Вам также может понравиться

- Topic 2Документ16 страницTopic 2Anonymous lVpFnX3Оценок пока нет

- Review of Some Online Banks and Visa/Master Cards IssuersОт EverandReview of Some Online Banks and Visa/Master Cards IssuersОценок пока нет

- Commerce Topic 2Документ16 страницCommerce Topic 2Anonymous lVpFnX3Оценок пока нет

- Money and Banking ProjectДокумент11 страницMoney and Banking Projectshahroze ALIОценок пока нет

- Evaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersОт EverandEvaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersОценок пока нет

- Modern Banking AnswersДокумент10 страницModern Banking AnswersAndalОценок пока нет

- File 1641790871 0004738 BLPДокумент118 страницFile 1641790871 0004738 BLPwww.ishusingh4420Оценок пока нет

- 2010 BB Brochure EngДокумент2 страницы2010 BB Brochure EngjoswaroopОценок пока нет

- Chapter 13 BankingДокумент5 страницChapter 13 BankingdragongskdbsОценок пока нет

- FM 202 Finals3Документ34 страницыFM 202 Finals3sudariodaisyre19Оценок пока нет

- Banks Other Bank TransactionsДокумент35 страницBanks Other Bank TransactionsBrenda PanyoОценок пока нет

- Card Buisiness Crdit Card EtcДокумент5 страницCard Buisiness Crdit Card EtcTarun GargОценок пока нет

- Commerce 1 GRD 12 ProjectДокумент12 страницCommerce 1 GRD 12 ProjectNeriaОценок пока нет

- SCR Banking GJKJ - HJHДокумент31 страницаSCR Banking GJKJ - HJHamitguptaujjОценок пока нет

- Watch Your Savings GrowДокумент14 страницWatch Your Savings GrowpratikjaiОценок пока нет

- Banking ProjectДокумент30 страницBanking Projectdhanya2979Оценок пока нет

- FABM2 Week 9 Bank AccountsДокумент7 страницFABM2 Week 9 Bank AccountsLoresse Guillian Asiado DiataОценок пока нет

- 1 Introduction To BankingДокумент8 страниц1 Introduction To BankingGurnihalОценок пока нет

- Week 1: Basic Documents and Transactions Related To Bank DepositsДокумент6 страницWeek 1: Basic Documents and Transactions Related To Bank Depositsgregorio gualdadОценок пока нет

- 8A&B Fin LitДокумент22 страницы8A&B Fin LitRamandeep KaurОценок пока нет

- Chapter16 - Basic Savings Bank Deposit AccountДокумент3 страницыChapter16 - Basic Savings Bank Deposit Accountshubhram2014Оценок пока нет

- What Is A BankДокумент5 страницWhat Is A BankmanojdunnhumbyОценок пока нет

- Types of Bank AccountsДокумент8 страницTypes of Bank Accountschaitanya100% (1)

- Fin 202Документ23 страницыFin 202Dorji DelmaОценок пока нет

- Policy On Bank DepositsДокумент11 страницPolicy On Bank DepositsAnshuman SharmaОценок пока нет

- Accounts of IndividualsДокумент67 страницAccounts of IndividualsgauriОценок пока нет

- English For International Trade - 2022 - Condori Deolinda Sofia BelenДокумент17 страницEnglish For International Trade - 2022 - Condori Deolinda Sofia BelenSofia CondoriОценок пока нет

- Banking ProductsДокумент11 страницBanking ProductsRadhi BalanОценок пока нет

- Lession 3 OperationsДокумент13 страницLession 3 Operationssusma susmaОценок пока нет

- Banking Is Described As The Business of Taking and Securing Money Held by Other People and CompaniesДокумент8 страницBanking Is Described As The Business of Taking and Securing Money Held by Other People and CompaniesTasnim ZaraОценок пока нет

- Module 1Документ15 страницModule 1Prajakta GokhaleОценок пока нет

- Basic Banking TransactionДокумент30 страницBasic Banking TransactionJennifer Dela Rosa100% (1)

- New Credit CardsДокумент68 страницNew Credit CardsManish GadekarОценок пока нет

- What Is Commercial Bank? Discuss The Different Product and Services Provided by Commercial Banks?Документ8 страницWhat Is Commercial Bank? Discuss The Different Product and Services Provided by Commercial Banks?KING ZIОценок пока нет

- BankFin Midterm Mod 6Документ4 страницыBankFin Midterm Mod 6Devon DebarrasОценок пока нет

