Вам также может понравиться

- Answers: Operating Income Changes in Net Operating AssetsДокумент6 страницAnswers: Operating Income Changes in Net Operating AssetsNawarathna KumariОценок пока нет

- Contemporary Financial Management 10th Edition Moyer Solutions Manual 1Документ15 страницContemporary Financial Management 10th Edition Moyer Solutions Manual 1carlo100% (40)

- Kelompok 5 - Cash Flow - ALKДокумент16 страницKelompok 5 - Cash Flow - ALKSiti Ruhmana SiregarОценок пока нет

- In Class Chap 12 SolutionДокумент15 страницIn Class Chap 12 SolutionDannickОценок пока нет

- CH 12 NotesДокумент23 страницыCH 12 NotesBec barronОценок пока нет

- hw4 (Answers) R2Документ6 страницhw4 (Answers) R2Arslan HafeezОценок пока нет

- Solution Manual For Fundamental Financial Accounting Concepts 7th Edition by EdmondsДокумент9 страницSolution Manual For Fundamental Financial Accounting Concepts 7th Edition by EdmondsDiane Jones100% (26)

- 01 - Exercises Session 1 - EmptyДокумент4 страницы01 - Exercises Session 1 - EmptyAgustín RosalesОценок пока нет

- E5-1B (Similar To E5-6) (LO 3) Preparing and Interpreting A Classified Balance Sheet With Discussion of Terminology (Challenging)Документ4 страницыE5-1B (Similar To E5-6) (LO 3) Preparing and Interpreting A Classified Balance Sheet With Discussion of Terminology (Challenging)Muostapha FikryОценок пока нет

- Practice Exam SOLUTIONS - Vol 2 (2020)Документ49 страницPractice Exam SOLUTIONS - Vol 2 (2020)Ledger PointОценок пока нет

- Last Assignment (Najeeb)Документ7 страницLast Assignment (Najeeb)Najeeb KhanОценок пока нет

- Case 1 Format IdeaДокумент5 страницCase 1 Format IdeaMarina StraderОценок пока нет

- Afif Juwandira-1162003016-Jawaban UTS Semester GenapДокумент10 страницAfif Juwandira-1162003016-Jawaban UTS Semester GenapYusuf AssegafОценок пока нет

- Advanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Документ23 страницыAdvanced Taxation - Solutions To Pilot Questions Suggested Solution To Question 1Oyebisi OpeyemiОценок пока нет

- Nama: Aliea Yenemia Putri NPM: 120110210003 P4-19 A. Randy & Wiskers Enterprises Pro Forma Balance Sheet December 31, 2019 Assets Liabilities and Stockholders' EquityДокумент10 страницNama: Aliea Yenemia Putri NPM: 120110210003 P4-19 A. Randy & Wiskers Enterprises Pro Forma Balance Sheet December 31, 2019 Assets Liabilities and Stockholders' EquityAliea YenemiaОценок пока нет

- 4.3. Example Scenario - Pro Forma ProblemsДокумент6 страниц4.3. Example Scenario - Pro Forma Problemskartik lakhotiyaОценок пока нет

- Fa2 TutorialДокумент59 страницFa2 TutorialNam PhươngОценок пока нет

- Chapter 4-Profitability Analysis: Multiple ChoiceДокумент30 страницChapter 4-Profitability Analysis: Multiple ChoiceRawan NaderОценок пока нет

- 130565353X 540322Документ19 страниц130565353X 540322blackghostОценок пока нет

- Solutions To End-Of-Chapter ProblemsДокумент14 страницSolutions To End-Of-Chapter ProblemsTushar MalhotraОценок пока нет

- 167 A 2Документ3 страницы167 A 2hira malik0% (1)

- Property, Plant, and Equipment Accumulated Depreciation Net Property, Plant, and EquipmentДокумент6 страницProperty, Plant, and Equipment Accumulated Depreciation Net Property, Plant, and EquipmentEman KhalilОценок пока нет

- Chapter 11 PDFДокумент12 страницChapter 11 PDFJay BrockОценок пока нет

- 6th Ed Module 1 Selected Homework AnswersДокумент7 страниц6th Ed Module 1 Selected Homework AnswersjoshОценок пока нет

