Вам также может понравиться

- Ranbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertДокумент4 страницыRanbaxy Labs: Mohali Plant Likely To Be Under USFDA Import AlertAngel BrokingОценок пока нет

- Oilseeds and Edible Oil UpdateДокумент9 страницOilseeds and Edible Oil UpdateAngel BrokingОценок пока нет

- WPIInflation August2013Документ5 страницWPIInflation August2013Angel BrokingОценок пока нет

- Daily Agri Tech Report September 14 2013Документ2 страницыDaily Agri Tech Report September 14 2013Angel BrokingОценок пока нет

- International Commodities Evening Update September 16 2013Документ3 страницыInternational Commodities Evening Update September 16 2013Angel BrokingОценок пока нет

- Daily Agri Report September 16 2013Документ9 страницDaily Agri Report September 16 2013Angel BrokingОценок пока нет

- Daily Metals and Energy Report September 16 2013Документ6 страницDaily Metals and Energy Report September 16 2013Angel BrokingОценок пока нет

- Derivatives Report 8th JanДокумент3 страницыDerivatives Report 8th JanAngel BrokingОценок пока нет

- Market Outlook: Dealer's DiaryДокумент13 страницMarket Outlook: Dealer's DiaryAngel BrokingОценок пока нет

- Daily Agri Tech Report September 16 2013Документ2 страницыDaily Agri Tech Report September 16 2013Angel BrokingОценок пока нет

- Daily Technical Report: Sensex (19733) / NIFTY (5851)Документ4 страницыDaily Technical Report: Sensex (19733) / NIFTY (5851)Angel BrokingОценок пока нет

- Currency Daily Report September 16 2013Документ4 страницыCurrency Daily Report September 16 2013Angel BrokingОценок пока нет

- Daily Agri Tech Report September 12 2013Документ2 страницыDaily Agri Tech Report September 12 2013Angel BrokingОценок пока нет

- Daily Technical Report: Sensex (19997) / NIFTY (5913)Документ4 страницыDaily Technical Report: Sensex (19997) / NIFTY (5913)Angel Broking100% (1)

- Metal and Energy Tech Report Sept 13Документ2 страницыMetal and Energy Tech Report Sept 13Angel BrokingОценок пока нет

- Press Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressДокумент1 страницаPress Note - Angel Broking Has Been Recognized With Two Awards at Asia Pacific HRM CongressAngel BrokingОценок пока нет

- Tata Motors: Jaguar Land Rover - Monthly Sales UpdateДокумент6 страницTata Motors: Jaguar Land Rover - Monthly Sales UpdateAngel BrokingОценок пока нет

- Currency Daily Report September 13 2013Документ4 страницыCurrency Daily Report September 13 2013Angel BrokingОценок пока нет

- Jaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechДокумент4 страницыJaiprakash Associates: Agreement To Sell Gujarat Cement Unit To UltratechAngel BrokingОценок пока нет

- Market Outlook: Dealer's DiaryДокумент12 страницMarket Outlook: Dealer's DiaryAngel BrokingОценок пока нет

- Metal and Energy Tech Report Sept 12Документ2 страницыMetal and Energy Tech Report Sept 12Angel BrokingОценок пока нет

- Daily Metals and Energy Report September 12 2013Документ6 страницDaily Metals and Energy Report September 12 2013Angel BrokingОценок пока нет

- Daily Agri Report September 12 2013Документ9 страницDaily Agri Report September 12 2013Angel BrokingОценок пока нет

- Market Outlook: Dealer's DiaryДокумент13 страницMarket Outlook: Dealer's DiaryAngel BrokingОценок пока нет

- Currency Daily Report September 12 2013Документ4 страницыCurrency Daily Report September 12 2013Angel BrokingОценок пока нет

- Daily Technical Report: Sensex (19997) / NIFTY (5897)Документ4 страницыDaily Technical Report: Sensex (19997) / NIFTY (5897)Angel BrokingОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- 2Q 2020 GLVA Galva+Technologies+TbkДокумент66 страниц2Q 2020 GLVA Galva+Technologies+TbkAank KurniaОценок пока нет

- Backus Valuation ExcelДокумент28 страницBackus Valuation ExcelAdrian MontoyaОценок пока нет