- Part 3Документ29 страницPart 3Rajib DattaОценок пока нет

- Syndicate BankДокумент28 страницSyndicate BankPriya MoorthyОценок пока нет

- Opening A Bank Account Can Seem IntimidatingДокумент9 страницOpening A Bank Account Can Seem IntimidatingtriratnacomОценок пока нет

- Retail Banking in Allahabad BankДокумент45 страницRetail Banking in Allahabad Bankaru161112Оценок пока нет

- Pubali BankДокумент13 страницPubali BankAminul Islam100% (1)

- Chapter 2 - Basic Documents and TransactionsДокумент33 страницыChapter 2 - Basic Documents and Transactionsmarissa casareno almuete100% (1)

- Citizenship Charter of DBДокумент13 страницCitizenship Charter of DBPrathyusha KothaОценок пока нет

- Central Banking 2.1 The Role and FunctionsДокумент34 страницыCentral Banking 2.1 The Role and FunctionsSubodh RoyОценок пока нет

- Kokan BankДокумент20 страницKokan BankramshaОценок пока нет

- BankingДокумент19 страницBankingTipu SultanОценок пока нет

- History: BankingДокумент20 страницHistory: BankingSubhadipGhoshОценок пока нет

- Unit 2 - Sbaa7001 Banking Products and ServicesДокумент38 страницUnit 2 - Sbaa7001 Banking Products and ServicesGracyОценок пока нет

- Lucknow University: Banking OperationsДокумент9 страницLucknow University: Banking OperationsAbhishek singhОценок пока нет

- Handbook For NSDL Depository Operations Module: Core ServicesДокумент108 страницHandbook For NSDL Depository Operations Module: Core ServicesMichael PetersonОценок пока нет

- Axis Bank ProjectДокумент48 страницAxis Bank Projectsohail shaikhОценок пока нет

- Latest Trends in Banking: Debit CardДокумент10 страницLatest Trends in Banking: Debit CardChristineОценок пока нет

- Unit 3. Procedure For Opening & Operating of Deposit AccountДокумент11 страницUnit 3. Procedure For Opening & Operating of Deposit AccountBhagyesh ThakurОценок пока нет

- Unit 3 TybbaДокумент11 страницUnit 3 TybbaChaitanya FulariОценок пока нет

- Chapter 3 - Retail DepositsДокумент115 страницChapter 3 - Retail Depositssudpost4uОценок пока нет

- Oman BNK AcntДокумент8 страницOman BNK AcntAneeza zafarОценок пока нет

- General Utility Services of Commercial Banks: Transactions. They Are Called Authorized Dealers. The BankДокумент10 страницGeneral Utility Services of Commercial Banks: Transactions. They Are Called Authorized Dealers. The BankSharan YadavОценок пока нет

- Retail Banking of Allahabad BankДокумент50 страницRetail Banking of Allahabad Bankaru161112Оценок пока нет

- Sheethal.S Bcom AccaДокумент23 страницыSheethal.S Bcom AccaSheethal SrinevasОценок пока нет

- EconomicsДокумент36 страницEconomicsSayed Nadeem A. KazmiОценок пока нет

- Job Analysis 1Документ35 страницJob Analysis 1Sayed Nadeem A. KazmiОценок пока нет

- Name:Shifa Siddiqui Jahan Class: 11 Div: J Sub: Evs ROLL NO: 3052Документ11 страницName:Shifa Siddiqui Jahan Class: 11 Div: J Sub: Evs ROLL NO: 3052Sayed Nadeem A. KazmiОценок пока нет

- IntrductionДокумент1 страницаIntrductionSayed Nadeem A. KazmiОценок пока нет

- EconomicsДокумент36 страницEconomicsSayed Nadeem A. KazmiОценок пока нет

- ParleДокумент77 страницParleKaushal Gupta33% (3)

- Maxx Moblink Private LimtedДокумент1 страницаMaxx Moblink Private LimtedSayed Nadeem A. KazmiОценок пока нет

- ParleДокумент77 страницParleKaushal Gupta33% (3)

- Swot Analysis of Hide Amp SeekДокумент2 страницыSwot Analysis of Hide Amp SeekSayed Nadeem A. KazmiОценок пока нет

- CodingДокумент35 страницCodingSayed Nadeem A. KazmiОценок пока нет

- Zee TelefilmsДокумент1 страницаZee TelefilmsSayed Nadeem A. KazmiОценок пока нет

- Financial Institution Financial IntermediaryДокумент15 страницFinancial Institution Financial IntermediarySayed Nadeem A. KazmiОценок пока нет

