Вам также может понравиться

- Business Math Module 7Документ5 страницBusiness Math Module 7CJ WATTPADОценок пока нет

- Business Mathematics: Business Applications of Fractions, Decimals, and PercentsДокумент16 страницBusiness Mathematics: Business Applications of Fractions, Decimals, and PercentsChantal AltheaОценок пока нет

- Business Math Module 11Документ9 страницBusiness Math Module 11James Earl AbainzaОценок пока нет

- RATIO COMPARISONS AND APPLICATIONSДокумент21 страницаRATIO COMPARISONS AND APPLICATIONSLevi Corral0% (1)

- Bataan National High School Activity SheetsДокумент10 страницBataan National High School Activity SheetsChristine Kayela Marquez CanareОценок пока нет

- Solving Real-Life Problems with Fractions, Decimals & PercentagesДокумент11 страницSolving Real-Life Problems with Fractions, Decimals & PercentagesFlordilyn DichonОценок пока нет

- Understanding the difference between markup and marginДокумент18 страницUnderstanding the difference between markup and marginCaryl GalocgocОценок пока нет

- Principles of Mrktg. - Q3 Module 7Документ11 страницPrinciples of Mrktg. - Q3 Module 7Marilyn TamayoОценок пока нет

- Lesson 2 Wk10 4th Fundamental Operations of Mathematics As Applied in Salaries and Wages StudentДокумент11 страницLesson 2 Wk10 4th Fundamental Operations of Mathematics As Applied in Salaries and Wages StudentFrancine Arielle Bernales100% (1)

- Business Mathematics: Quarter 1 - Module 5 Markup, Markdown, and Mark-OnДокумент27 страницBusiness Mathematics: Quarter 1 - Module 5 Markup, Markdown, and Mark-OnAthena KleahОценок пока нет

- 1Q BM 3rd Module A.Y. 2021 - 2022Документ20 страниц1Q BM 3rd Module A.Y. 2021 - 2022Jewel RamosОценок пока нет

- LM Busmath q2 Module 2 Wk2 CasillaДокумент30 страницLM Busmath q2 Module 2 Wk2 CasillaDonna CasillaОценок пока нет

- Key Concepts of Commissions ExplainedДокумент11 страницKey Concepts of Commissions ExplainedDearla BitoonОценок пока нет

- Activity Sheet: Solving A Problems Involving Fractions, Decimals and PercentДокумент18 страницActivity Sheet: Solving A Problems Involving Fractions, Decimals and PercentJo Ash BiongОценок пока нет

- Accounting Equation Lesson 1.1Документ23 страницыAccounting Equation Lesson 1.1Renz RaphОценок пока нет

- Business Math - Q2 - M3Документ12 страницBusiness Math - Q2 - M3Real GurayОценок пока нет

- Module 3 in Business MathДокумент12 страницModule 3 in Business MathJiro DomantayОценок пока нет

- Business Mathematics - Module 3 - Ratio Rates and ProportionsДокумент18 страницBusiness Mathematics - Module 3 - Ratio Rates and ProportionsRenmel Joseph PurisimaОценок пока нет

- Bus Math Week 3 Q2Документ5 страницBus Math Week 3 Q2Trixine BrozasОценок пока нет

- Chapter V. Types of Business According To ActivitiesДокумент1 страницаChapter V. Types of Business According To Activitiesmarissa casareno almueteОценок пока нет

- BusinessMath LAS Q1 Wk3Документ10 страницBusinessMath LAS Q1 Wk3Janna GunioОценок пока нет

- Businessfinance12 - q3 - Mod6.2 - Basic Long Term Financial Concepts - Loan AmortizationДокумент22 страницыBusinessfinance12 - q3 - Mod6.2 - Basic Long Term Financial Concepts - Loan AmortizationBernadette MendozaОценок пока нет

- Most Essential Learning Competency: National Capital Region SchoolsdivisionofficeoflaspiñascityДокумент3 страницыMost Essential Learning Competency: National Capital Region SchoolsdivisionofficeoflaspiñascityJessel CarilloОценок пока нет

- Business Mathematics: Specialized Subject - ABMДокумент12 страницBusiness Mathematics: Specialized Subject - ABMemmalou shane fernandezОценок пока нет

- Business Finance: Roles of Financial ManagersДокумент12 страницBusiness Finance: Roles of Financial ManagersAngelica ParasОценок пока нет