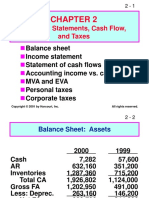

- ch02 Financial Statement, Cash Flows and TaxesДокумент30 страницch02 Financial Statement, Cash Flows and TaxesAffan AhmedОценок пока нет

- Name: Mukarram Ali Siddiqui (18020) Topic: Financial Statements On CorporationДокумент4 страницыName: Mukarram Ali Siddiqui (18020) Topic: Financial Statements On CorporationAreeba NaeemОценок пока нет

- Examination Question and Answers, Set D (Problem Solving), Chapter 15 - Statement of Cash FlowДокумент2 страницыExamination Question and Answers, Set D (Problem Solving), Chapter 15 - Statement of Cash Flowjohn carlos doringoОценок пока нет

- Profits Tax Computation Illustration 2023S - Suggested Answers Ver2Документ2 страницыProfits Tax Computation Illustration 2023S - Suggested Answers Ver2何健珩Оценок пока нет

- Question 44 (65 Minutes) (Chapters 11, 12) : NotesДокумент2 страницыQuestion 44 (65 Minutes) (Chapters 11, 12) : Notesromie2bОценок пока нет

- CMA Part2 EssaysДокумент128 страницCMA Part2 EssaysSandeep Sawan100% (1)

- CH4 MinicaseДокумент4 страницыCH4 Minicasemervin coquillaОценок пока нет

- Practice Solution 2Документ4 страницыPractice Solution 2Luigi NocitaОценок пока нет

- ch04 PDFДокумент5 страницch04 PDFĐào Quốc Anh100% (1)

- IA3 Engaging Activity, PT1 PT2 PT3 & QUIZДокумент8 страницIA3 Engaging Activity, PT1 PT2 PT3 & QUIZKaye Ann Abejuela RamosОценок пока нет

- Department: Banking & Finance Course Title: Business Finance Chapter 3: Financial StatementsДокумент14 страницDepartment: Banking & Finance Course Title: Business Finance Chapter 3: Financial StatementsMhmdОценок пока нет

- CH 4 In-Class ExerciseДокумент4 страницыCH 4 In-Class ExerciseAbdullah alhamaadОценок пока нет

- Solution To P 9-8Документ8 страницSolution To P 9-8Muhammad Iqbal PerwaizОценок пока нет

- Financial Statements, Cash Flow, and TaxesДокумент44 страницыFinancial Statements, Cash Flow, and TaxesJuliani Tania RizkyОценок пока нет

- Financial Statements, Cash Flow, and TaxesДокумент45 страницFinancial Statements, Cash Flow, and TaxesFridolin Belnovando Abditomo PrakosoОценок пока нет

- Financial Statements, Cash Flow, and TaxesДокумент44 страницыFinancial Statements, Cash Flow, and TaxesMahmoud Abdullah100% (1)

- Ch02 ShowДокумент44 страницыCh02 ShowardiОценок пока нет

- Problem 12-10 SolutionДокумент9 страницProblem 12-10 SolutionKELLY DANGОценок пока нет

- Homework Session 1 Caroline Oktaviani - 01619190059 Exercise 1.1Документ3 страницыHomework Session 1 Caroline Oktaviani - 01619190059 Exercise 1.1Caroline OktavianiОценок пока нет

- B205B Financial ExamplesДокумент6 страницB205B Financial ExamplesAhmad RahjeОценок пока нет

- Financial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Test Bank 1Документ36 страницFinancial Reporting Financial Statement Analysis and Valuation 8th Edition Wahlen Test Bank 1ericsuttonybmqwiorsa100% (28)

- Febbinia Dwigna P - Week7 AKL 1Документ5 страницFebbinia Dwigna P - Week7 AKL 1febbiniaОценок пока нет

- Manajemen Keuangan Kelompok CaiaДокумент6 страницManajemen Keuangan Kelompok CaiaintandewiОценок пока нет

- CF MBA S23 Ch2 (B2) QsДокумент6 страницCF MBA S23 Ch2 (B2) QsWaris 3478-FBAS/BSCS/F16Оценок пока нет

