Вам также может понравиться

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Cash Flow StatementsДокумент48 страницCash Flow StatementsApollo Institute of Hospital Administration60% (5)

- Income Tax Book by CA Suraj Agrawal - May & Nov 2020 Exam - CompressedДокумент590 страницIncome Tax Book by CA Suraj Agrawal - May & Nov 2020 Exam - CompressedSonali Dixit100% (1)

- PILMICO v. CIRДокумент2 страницыPILMICO v. CIRPat EspinozaОценок пока нет

- PNB vs. SantosДокумент2 страницыPNB vs. SantosAyi Anigan100% (1)

- Finman ReviewerДокумент5 страницFinman ReviewerCecilia TanОценок пока нет

- Caspian Oil and Gas Potential and Export ChallengesДокумент285 страницCaspian Oil and Gas Potential and Export ChallengespauldmeОценок пока нет

- Dilg Joincircular 2016815 81d0d76d7eДокумент16 страницDilg Joincircular 2016815 81d0d76d7eRaidenAiОценок пока нет

- Donors Tax Handout 3Документ5 страницDonors Tax Handout 3Xerez SingsonОценок пока нет

- OECD International Academy For Tax Crime InvestigationДокумент25 страницOECD International Academy For Tax Crime InvestigationADBI EventsОценок пока нет

- 7089 LIIHEN AnnualReport 2016-12-31 Lii Hen 2016 Annual Report 1661818133Документ156 страниц7089 LIIHEN AnnualReport 2016-12-31 Lii Hen 2016 Annual Report 1661818133Jordan YiiОценок пока нет

- Abdul Latif and Rafiq Cleaning Services L.L.CДокумент2 страницыAbdul Latif and Rafiq Cleaning Services L.L.CMuhammad Shahzad ChandiaОценок пока нет

- 7 The Crown As Corporation by Frederick MaitlandДокумент14 страниц7 The Crown As Corporation by Frederick Maitlandarchivaris.archief6573Оценок пока нет

- Heritage Investment in ThailandДокумент5 страницHeritage Investment in ThailandPacharaporn PhanomvanОценок пока нет

- Spring2022 Paper Berrychristopher 2-24-22Документ58 страницSpring2022 Paper Berrychristopher 2-24-22Cristiana NobileОценок пока нет

- Garmin Invoice for Helicopter Navigation Data SubscriptionДокумент1 страницаGarmin Invoice for Helicopter Navigation Data SubscriptionernestozagОценок пока нет

- Chapter 26Документ8 страницChapter 26Mae Ciarie YangcoОценок пока нет

- Pakistan Under Musharraf RegimeДокумент27 страницPakistan Under Musharraf Regimeapi-3713302100% (2)

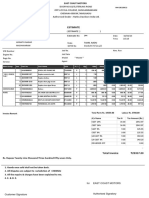

- Job Est PrintДокумент1 страницаJob Est PrintKashish JainОценок пока нет

- 1 - Pe GuideДокумент386 страниц1 - Pe GuidePramod RaiОценок пока нет

- DISPOSAL OF SUBSIDIARY SHARESДокумент9 страницDISPOSAL OF SUBSIDIARY SHARESCourage KanyonganiseОценок пока нет

- TaxationДокумент71 страницаTaxationUnnati RawatОценок пока нет

- Chapter 7 - Forecasting Financial StatementsДокумент23 страницыChapter 7 - Forecasting Financial Statementsamanthi gunarathna95Оценок пока нет

- Chapter 5 TaxationДокумент3 страницыChapter 5 TaxationAngela Nicole NobletaОценок пока нет

- State - A Community of Persons More or Less Numerous, Permanently Occupying A Definite Portion ofДокумент7 страницState - A Community of Persons More or Less Numerous, Permanently Occupying A Definite Portion ofRonna MaeОценок пока нет

- API COD DS2 en Excel v2 1622388Документ454 страницыAPI COD DS2 en Excel v2 1622388jo joОценок пока нет

- Ordinance No 302 2016 of The 2nd DecemberДокумент118 страницOrdinance No 302 2016 of The 2nd DecemberEscobar Ruiz Iris MaríaОценок пока нет

- Haritha Hotel Booking Keesaragutta PDFДокумент4 страницыHaritha Hotel Booking Keesaragutta PDFRaviTeja KvsnОценок пока нет

- Sales: IFRS 15 - Revenue From Contracts With CustomersДокумент20 страницSales: IFRS 15 - Revenue From Contracts With CustomersMeena PannalaОценок пока нет

- PaymentДокумент1 страницаPaymentPepe PeprОценок пока нет

- Tax Invoice for Agricultural ToolsДокумент1 страницаTax Invoice for Agricultural ToolspharmastudiesОценок пока нет