- FABM1 Q4 M1 Preparing-Adjusting-EntriesДокумент14 страницFABM1 Q4 M1 Preparing-Adjusting-EntriesXedric JuantaОценок пока нет

- ABM11 Business Math Q1 W1 MODULE1Документ13 страницABM11 Business Math Q1 W1 MODULE1Ian BoneoОценок пока нет

- Learning Activity Sheets: Business MathematicsДокумент4 страницыLearning Activity Sheets: Business MathematicsKimberly Lagman100% (1)

- ShareholdersThe ___________ oversees the day-to-day operations of the company. He/She is also the chief decision makerДокумент16 страницShareholdersThe ___________ oversees the day-to-day operations of the company. He/She is also the chief decision makerKinn Jay100% (1)

- Business Math Q2 FinalsДокумент4 страницыBusiness Math Q2 FinalsZeus MalicdemОценок пока нет

- Business Mathematics Key Concepts of Ratio and Proportion: Quarter 1 Week 3 Module 3Документ13 страницBusiness Mathematics Key Concepts of Ratio and Proportion: Quarter 1 Week 3 Module 3thea delimaОценок пока нет

- Learners Packet Business MathДокумент26 страницLearners Packet Business MathRed TulaoОценок пока нет

- Business Math Quarter 3 Week 3Документ7 страницBusiness Math Quarter 3 Week 3Gladys Angela ValdemoroОценок пока нет

- BUSINESS MATH MODULE 4A For MANDAUE CITY DIVISIONДокумент14 страницBUSINESS MATH MODULE 4A For MANDAUE CITY DIVISIONJASON DAVID AMARILAОценок пока нет

- STATEMENT OF COMPREHENSIVE INCOME Preparing Single-Step SCI for Service BusinessДокумент6 страницSTATEMENT OF COMPREHENSIVE INCOME Preparing Single-Step SCI for Service BusinessJUDITH PIANOОценок пока нет

- Insights into the complex relationship between Malinalli and CortesДокумент5 страницInsights into the complex relationship between Malinalli and Cortesbangtanswifue -Оценок пока нет

- Bus. Math Q2 - W1&W2Документ7 страницBus. Math Q2 - W1&W2DARLENE MARTINОценок пока нет

- Financial Statement Analysis: Lesson 5.2Документ29 страницFinancial Statement Analysis: Lesson 5.2Rein BalicogОценок пока нет

- BusinessMath Q4 Ver4 Mod3Документ39 страницBusinessMath Q4 Ver4 Mod3Isnihaya AbubacarОценок пока нет

- Week 4 - Module (Trade Discount)Документ8 страницWeek 4 - Module (Trade Discount)Angelica perezОценок пока нет

- FABM 2 - Review of Journal Entries, T-Accounts, General Ledger and Trial BalanceДокумент13 страницFABM 2 - Review of Journal Entries, T-Accounts, General Ledger and Trial BalanceKim Patrick Victoria0% (1)

- Fractions, Decimals, Percents: Learners Module in Business MathematicsДокумент29 страницFractions, Decimals, Percents: Learners Module in Business MathematicsJamaica C. AquinoОценок пока нет

- ABM11 BussMath Q1 Wk3 ProportionsДокумент12 страницABM11 BussMath Q1 Wk3 ProportionsArchimedes Arvie Garcia100% (1)

- RATIOДокумент3 страницыRATIOmejoy marbidaОценок пока нет

- Marketing q2 Mod4 PromotionДокумент25 страницMarketing q2 Mod4 PromotionChrissalyn BuizonОценок пока нет

- 07 Abm 11 Pasay Busmath q2 w1Документ24 страницы07 Abm 11 Pasay Busmath q2 w1Jay Kenneth BaldoОценок пока нет

- Q3 Fundamentals of ABM 1 Module 3Документ22 страницыQ3 Fundamentals of ABM 1 Module 3Krisha FernandezОценок пока нет

- Business Mathematics Chapter 2 Ratio and Proportion Lesson in 1st Quarter 4th WeekДокумент18 страницBusiness Mathematics Chapter 2 Ratio and Proportion Lesson in 1st Quarter 4th WeekDearla BitoonОценок пока нет

- 1st Quater ExamДокумент3 страницы1st Quater ExamRedaw BandilanОценок пока нет

- Compound Interest: Learning Module in Applied Mathematics of InvestmentДокумент11 страницCompound Interest: Learning Module in Applied Mathematics of InvestmentiamamayОценок пока нет