- Chapter Thirteen SolutionsДокумент18 страницChapter Thirteen Solutionsapi-3705855Оценок пока нет

- EFM2e, CH 02, SlidesДокумент19 страницEFM2e, CH 02, SlidesEricLiangtoОценок пока нет

- Financial Management Economics For Finance 2023 1671444516Документ36 страницFinancial Management Economics For Finance 2023 1671444516RADHIKAОценок пока нет

- Adjusted Retained Earnings StatementДокумент2 страницыAdjusted Retained Earnings StatementSerazul Arafin MrinmoyОценок пока нет

- Investment Analysis and Portfolio Management 2012Документ61 страницаInvestment Analysis and Portfolio Management 2012Nelson Ivan Acosta100% (1)

- Solution To P3-5: Chapter 8) - When The Shares Are Sold in 2021, When Landry Is A Non-Resident, TheДокумент23 страницыSolution To P3-5: Chapter 8) - When The Shares Are Sold in 2021, When Landry Is A Non-Resident, TheLucyОценок пока нет

- MT Test Review-Taxation 1-Win 2024Документ4 страницыMT Test Review-Taxation 1-Win 2024Mariola AlkuОценок пока нет

- Chapter 16Документ72 страницыChapter 16Sour CandyОценок пока нет

- Module 1, Chapter 1 Handout Introduction To Financial StatementsДокумент5 страницModule 1, Chapter 1 Handout Introduction To Financial StatementssdfsdfuignbcbbdfbОценок пока нет

- Gitman IM Ch03Документ15 страницGitman IM Ch03tarekffОценок пока нет

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsОт EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsОценок пока нет

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineОт EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineОценок пока нет

- Solutions To Exam #1Документ11 страницSolutions To Exam #1api-3705855100% (2)

- Chapter 13Документ1 страницаChapter 13api-3705855Оценок пока нет

- Chapter Sixteen SolutionsДокумент22 страницыChapter Sixteen Solutionsapi-3705855Оценок пока нет

- Chapter 15Документ1 страницаChapter 15api-3705855Оценок пока нет

- Chapter Thirteen SolutionsДокумент18 страницChapter Thirteen Solutionsapi-3705855Оценок пока нет

- Chapter 16Документ1 страницаChapter 16api-3705855Оценок пока нет

- CH 16Документ68 страницCH 16api-3705855Оценок пока нет

- Chapter One SolutionsДокумент9 страницChapter One Solutionsapi-3705855100% (1)

- CorporationsДокумент88 страницCorporationsapi-3705855Оценок пока нет

- CH 18Документ50 страницCH 18api-3705855100% (1)

- CH 19Документ53 страницыCH 19api-3705855Оценок пока нет

- CH 05Документ39 страницCH 05api-3705855Оценок пока нет

- Chapter Two SolutionsДокумент9 страницChapter Two Solutionsapi-3705855Оценок пока нет

- CH 17Документ38 страницCH 17api-3705855Оценок пока нет

- CH 08Документ51 страницаCH 08api-3705855100% (1)

- CH 14Документ52 страницыCH 14api-3705855Оценок пока нет

- CH 15Документ89 страницCH 15api-3705855Оценок пока нет

- CH 10Документ41 страницаCH 10api-3705855Оценок пока нет

- CH 11Документ41 страницаCH 11api-3705855Оценок пока нет

- CH 12Документ39 страницCH 12api-3705855Оценок пока нет

- CH 07Документ41 страницаCH 07api-3705855Оценок пока нет

- CH 06Документ53 страницыCH 06api-3705855Оценок пока нет

- CH 09Документ44 страницыCH 09api-3705855Оценок пока нет

- CH 13Документ40 страницCH 13api-3705855Оценок пока нет

- CH 04Документ27 страницCH 04api-3705855Оценок пока нет

- CH 03Документ25 страницCH 03api-3705855Оценок пока нет

- CH 02Документ34 страницыCH 02api-3705855Оценок пока нет

- Chapter 2Документ1 страницаChapter 2api-3705855Оценок пока нет

- CH 01Документ13 страницCH 01api-3705855Оценок пока нет

- LogoДокумент4 страницыLogoNiti YadavОценок пока нет

- Debonair-Strategic Analysis of No Frills AirlineДокумент8 страницDebonair-Strategic Analysis of No Frills AirlineHarry LondonОценок пока нет