- Financial & Managerial Accounting MbasДокумент40 страницFinancial & Managerial Accounting MbasHồng Long100% (1)

- Review On Financial Statement AnalysisДокумент6 страницReview On Financial Statement AnalysisDanica VetuzОценок пока нет

- Presentation of FSДокумент2 страницыPresentation of FSTimmy KellyОценок пока нет

- The Basic Purpose of Accounting IsДокумент10 страницThe Basic Purpose of Accounting IsJesicca JungОценок пока нет

- Account Form Fabm2 What I Can DoДокумент1 страницаAccount Form Fabm2 What I Can DoHenry Balmores TamayoОценок пока нет

- Template Annual ReportДокумент8 страницTemplate Annual ReportMas Hamzah FansuriОценок пока нет

- A Je Worksheet Illustration 1Документ17 страницA Je Worksheet Illustration 1Nichole TanОценок пока нет

- Adi Sarana Armada TBK.: Company Report: January 2019 As of 31 January 2019Документ3 страницыAdi Sarana Armada TBK.: Company Report: January 2019 As of 31 January 2019nugros belajarОценок пока нет

- Group 3 FS Forecasting Jollibee SourceДокумент43 страницыGroup 3 FS Forecasting Jollibee SourceChristian VillarОценок пока нет

- Financial StatementsДокумент30 страницFinancial StatementsPrincess BersaminaОценок пока нет

- Aicpa 040212far SimДокумент118 страницAicpa 040212far SimHanabusa Kawaii IdouОценок пока нет

- Baja PDFДокумент3 страницыBaja PDFdindakharismaОценок пока нет

- CH1 - Accounting in BusinessДокумент18 страницCH1 - Accounting in BusinessMaiaOshakmashviliОценок пока нет

- Persistent-With Historic DataДокумент65 страницPersistent-With Historic DataSANDHYA KHANDESHEОценок пока нет

- Presentation of Financial Statements: IASB Documents Published To Accompany Ias 1Документ30 страницPresentation of Financial Statements: IASB Documents Published To Accompany Ias 1Kemala Putri AyundaОценок пока нет

- Financial Ratio Calculator: Income StatementДокумент18 страницFinancial Ratio Calculator: Income StatementPriyal ShahОценок пока нет

- Ifrs Versus GaapДокумент25 страницIfrs Versus GaapNigist Woldeselassie100% (1)

- Chap 17 Intercompany Sales of InventoryДокумент71 страницаChap 17 Intercompany Sales of InventoryPhrexilyn PajarilloОценок пока нет

- LK Myoh 2013Документ132 страницыLK Myoh 2013Arief KurniawanОценок пока нет

- HP Cotton Sept 2021 ResultsДокумент6 страницHP Cotton Sept 2021 ResultsPuneet367Оценок пока нет

- ITC Balance SheetДокумент1 страницаITC Balance SheetDivitya ChaudharyОценок пока нет

- Intercompany Sale of PPE Problem 2: Requirement: January 1, 20x4Документ31 страницаIntercompany Sale of PPE Problem 2: Requirement: January 1, 20x4Abegail LibreaОценок пока нет

- OHADA Financial Analysis: February 2019Документ6 страницOHADA Financial Analysis: February 2019Jaime Nze Nguema BahamondeОценок пока нет

- Answer (Question) Module 4 Quiz 1 Adjusting Entries, Worksheet, FS PreparationДокумент1 страницаAnswer (Question) Module 4 Quiz 1 Adjusting Entries, Worksheet, FS Preparationkakao100% (1)

- Accounting Chapter 2Документ56 страницAccounting Chapter 2hnhОценок пока нет

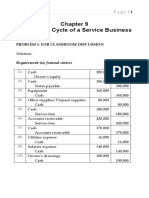

- Sol. Man. - Chapter 9 - Acctg Cycle of A Service BusinessДокумент52 страницыSol. Man. - Chapter 9 - Acctg Cycle of A Service Businesscan't yujout80% (5)

- Consolidated Financial StatementДокумент5 страницConsolidated Financial StatementTriechia LaudОценок пока нет

- Chap 21 - Leasing (PSAK 73) - E12-12Документ27 страницChap 21 - Leasing (PSAK 73) - E12-12Happy MichaelОценок пока нет