- Business Mathematics Module 7 Profit and LossДокумент16 страницBusiness Mathematics Module 7 Profit and LossDavid DueОценок пока нет

- Basic Long-Term Financial ConceptsДокумент30 страницBasic Long-Term Financial ConceptsJanna GunioОценок пока нет

- Business Math M2 & M3Документ24 страницыBusiness Math M2 & M3Real GurayОценок пока нет

- Marketing Principles ExplainedДокумент20 страницMarketing Principles ExplainedGeraldine EctanaОценок пока нет

- MotionДокумент8 страницMotionKaren Anne Briones RufinoОценок пока нет

- Business Math - 2nd Semeter ModuleДокумент44 страницыBusiness Math - 2nd Semeter ModuleChristian Luis De GuzmanОценок пока нет

- Simple InterestДокумент13 страницSimple InterestBridget Anne BenitezОценок пока нет

- GenMath11 Q2 Mod3oknaprinted NaДокумент19 страницGenMath11 Q2 Mod3oknaprinted NaLarilyn BenictaОценок пока нет

- Handout Mathematics of Investment PDFДокумент36 страницHandout Mathematics of Investment PDFJhon Carlo Delmonte100% (6)

- EstimationДокумент27 страницEstimationmonch1998Оценок пока нет

- Animals Module: Classification, Life Cycles, CareersДокумент52 страницыAnimals Module: Classification, Life Cycles, CareersMaam PreiОценок пока нет

- Fire Safety in The HomeДокумент46 страницFire Safety in The Homemonch1998Оценок пока нет

- Environmental Causes of DiseasesДокумент50 страницEnvironmental Causes of Diseasesmonch1998Оценок пока нет

- Advances in Communication TechnologyДокумент23 страницыAdvances in Communication Technologymonch1998Оценок пока нет

- Balance in NatureДокумент53 страницыBalance in Naturemonch1998Оценок пока нет

- Developing Scientific Thinking SkillsДокумент29 страницDeveloping Scientific Thinking Skillsmonch1998100% (1)

- Effects of VolcanoesДокумент38 страницEffects of Volcanoesmonch1998Оценок пока нет

- EarthquakeДокумент44 страницыEarthquakemonch1998Оценок пока нет

- Aquatic and Man Made EcosystemДокумент43 страницыAquatic and Man Made Ecosystemmonch1998Оценок пока нет

- CompostingДокумент44 страницыCompostingmonch1998Оценок пока нет

- Addictive and Dangerous Drug Part 2Документ48 страницAddictive and Dangerous Drug Part 2monch1998Оценок пока нет

- What Is This Module About?: What Would Life Be Without Plants? and Think GreenДокумент52 страницыWhat Is This Module About?: What Would Life Be Without Plants? and Think Greennageen198475% (4)

- Appreciating StatisticsДокумент38 страницAppreciating Statisticsmonch1998Оценок пока нет

- AreaДокумент44 страницыAreamonch1998Оценок пока нет

- Business Math 2Документ46 страницBusiness Math 2joel alanoОценок пока нет

- The Notion of Development: As Seen From Caritas in Veritate - Notes For Chapter 1 and 2Документ15 страницThe Notion of Development: As Seen From Caritas in Veritate - Notes For Chapter 1 and 2monch1998Оценок пока нет

- Advances in Communication TechnologyДокумент23 страницыAdvances in Communication Technologymonch1998Оценок пока нет

- The Development of People, Rights and Duties, The EnvironmentДокумент7 страницThe Development of People, Rights and Duties, The Environmentmonch1998Оценок пока нет

- The Organ System of The Human BodyДокумент45 страницThe Organ System of The Human Bodymonch1998100% (3)

- Addictive and Dangerous Drug Part 1Документ53 страницыAddictive and Dangerous Drug Part 1monch1998Оценок пока нет

- Human Development in Our TimeДокумент12 страницHuman Development in Our Timemonch1998Оценок пока нет

- Spirituality of WorkДокумент14 страницSpirituality of Workmonch1998Оценок пока нет

- The Message of Populorum ProgressioДокумент13 страницThe Message of Populorum Progressiomonch1998Оценок пока нет

- Assignment AccДокумент47 страницAssignment Acchakimstars2003Оценок пока нет

- Economic Growth (Mankiw) PDFДокумент69 страницEconomic Growth (Mankiw) PDFaminul akashОценок пока нет