- BA 1201 AssignmentДокумент4 страницыBA 1201 AssignmentJuvy DimaanoОценок пока нет

- Case Study ON Mcdonald'S-Serving Fast Food Around The WorldДокумент10 страницCase Study ON Mcdonald'S-Serving Fast Food Around The WorldJaya SharmaОценок пока нет

- Homework T1. Fin Account - IntroductionДокумент4 страницыHomework T1. Fin Account - IntroductionCrayZeeAlexОценок пока нет

- BF Readingtxt02 PDFДокумент2 страницыBF Readingtxt02 PDFRoberta MarcheseОценок пока нет

- E-Mail - Bo3900@pnb - Co.in: Punjab National Bank International Banking Division Head Office:New Delhi Page 1 of 12Документ12 страницE-Mail - Bo3900@pnb - Co.in: Punjab National Bank International Banking Division Head Office:New Delhi Page 1 of 12kirpaldoadОценок пока нет

- Labor Full 2.1 - Art120-129Документ43 страницыLabor Full 2.1 - Art120-129kat78904Оценок пока нет

- Case Study 18 PresentationДокумент11 страницCase Study 18 PresentationZara KhanОценок пока нет

- Motion To Sell Adak PlantДокумент12 страницMotion To Sell Adak PlantDeckbossОценок пока нет

- Lehman Bankruptcy DocketДокумент2 480 страницLehman Bankruptcy Docketpowda1120Оценок пока нет

- Form10 KДокумент12 страницForm10 Ksl7789Оценок пока нет

- Pre Incorporation Contracts - SynopsisДокумент3 страницыPre Incorporation Contracts - SynopsisRavindran VairamoorthyОценок пока нет

- Walmart and Its Strategy in Different CulturesДокумент5 страницWalmart and Its Strategy in Different Culturessan33045Оценок пока нет

- Venture Capital Class 4 SDДокумент25 страницVenture Capital Class 4 SDMary Williams100% (1)

- Omnicom Group: Financial Position of Omnicon GroupДокумент7 страницOmnicom Group: Financial Position of Omnicon GroupPuja AryaОценок пока нет

- Managerial Accounting Solutions Chapter 3 PDFДокумент42 страницыManagerial Accounting Solutions Chapter 3 PDFadam_garcia_81Оценок пока нет

- Liability of Accommodation Party in Negotiable InstrumentsДокумент7 страницLiability of Accommodation Party in Negotiable InstrumentsRonalyn Orpiano0% (1)

- PSA - Financial Accounting PDFДокумент684 страницыPSA - Financial Accounting PDFMinhajul Haque Sajal100% (1)

- Enron Scandal - Wikipedia PDFДокумент31 страницаEnron Scandal - Wikipedia PDFJohn Philip De GuzmanОценок пока нет

- Alamo Child Care WaiverДокумент1 страницаAlamo Child Care WaiverAlamo Drafthouse CinemaОценок пока нет

- Hilton Us FDDДокумент321 страницаHilton Us FDDPari SavlaОценок пока нет

- 11 Fortune Cement Vs NLRCДокумент4 страницы11 Fortune Cement Vs NLRCLegaspiCabatchaОценок пока нет

- Report On Tax Saving SchemesДокумент16 страницReport On Tax Saving SchemesDivya Vishwanadh100% (1)

- PC Collectionreceipt 10093857Документ1 страницаPC Collectionreceipt 10093857Ravi ShekhawatОценок пока нет

- AbandonmentДокумент5 страницAbandonmentDuke EphraimОценок пока нет

- Catalyst Tic PDFДокумент12 страницCatalyst Tic PDF66apenlullenОценок пока нет

- Cs Executive Taxation Solution Dec 2015 ExamsДокумент9 страницCs Executive Taxation Solution Dec 2015 ExamsBJK SIVA0% (2)

- Market Evaluation of PepsiДокумент110 страницMarket Evaluation of Pepsirafeeq505100% (1)

- Ibus Topology Original With ModsДокумент3 страницыIbus Topology Original With ModsJeevanath VeluОценок пока нет