Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1091)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- 8AДокумент17 страниц8Aselene50% (2)

- Article Family FarmДокумент3 страницыArticle Family FarmknappnlktjqvensОценок пока нет

- Re InsuranceДокумент26 страницRe Insurancepankajgupta100% (2)

- 1.02 Introduction To HPI Sub-ConceptsДокумент38 страниц1.02 Introduction To HPI Sub-ConceptsNurmalinda SihombingОценок пока нет

- Third Party InsuranceДокумент22 страницыThird Party InsurancePulkit Mago 1703887Оценок пока нет

- Class 9 SST WorksheetДокумент3 страницыClass 9 SST WorksheetBharat GundОценок пока нет

- Daftar Pustaka: LILIK YULIANTO N, Prof. Dr. Bambang Riyanto L.S., MBA., Ak, CAДокумент3 страницыDaftar Pustaka: LILIK YULIANTO N, Prof. Dr. Bambang Riyanto L.S., MBA., Ak, CAAnggit Jaya MuktiОценок пока нет

- Pestle Analysis of Bangladesh: AssignmentДокумент8 страницPestle Analysis of Bangladesh: AssignmentSrinivasan KCОценок пока нет

- ClothingДокумент2 страницыClothingFHKОценок пока нет

- Hutti Gold Mines 02 Mar 2012Документ3 страницыHutti Gold Mines 02 Mar 2012Chandrakumar87Оценок пока нет

- LP 1T Pipes Critical Crane Lift Plan 25T Crane CPFДокумент1 страницаLP 1T Pipes Critical Crane Lift Plan 25T Crane CPFMPS PSKОценок пока нет

- Melbourne Itinerary PDFДокумент7 страницMelbourne Itinerary PDFdawna25Оценок пока нет

- Semirara Mining and Power Corporation-ScriptДокумент8 страницSemirara Mining and Power Corporation-ScriptYan's Senora BescoroОценок пока нет

- Impact of Globalization On Pharmaceutical IndustryДокумент15 страницImpact of Globalization On Pharmaceutical IndustrySneha Tawsalkar50% (2)

- Form For Cargo Information For Solid Bulk Cargoes: E.g., Class & UN No. or "MHB"Документ2 страницыForm For Cargo Information For Solid Bulk Cargoes: E.g., Class & UN No. or "MHB"Jayme LemОценок пока нет

- Surat Chennai EMT59092244Документ2 страницыSurat Chennai EMT59092244nik1111Оценок пока нет

- Custom Seat Rail FormДокумент1 страницаCustom Seat Rail FormIvan Ezequiel CastilloОценок пока нет

- Beck Daniel ResumeДокумент1 страницаBeck Daniel Resumeapi-278118064Оценок пока нет

- Preliminary Assessment SEAM 3Документ14 страницPreliminary Assessment SEAM 3nerissa belloОценок пока нет

- Capital Formation in Agriculture PDFДокумент17 страницCapital Formation in Agriculture PDFArya SenapatiОценок пока нет

- Metro Manila PhilippinesДокумент27 страницMetro Manila PhilippinesRaymond AnactaОценок пока нет

- Construction On Rivonia Road Rea Vaya BRT Station CommencesДокумент3 страницыConstruction On Rivonia Road Rea Vaya BRT Station CommencesJDAОценок пока нет

- Tugas Bahasa Inggris Retail Banking: By: Group EightДокумент5 страницTugas Bahasa Inggris Retail Banking: By: Group EightOka HagaОценок пока нет

- Dutch Flower Cluster v2Документ9 страницDutch Flower Cluster v2gagafikОценок пока нет

- Green Peace Lincoln College: IntroductionДокумент36 страницGreen Peace Lincoln College: IntroductionLucas lopezОценок пока нет

- Steel Industry in LahoreДокумент6 страницSteel Industry in LahoreEngr Muhammad Haider Ali100% (1)

- Haitian Jupiter SeriesДокумент4 страницыHaitian Jupiter SeriesRenardОценок пока нет

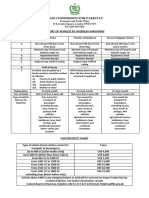

- High Commission For Pakistan: Import of Vehicles by Overseas PakistanisДокумент1 страницаHigh Commission For Pakistan: Import of Vehicles by Overseas Pakistaniszeeshan tanveerОценок пока нет

- Angola Offshore - MagДокумент52 страницыAngola Offshore - Magrieza_fОценок пока нет

- gr8 Business-Ch2 Classification of Business Notes With Case StudyДокумент8 страницgr8 Business-Ch2 Classification of Business Notes With Case StudyTariqul Islam0% (2)