Вам также может понравиться

- 1Документ40 страниц1Ehab AgwaОценок пока нет

- Visvanathan 2017Документ10 страницVisvanathan 2017Ehab AgwaОценок пока нет

- PropДокумент74 страницыPropEhab AgwaОценок пока нет

- Principles-Versus Rules-Based Accounting Standards: The FASB's Standard Setting StrategyДокумент24 страницыPrinciples-Versus Rules-Based Accounting Standards: The FASB's Standard Setting StrategyEhab AgwaОценок пока нет

- Discussion of "The Effect On Financial Reporting Quality of An Exemption From The SEC Reporting Requirements For Foreign Private Issuers "Документ4 страницыDiscussion of "The Effect On Financial Reporting Quality of An Exemption From The SEC Reporting Requirements For Foreign Private Issuers "Ehab AgwaОценок пока нет

- Measurement in Financial Reporting PDFДокумент84 страницыMeasurement in Financial Reporting PDFEhab AgwaОценок пока нет

- DP ITC Disclosure FrameworkДокумент81 страницаDP ITC Disclosure FrameworkEhab AgwaОценок пока нет

- Financial Management - EVA PDFДокумент28 страницFinancial Management - EVA PDFBhoopal PadmanabhanОценок пока нет

- Science 30Документ2 страницыScience 30Ehab AgwaОценок пока нет

- 2.7. Du BoisДокумент23 страницы2.7. Du BoisAvneet SethiОценок пока нет

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Casus Omissus Pro Omisso Habendus Est - A Person, Object, or Thing Omitted FromДокумент3 страницыCasus Omissus Pro Omisso Habendus Est - A Person, Object, or Thing Omitted FromCP LugoОценок пока нет

- Credit Card VS Debit CardДокумент3 страницыCredit Card VS Debit CardS K MahapatraОценок пока нет

- M1 Post-Task Essay On The History of GlobalizationДокумент2 страницыM1 Post-Task Essay On The History of GlobalizationJean SantosОценок пока нет

- SegmentationДокумент5 страницSegmentationChahatBhattiAli75% (4)

- Chapter 1 - Cost Accounting FundamentalsДокумент16 страницChapter 1 - Cost Accounting FundamentalsPrincess Jay NacorОценок пока нет

- Journal of Financial Economics: Progress PaperДокумент17 страницJournal of Financial Economics: Progress PapersaidОценок пока нет

- MonopolyДокумент19 страницMonopolyJames BondОценок пока нет

- Labourindindustrial 1 1Документ148 страницLabourindindustrial 1 1Brian ChegeОценок пока нет

- 6 Operations ImprovementДокумент30 страниц6 Operations ImprovementAnushaBalasubramanya100% (1)

- Session 2 Reasons of Wins On Losses in SalesДокумент5 страницSession 2 Reasons of Wins On Losses in SalesAritra BanerjeeОценок пока нет

- ICGAB Prospectus PDFДокумент11 страницICGAB Prospectus PDFSyed Fazle ImamОценок пока нет

- Financial Controller 1 Pre-Final QuestionsДокумент2 страницыFinancial Controller 1 Pre-Final QuestionsWen CapunoОценок пока нет

- 001 FundamentalsДокумент30 страниц001 FundamentalsTutuch NidonatoОценок пока нет

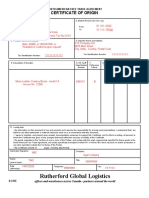

- Rutherford Global Logistics: Certificate of OriginДокумент1 страницаRutherford Global Logistics: Certificate of OriginAnkita SinhaОценок пока нет

- CH 1 EntrepreneurshipДокумент19 страницCH 1 EntrepreneurshipGursahib Singh JauraОценок пока нет

- Managing Small Projects PDFДокумент4 страницыManaging Small Projects PDFJ. ZhouОценок пока нет

- Finance & StrategyДокумент36 страницFinance & StrategySirsanath Banerjee100% (1)

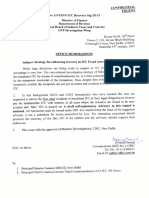

- Advisory For Action Fake Itc Recipients Date 19.1.21Документ2 страницыAdvisory For Action Fake Itc Recipients Date 19.1.21GroupA PreventiveОценок пока нет

- Lic Act 1956Документ18 страницLic Act 1956Anonymous 0cGqn3Оценок пока нет

- PST AAA 2015 2022Документ45 страницPST AAA 2015 2022mulika99Оценок пока нет

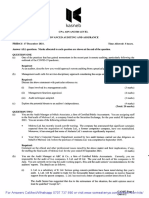

- ACCA Audit and Assurance (AA) - Course Exam 1 - Questions - 2020Документ6 страницACCA Audit and Assurance (AA) - Course Exam 1 - Questions - 2020Karman SyakirОценок пока нет

- 3rd Sem Cost Accounting Apr 2023Документ8 страниц3rd Sem Cost Accounting Apr 2023Chandan GОценок пока нет

- Four Green Houses... One Red HotelДокумент325 страницFour Green Houses... One Red HotelDhruv Thakkar100% (1)

- Can Capitalism Bring Inclusive Growth?: - Suneel SheoranДокумент4 страницыCan Capitalism Bring Inclusive Growth?: - Suneel SheoranSandeepkumar SgОценок пока нет

- Ümmüşnur Özcan - CartwrightlumberworksheetДокумент7 страницÜmmüşnur Özcan - CartwrightlumberworksheetUMMUSNUR OZCANОценок пока нет

- Chapter 7 - Compound Financial Instrument (FAR6)Документ5 страницChapter 7 - Compound Financial Instrument (FAR6)Honeylet SigesmundoОценок пока нет

- Cryptocurrency and The Future of FinanceДокумент9 страницCryptocurrency and The Future of FinanceJawad NadeemОценок пока нет

- Premium & Warranty LiabilitiesДокумент16 страницPremium & Warranty LiabilitiesKring Zel0% (1)

- Learning Activity 3 - Inc TaxДокумент3 страницыLearning Activity 3 - Inc TaxErica FlorentinoОценок пока нет

- MedMen CFO Lawsuit PDFДокумент48 страницMedMen CFO Lawsuit PDFsandydocs100% (2)