- Turnaround Project ZeeДокумент7 страницTurnaround Project ZeeSayed Nadeem A. KazmiОценок пока нет

- Viet Ebook Company: - Dao Thi Hong Tham (Tracy) - Tong Duy Hieu (Jack) - Mr. BinjieДокумент27 страницViet Ebook Company: - Dao Thi Hong Tham (Tracy) - Tong Duy Hieu (Jack) - Mr. BinjiebombyĐОценок пока нет

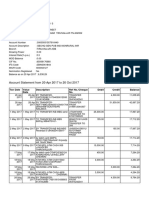

- e-StatementBRImo 099601032913537 Jun2023 20230706 133913Документ8 страницe-StatementBRImo 099601032913537 Jun2023 20230706 133913hernanОценок пока нет

- I - Functions of MoneyДокумент38 страницI - Functions of MoneyVISHVESH JUNEJAОценок пока нет

- Disbursement Voucher FeedingДокумент2 страницыDisbursement Voucher FeedingRuben0% (1)

- Membership ApplicationДокумент5 страницMembership ApplicationAbhishek VijayОценок пока нет

- The Future of The Mobile Payment As Electronic Payment System PDFДокумент6 страницThe Future of The Mobile Payment As Electronic Payment System PDFRohan MehtaОценок пока нет

- Nomad 2023 March Monthly StatementsДокумент4 страницыNomad 2023 March Monthly StatementsRogério FrançaОценок пока нет

- Qatar AirwaysДокумент3 страницыQatar AirwaysJess Elias ObarОценок пока нет

- Awareness About Cash Less Economy Among Students: K. Girija & M. NandhiniДокумент8 страницAwareness About Cash Less Economy Among Students: K. Girija & M. NandhiniTJPRC PublicationsОценок пока нет

- Presentation Eng - Residence Culture 2024 - EngДокумент7 страницPresentation Eng - Residence Culture 2024 - EngAdriana Leyton GarateОценок пока нет

- Stanbicpricingguide2022 2023Документ1 страницаStanbicpricingguide2022 2023Yaseen QariОценок пока нет

- Eea QP 03-16Документ35 страницEea QP 03-16zoiОценок пока нет

- Mju TVi 0 H RIa VPD 3 CДокумент5 страницMju TVi 0 H RIa VPD 3 CPallaviОценок пока нет

- Improving Online Admission SystemДокумент9 страницImproving Online Admission SystemKumar2019Оценок пока нет

- Development of E-Wallet System For Tertiary Institution in A Developing CountryДокумент12 страницDevelopment of E-Wallet System For Tertiary Institution in A Developing CountryFernando VidoniОценок пока нет

- Last Six Months Banking Finance and Economy Current Affairs PDFДокумент111 страницLast Six Months Banking Finance and Economy Current Affairs PDFAbhishekОценок пока нет

- Account Statement564Документ12 страницAccount Statement564Kiran SNОценок пока нет

- Civil Suit 396 of 2011Документ8 страницCivil Suit 396 of 2011wanyamaОценок пока нет

- PTE Academic Online Test Taker Handbook - May 2022Документ28 страницPTE Academic Online Test Taker Handbook - May 2022Tommy Linny H.Оценок пока нет

- Customer Retention Strategies at HDFC BankДокумент20 страницCustomer Retention Strategies at HDFC BankHemantSharma100% (1)

- Plane Ticket PAPAДокумент2 страницыPlane Ticket PAPAkerwin val AldeonОценок пока нет

- IndusInd Bank LTD.Документ72 страницыIndusInd Bank LTD.Prateek Logani100% (2)

- PayflowPro GuideДокумент198 страницPayflowPro GuidevaradasriniОценок пока нет

- IVeri WebAPI Developers GuideДокумент18 страницIVeri WebAPI Developers GuidedefamaОценок пока нет

- Chapter 4Документ11 страницChapter 4Salman SathiОценок пока нет

- PBB Bank StatementДокумент4 страницыPBB Bank Statementzhi xia100% (1)

- Harry BennettДокумент1 страницаHarry BennettEmannuel Ontario33% (3)

- User Agreement: General Terms and ConditionsДокумент32 страницыUser Agreement: General Terms and ConditionsJustin WaongoОценок пока нет

- PRACTICAL FILE OF E-COMMERCE 1 (Richa Jha)Документ55 страницPRACTICAL FILE OF E-COMMERCE 1 (Richa Jha)Shivam MishraОценок пока нет

