Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (265)

- System Design Data Flow Diagrams (DFD) of Job PortalДокумент10 страницSystem Design Data Flow Diagrams (DFD) of Job PortalVinod Bhaskar89% (38)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Project On Linear Programming ProblemsДокумент29 страницProject On Linear Programming ProblemsVinod Bhaskar67% (129)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Biodata For MarriageДокумент1 страницаBiodata For MarriageVinod Bhaskar50% (2)

- Resume - Curriculum Vitae Normal SampleДокумент1 страницаResume - Curriculum Vitae Normal SampleVinod Bhaskar82% (11)

- Form For Claim of Balance in The Savings Bank Account of Deceased DepositorДокумент2 страницыForm For Claim of Balance in The Savings Bank Account of Deceased DepositorVinod Bhaskar75% (60)

- 7k HR EmailsДокумент252 страницы7k HR EmailsGp Mishra33% (3)

- IGNOU Evaluation SlipДокумент1 страницаIGNOU Evaluation SlipVinod BhaskarОценок пока нет

- Higher Secondary Model Computerised Accounting Practical ExaminationДокумент3 страницыHigher Secondary Model Computerised Accounting Practical ExaminationVinod BhaskarОценок пока нет

- Computerised AccountingДокумент4 страницыComputerised AccountingVinod Bhaskar100% (1)

- Keral PSC Model 100 Questions - PSC Model Question Papers in MalayalamДокумент4 страницыKeral PSC Model 100 Questions - PSC Model Question Papers in MalayalamVinod Bhaskar50% (2)

- English 2011-2012 10th (XTH)Документ2 страницыEnglish 2011-2012 10th (XTH)Vinod BhaskarОценок пока нет

- Assignment: Strategic Financial ManagementДокумент7 страницAssignment: Strategic Financial ManagementVinod BhaskarОценок пока нет

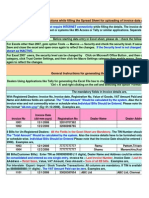

- General Instructions While Filling The Spread Sheet For Uploading of Invoice Data Along With EreturnsДокумент10 страницGeneral Instructions While Filling The Spread Sheet For Uploading of Invoice Data Along With EreturnsVinod Bhaskar0% (1)

- IGNOU Assignment Remittence-cum-Acknowledgement FromДокумент1 страницаIGNOU Assignment Remittence-cum-Acknowledgement FromVinod BhaskarОценок пока нет

- Microprocessor LAB MANUALДокумент129 страницMicroprocessor LAB MANUALChandrakantha K100% (2)

- Nuclear and Hydel Power PlantsДокумент15 страницNuclear and Hydel Power PlantsVinod BhaskarОценок пока нет

- Nuclear and Hydel Power PlantsДокумент15 страницNuclear and Hydel Power PlantsVinod BhaskarОценок пока нет

- English 2011-2012 10th (XTH)Документ2 страницыEnglish 2011-2012 10th (XTH)Vinod BhaskarОценок пока нет

- Sample - Memorandum Report Memo ReportДокумент6 страницSample - Memorandum Report Memo ReportVinod BhaskarОценок пока нет

- Mathematics 2011-2012 10th (XTH) Malayalam MediumДокумент3 страницыMathematics 2011-2012 10th (XTH) Malayalam MediumVinod BhaskarОценок пока нет

- Mathematics 2011-2012 XTH (10th) - English MediumДокумент2 страницыMathematics 2011-2012 XTH (10th) - English MediumVinod BhaskarОценок пока нет

- RadioactivityДокумент16 страницRadioactivityVinod BhaskarОценок пока нет

- Marriage Certificate ApplicationДокумент1 страницаMarriage Certificate ApplicationVinod BhaskarОценок пока нет

- Medical Uses of LasersДокумент1 страницаMedical Uses of LasersVinod BhaskarОценок пока нет

- Liquid-Drop ModelДокумент14 страницLiquid-Drop ModelVinod BhaskarОценок пока нет

- SEMINAR REPORT On Swap Space Management For NAND Flash MemoryДокумент23 страницыSEMINAR REPORT On Swap Space Management For NAND Flash MemoryVinod BhaskarОценок пока нет

- Sample Curriculum VitaeДокумент1 страницаSample Curriculum VitaeVinod BhaskarОценок пока нет

- News Articles About Issues Against WomenДокумент4 страницыNews Articles About Issues Against WomenVinod BhaskarОценок пока нет

- States of Matter - Entrance Exam Model Question Paper 2012Документ3 страницыStates of Matter - Entrance Exam Model Question Paper 2012Vinod BhaskarОценок пока нет

- General Science & Chemistry - Achievement Test July 2011 Question Paper - VIII - 7th - MalayalamДокумент3 страницыGeneral Science & Chemistry - Achievement Test July 2011 Question Paper - VIII - 7th - MalayalamVinod BhaskarОценок пока нет