- AGREEMEN1Документ56 страницAGREEMEN1Elah De LeonОценок пока нет

- DRC-Uganda Cross-Border Road ProjectsДокумент28 страницDRC-Uganda Cross-Border Road ProjectsasdasdОценок пока нет

- CRM 4Документ25 страницCRM 4Zankhana BhosleОценок пока нет

- Drycargo 05-2019Документ134 страницыDrycargo 05-2019fracev100% (1)

- Earthwear Hands-On Mini-Case: Chapter 3 - Materiality and Tolerable MisstatementДокумент8 страницEarthwear Hands-On Mini-Case: Chapter 3 - Materiality and Tolerable MisstatementRuany LisbethОценок пока нет

- Statement 517000057 86377450 17 07 2023 17 09 2023Документ6 страницStatement 517000057 86377450 17 07 2023 17 09 2023katsergey12Оценок пока нет

- Narita Express Press - 20220304 - Nex - eДокумент2 страницыNarita Express Press - 20220304 - Nex - eJames ChoongОценок пока нет

- Objectives of Planning in India (BYJUS)Документ1 страницаObjectives of Planning in India (BYJUS)C. MittalОценок пока нет

- Marginal Cost Questions - Past ExamДокумент3 страницыMarginal Cost Questions - Past ExamLouisa HasfordОценок пока нет

- Signature Global BlogДокумент2 страницыSignature Global BlogOmkar kumarОценок пока нет

- Class 9 Economics Chapter 2 Ncert NotesДокумент2 страницыClass 9 Economics Chapter 2 Ncert NoteshariharanrevathyОценок пока нет

- Toyota Operations Management As A Competitive AdvantageДокумент8 страницToyota Operations Management As A Competitive AdvantageGodman KipngenoОценок пока нет

- Impact of MacroeconomicsДокумент5 страницImpact of MacroeconomicsChetan ChanneОценок пока нет

- Grade 11 UcspДокумент4 страницыGrade 11 Ucspmarlon anzanoОценок пока нет

- Bollinger Bands Essentials 1Документ13 страницBollinger Bands Essentials 1Kiran KudtarkarОценок пока нет

- The Avoidable War - Full ReportДокумент89 страницThe Avoidable War - Full ReportAkshat TennetiОценок пока нет

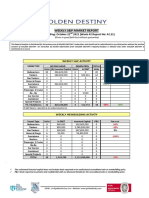

- Weekly S&P and Newbuilding Market Report SummaryДокумент7 страницWeekly S&P and Newbuilding Market Report SummarySandesh Tukaram GhandatОценок пока нет

- Why Growth Can't Be Green - Jason HickelДокумент6 страницWhy Growth Can't Be Green - Jason HickelIsabela Prado - PeritaОценок пока нет

- To Get More Videos of All Subjects: ShareДокумент50 страницTo Get More Videos of All Subjects: ShareMridul UpadhyayОценок пока нет

- Lecture 2 Notes IДокумент23 страницыLecture 2 Notes I林靖雯Оценок пока нет

- Annual Program Agric Advisory and Services Unit FOR YEAR 2021Документ15 страницAnnual Program Agric Advisory and Services Unit FOR YEAR 2021Rose Asman Samsul BahrinОценок пока нет

- Choose A Forex BrokerДокумент1 страницаChoose A Forex BrokerMed MesОценок пока нет

- Who Owns Indonesia's Deadly Abandoned Coal Mines?Документ12 страницWho Owns Indonesia's Deadly Abandoned Coal Mines?Erick CalvinОценок пока нет

- Lesson 1 - Contemporary World: Why Do You Need To Study The World?Документ23 страницыLesson 1 - Contemporary World: Why Do You Need To Study The World?RachelleОценок пока нет

- Iare Birm Lecture NotesДокумент188 страницIare Birm Lecture NotesSumit Kumar GautamОценок пока нет

- PolestarДокумент2 страницыPolestarHusseinОценок пока нет

- DISMANTLING AND PACKING OF GE Fr.9E Gas Turbine Plant - Eng ProposalДокумент6 страницDISMANTLING AND PACKING OF GE Fr.9E Gas Turbine Plant - Eng Proposalvarun100% (1)

- Consulting 101Документ16 страницConsulting 101Aniek de Vroome0% (1)