PDFДокумент43 страницыSovereign Government Rating Methodology and Assumptions PDFOmkar BibikarОценок пока нет

- Standard and Poor's USA Downgrade Full Report (From AAA To AA+)Документ8 страницStandard and Poor's USA Downgrade Full Report (From AAA To AA+)Zim VicomОценок пока нет

- CBO Analysis of Budget Control ActДокумент11 страницCBO Analysis of Budget Control ActBrian AhierОценок пока нет

- Budget Control Act of 2011 (Debt Ceiling Bill) As Approved by The House of RepresentativesДокумент58 страницBudget Control Act of 2011 (Debt Ceiling Bill) As Approved by The House of RepresentativesZim VicomОценок пока нет

- House Speaker Boehner Power Point On Debt Ceiling DealДокумент7 страницHouse Speaker Boehner Power Point On Debt Ceiling DealZim VicomОценок пока нет

- Executive Order - Blocking Property of Transnational Criminal OrganizationsДокумент4 страницыExecutive Order - Blocking Property of Transnational Criminal OrganizationsZim VicomОценок пока нет

- Ahtasham Ahmed Case - CompressedДокумент19 страницAhtasham Ahmed Case - CompressedarsssyОценок пока нет

- IRS Form 4506-TДокумент2 страницыIRS Form 4506-TJulie Payne-King100% (2)

- File Your 2019 Federal Tax Return by April 15Документ7 страницFile Your 2019 Federal Tax Return by April 15Kevin Osorio100% (2)

- 2016 California Resident Income Tax Return Form 540 2ezДокумент4 страницы2016 California Resident Income Tax Return Form 540 2ezapi-354477702Оценок пока нет

- 2021 W-2 and Earnings SummaryДокумент2 страницы2021 W-2 and Earnings SummaryKawljeet Singh KohliОценок пока нет

- Pro SourceДокумент18 страницPro Sourcejenny100% (2)

- PIT - IT1040 StateДокумент4 страницыPIT - IT1040 StateLisa GibsonОценок пока нет

- IRSDoc6209 2003Документ665 страницIRSDoc6209 2003EheyehAsherEheyehОценок пока нет

- W 2Документ1 страницаW 2Raj SharmaОценок пока нет

- 6) What Are The Allowable Deductions From Gross Income?: Personal ExemptionsДокумент2 страницы6) What Are The Allowable Deductions From Gross Income?: Personal ExemptionsDeopito BarrettОценок пока нет

- Tax and investment documents for 2020Документ14 страницTax and investment documents for 2020Pete MulardОценок пока нет

- MO-1040A Fillable Calculating - 2015 PDFДокумент3 страницыMO-1040A Fillable Calculating - 2015 PDFAnonymous 3RVba19mОценок пока нет

- f1098t PDFДокумент6 страницf1098t PDFashley valdiviaОценок пока нет

- Home TestДокумент22 страницыHome TestSelina ChenОценок пока нет

- Earnings StatementДокумент2 страницыEarnings StatementRielzaruxo Ka Rioelzarux Ko XОценок пока нет

- Act ch10 l04 EnglishДокумент7 страницAct ch10 l04 EnglishLinds Rivera100% (1)

- 2020 CBO IRS Enforcement ReportДокумент40 страниц2020 CBO IRS Enforcement ReportStephen LoiaconiОценок пока нет

- U.S. Individual Income Tax ReturnДокумент2 страницыU.S. Individual Income Tax Returnapi-310622354Оценок пока нет

- Drake State Refund As Taxable Worksheet (2018)Документ1 страницаDrake State Refund As Taxable Worksheet (2018)TaxGuyОценок пока нет

- WOTCДокумент2 страницыWOTCSa MiОценок пока нет

- IRS Publication Form 8919Документ2 страницыIRS Publication Form 8919Francis Wolfgang UrbanОценок пока нет

- Official Authorization List DocumentsДокумент3 страницыOfficial Authorization List DocumentsJohn WallaceОценок пока нет

- Response To Dishonor of ProcessДокумент2 страницыResponse To Dishonor of ProcessMikeDouglas100% (1)