- Experience Certificate - SampleДокумент1 страницаExperience Certificate - SampleVinod Bhaskar0% (1)

- IFRS 12 Disclosure Standard for Interests in Other EntitiesДокумент6 страницIFRS 12 Disclosure Standard for Interests in Other EntitiessaadalamОценок пока нет

- KRN BIR ReqДокумент2 страницыKRN BIR ReqNitz GallevoОценок пока нет

- Effect of Declining Market On TATA MotorsДокумент65 страницEffect of Declining Market On TATA Motorsarvind3041990Оценок пока нет

- Ambry Square Mall Floor Plan OverviewДокумент62 страницыAmbry Square Mall Floor Plan OverviewJackОценок пока нет

- 02 - Aditi Jain - Wendy Peterson ReportДокумент8 страниц02 - Aditi Jain - Wendy Peterson ReportKunal KaushalОценок пока нет

- Bankways BSДокумент3 страницыBankways BSJoey Albarracin SardañasОценок пока нет

- Offering Memorandum-DKAM Capital Ideas Fund (00001064-9)Документ54 страницыOffering Memorandum-DKAM Capital Ideas Fund (00001064-9)alysomjiОценок пока нет

- DocumentДокумент2 страницыDocumentNorelkis Thais Perez ArangurenОценок пока нет

- Enron-Andersen case study reveals auditor independence issuesДокумент3 страницыEnron-Andersen case study reveals auditor independence issuesFatiha Yusof0% (2)

- Flying in Ireland October 2014Документ52 страницыFlying in Ireland October 2014Adriano BelucoОценок пока нет

- M/S. Lavish Ceramics: The Project Cost 1 Cost of ProjectДокумент20 страницM/S. Lavish Ceramics: The Project Cost 1 Cost of ProjectSabhaya ChiragОценок пока нет

- Ing N.V. Metro Manila Branch Vs Cir DigestДокумент2 страницыIng N.V. Metro Manila Branch Vs Cir Digestbrian jay hernandezОценок пока нет

- A Tale of Two TradersДокумент4 страницыA Tale of Two Tradersmayankjain24inОценок пока нет

- Vodafone International Holdings B.V. vs. Union of India & Anr. (2012) 6SCC613 Tax Avoidance/Evasion: Correctness of Azadi Bachao CaseДокумент18 страницVodafone International Holdings B.V. vs. Union of India & Anr. (2012) 6SCC613 Tax Avoidance/Evasion: Correctness of Azadi Bachao CasearmsarivuОценок пока нет

- Mergers and Acquisitions: Effect On Financial Performance of Manufacturing Companies of PakistanДокумент11 страницMergers and Acquisitions: Effect On Financial Performance of Manufacturing Companies of PakistanHoney GuptaОценок пока нет

- Brandon Keith WatsonДокумент2 страницыBrandon Keith WatsonuscomplaintcenterОценок пока нет

- LIM TONG LIM Vs CAДокумент3 страницыLIM TONG LIM Vs CARoseannvalorie JaramillaОценок пока нет

- Audit and Internal ReviewДокумент6 страницAudit and Internal ReviewkhengmaiОценок пока нет

- PPSAS 17 - Guidelines for Accounting of Property, Plant and EquipmentДокумент4 страницыPPSAS 17 - Guidelines for Accounting of Property, Plant and EquipmentAr Line100% (2)

- SpiceJet's Marketing Strategies for Attracting FDIДокумент14 страницSpiceJet's Marketing Strategies for Attracting FDIPrasanna NarayananОценок пока нет

- Wasim Akram Zabin KhanДокумент70 страницWasim Akram Zabin KhanamalremeshОценок пока нет

- IcbpДокумент2 страницыIcbpdennyaikiОценок пока нет

- Customer Satisfaction at Maruti SuzukiДокумент55 страницCustomer Satisfaction at Maruti SuzukirajОценок пока нет

- BHT 1Документ44 страницыBHT 1Onkar ChavanОценок пока нет

- Edward Nell Company vs. Pacific Farms Inc.Документ4 страницыEdward Nell Company vs. Pacific Farms Inc.Gerald HernandezОценок пока нет

- FICO Interview AnswersДокумент160 страницFICO Interview Answersy janardhanreddy100% (1)

- Understanding Company LawДокумент13 страницUnderstanding Company LawUditaОценок пока нет

- Bharati Vidyapeeth Deemed University, Pune: Institute of Management andДокумент32 страницыBharati Vidyapeeth Deemed University, Pune: Institute of Management andLainious Rai50% (2)

- Volume Variety Mix ProjectДокумент12 страницVolume Variety Mix ProjectAbdullah rehmanОценок пока нет