Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- BondsДокумент12 страницBondsSai Hari Haran100% (1)

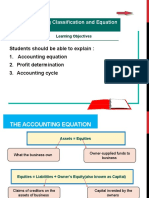

- Week 2 Accounting EquationДокумент19 страницWeek 2 Accounting EquationNor LailyОценок пока нет

- Hidayatullah National Law University: Mortgage and Its Various TypesДокумент16 страницHidayatullah National Law University: Mortgage and Its Various TypesSirshenduОценок пока нет

- Fixed IncomeДокумент213 страницFixed IncomeMia Cristiana100% (1)

- Debt Securities MarketДокумент21 страницаDebt Securities MarketILOVE MATURED FANSОценок пока нет

- First Summative Test in Business Mathematics (2 Quarter) : Department of EducationДокумент7 страницFirst Summative Test in Business Mathematics (2 Quarter) : Department of Educationerica de guzmanОценок пока нет

- Contract of GuaranteeДокумент15 страницContract of GuaranteeRishab Jain 2027203Оценок пока нет

- ACCTGДокумент11 страницACCTGCharles Andrew BaguioОценок пока нет

- Bond ValuationДокумент35 страницBond ValuationCOC AbirОценок пока нет

- 411 Locals: Fees Owed Due Date Inv. Amount BalanceДокумент1 страница411 Locals: Fees Owed Due Date Inv. Amount BalanceAnonymous HRa6knCfrgОценок пока нет

- Time Value of MoneyДокумент10 страницTime Value of MoneyAbasi masoudОценок пока нет

- Deloitte CH en Audit Lease Modifications Extending The Lease TermДокумент25 страницDeloitte CH en Audit Lease Modifications Extending The Lease TermnanaОценок пока нет

- EMI CalculatorДокумент7 страницEMI Calculatorarunasagar_2011Оценок пока нет

- Tugas P17-8 - AKLДокумент15 страницTugas P17-8 - AKLNovie AriyantiОценок пока нет

- 3 M3286 FinДокумент21 страница3 M3286 FinSuramase AutОценок пока нет

- Dungannon Enterprises LTD Sells A Specialty Part That Is Used PDFДокумент1 страницаDungannon Enterprises LTD Sells A Specialty Part That Is Used PDFTaimur TechnologistОценок пока нет

- XXX-XX-0934: Daniels 9 1957Документ7 страницXXX-XX-0934: Daniels 9 1957luis gonzalezОценок пока нет

- What Is A MortgageДокумент7 страницWhat Is A MortgageMessi TanejaОценок пока нет

- Audit of Cash - Exercise 2 (Solution)Документ5 страницAudit of Cash - Exercise 2 (Solution)Aby ReedОценок пока нет

- The Financial Crisis of 2008: What Happened in Simple TermsДокумент2 страницыThe Financial Crisis of 2008: What Happened in Simple TermsBig ALОценок пока нет

- Credit AbejarДокумент2 страницыCredit AbejarGerwin AbejarОценок пока нет

- Chapter 5 - Managing The Credit RiskДокумент18 страницChapter 5 - Managing The Credit RiskWill De OcampoОценок пока нет

- OMLP2P Loan - Peer To Peer Lending India - Online Money LendingДокумент6 страницOMLP2P Loan - Peer To Peer Lending India - Online Money LendingOMLP2P.comОценок пока нет

- Chapter-4: Fixed Income SecuritiesДокумент52 страницыChapter-4: Fixed Income SecuritiesNati YalewОценок пока нет

- Debt RatioДокумент10 страницDebt RatioHera WhitecrownОценок пока нет

- My PuhunanДокумент2 страницыMy PuhunanJaymart de VillaОценок пока нет

- Solution:: Problem 4: For Classroom DiscussionДокумент2 страницыSolution:: Problem 4: For Classroom DiscussionAnika Gaudan PonoОценок пока нет

- Amortization & Sinking FundДокумент2 страницыAmortization & Sinking FundAaronUyОценок пока нет

- ACCO 30103 CORPLIQ-Statement of Affairs and Deficiency Statement 04-2022Документ3 страницыACCO 30103 CORPLIQ-Statement of Affairs and Deficiency Statement 04-2022Zyrille Corrine GironОценок пока нет

- Accounting 4 Note Payable and Debt RestructureДокумент2 страницыAccounting 4 Note Payable and Debt RestructurelorenОценок пока нет