- Pricing of Financial Products and Services Offered by BankДокумент42 страницыPricing of Financial Products and Services Offered by BankSmitaОценок пока нет

- Perversion of Justice: The Jeffrey Epstein StoryОт EverandPerversion of Justice: The Jeffrey Epstein StoryРейтинг: 4.5 из 5 звезд4.5/5 (10)

- Reading the Constitution: Why I Chose Pragmatism, not TextualismОт EverandReading the Constitution: Why I Chose Pragmatism, not TextualismОценок пока нет

- For the Thrill of It: Leopold, Loeb, and the Murder That Shocked Jazz Age ChicagoОт EverandFor the Thrill of It: Leopold, Loeb, and the Murder That Shocked Jazz Age ChicagoРейтинг: 4 из 5 звезд4/5 (97)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingОт EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingРейтинг: 4.5 из 5 звезд4.5/5 (97)

- Nine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesОт EverandNine Black Robes: Inside the Supreme Court's Drive to the Right and Its Historic ConsequencesОценок пока нет

- Hunting Whitey: The Inside Story of the Capture & Killing of America's Most Wanted Crime BossОт EverandHunting Whitey: The Inside Story of the Capture & Killing of America's Most Wanted Crime BossРейтинг: 3.5 из 5 звезд3.5/5 (6)

- All You Need to Know About the Music Business: Eleventh EditionОт EverandAll You Need to Know About the Music Business: Eleventh EditionОценок пока нет

- Reasonable Doubts: The O.J. Simpson Case and the Criminal Justice SystemОт EverandReasonable Doubts: The O.J. Simpson Case and the Criminal Justice SystemРейтинг: 4 из 5 звезд4/5 (25)

- The Law of the Land: The Evolution of Our Legal SystemОт EverandThe Law of the Land: The Evolution of Our Legal SystemРейтинг: 4.5 из 5 звезд4.5/5 (11)

- The Edge of Innocence: The Trial of Casper BennettОт EverandThe Edge of Innocence: The Trial of Casper BennettРейтинг: 4.5 из 5 звезд4.5/5 (3)

- Summary: Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) by Thomas Erikson: Key Takeaways, Summary & AnalysisОт EverandSummary: Surrounded by Idiots: The Four Types of Human Behavior and How to Effectively Communicate with Each in Business (and in Life) by Thomas Erikson: Key Takeaways, Summary & AnalysisРейтинг: 4 из 5 звезд4/5 (2)

- Insider's Guide To Your First Year Of Law School: A Student-to-Student Handbook from a Law School SurvivorОт EverandInsider's Guide To Your First Year Of Law School: A Student-to-Student Handbook from a Law School SurvivorРейтинг: 3.5 из 5 звезд3.5/5 (3)

- Learning to Disagree: The Surprising Path to Navigating Differences with Empathy and RespectОт EverandLearning to Disagree: The Surprising Path to Navigating Differences with Empathy and RespectОценок пока нет

- Free & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageОт EverandFree & Clear, Standing & Quiet Title: 11 Possible Ways to Get Rid of Your MortgageРейтинг: 2 из 5 звезд2/5 (3)

- Get Outta Jail Free Card “Jim Crow’s last stand at perpetuating slavery” Non-Unanimous Jury Verdicts & Voter SuppressionОт EverandGet Outta Jail Free Card “Jim Crow’s last stand at perpetuating slavery” Non-Unanimous Jury Verdicts & Voter SuppressionРейтинг: 5 из 5 звезд5/5 (1)

- Chokepoint Capitalism: How Big Tech and Big Content Captured Creative Labor Markets and How We'll Win Them BackОт EverandChokepoint Capitalism: How Big Tech and Big Content Captured Creative Labor Markets and How We'll Win Them BackРейтинг: 5 из 5 звезд5/5 (20)

- Waste: One Woman’s Fight Against America’s Dirty SecretОт EverandWaste: One Woman’s Fight Against America’s Dirty SecretРейтинг: 5 из 5 звезд5/5 (1)

- Art of Commenting: How to Influence Environmental Decisionmaking With Effective Comments, The, 2d EditionОт EverandArt of Commenting: How to Influence Environmental Decisionmaking With Effective Comments, The, 2d EditionРейтинг: 3 из 5 звезд3/5 (1)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!От EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Рейтинг: 4.5 из 5 звезд4.5/5 (14)

- Conviction: The Untold Story of Putting Jodi Arias Behind BarsОт EverandConviction: The Untold Story of Putting Jodi Arias Behind BarsРейтинг: 4.5 из 5 звезд4.5/5 (16)