Вам также может понравиться

- Timmons New Venture CreationДокумент30 страницTimmons New Venture CreationMessageDanceОценок пока нет

- GreenPaperiTunes03 04Документ100 страницGreenPaperiTunes03 04SuvidОценок пока нет

- Historical Release Dates Non Farm PayrollsДокумент10 страницHistorical Release Dates Non Farm PayrollsMessageDanceОценок пока нет

- Business EtiquetteДокумент57 страницBusiness EtiquetteNeeraj Bhardwaj100% (10)

- Still Working On It Meeting LongwoodДокумент2 страницыStill Working On It Meeting LongwoodMessageDanceОценок пока нет

- Facebook Open Platform Release NotesДокумент10 страницFacebook Open Platform Release NotesMessageDanceОценок пока нет

- Ryerson Fashion Portfolio InterviewДокумент2 страницыRyerson Fashion Portfolio InterviewMessageDanceОценок пока нет

- Headstand Venture-PresentationДокумент16 страницHeadstand Venture-PresentationMessageDanceОценок пока нет

- 2 Jun For MembesДокумент7 страниц2 Jun For MembesMessageDanceОценок пока нет

- Scaling Rails With MemcachedДокумент41 страницаScaling Rails With MemcachedOleksiy Kovyrin100% (7)

- USC Football Recruiting Database System.: Team 6Документ27 страницUSC Football Recruiting Database System.: Team 6MessageDanceОценок пока нет

- 0418 DepthchartДокумент2 страницы0418 DepthchartMessageDanceОценок пока нет

- DFDCHДокумент1 страницаDFDCHMessageDanceОценок пока нет

- Music and Social MovementsДокумент25 страницMusic and Social MovementsMessageDanceОценок пока нет

- 6th Central Pay Commission Salary CalculatorДокумент15 страниц6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Intro To Music HistoryДокумент17 страницIntro To Music HistoryMessageDanceОценок пока нет

- Why Music MattersДокумент35 страницWhy Music MattersMessageDanceОценок пока нет

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Jap YenДокумент13 страницThe Jap YenRadhika KashyapОценок пока нет

- Invoice IXITRS185875952789718Документ1 страницаInvoice IXITRS185875952789718PatriotОценок пока нет

- 04 2013-2014 Financial AgreementДокумент2 страницы04 2013-2014 Financial Agreementapi-234678525Оценок пока нет

- GU215RG Post To Home Address: SurreyДокумент1 страницаGU215RG Post To Home Address: SurreyhelikacarvalhoОценок пока нет

- Alasdair Macleod Sound Money 555Документ5 страницAlasdair Macleod Sound Money 555Kevin CreaseyОценок пока нет

- Coffee Table Booklet 19012024Документ244 страницыCoffee Table Booklet 19012024Antony AОценок пока нет

- Compensation Income - Fringe Benefit TaxДокумент41 страницаCompensation Income - Fringe Benefit Taxdelacruzrojohn600Оценок пока нет

- Axis Service Charges of Foreign ExchangeДокумент9 страницAxis Service Charges of Foreign ExchangeHimesh ShahОценок пока нет

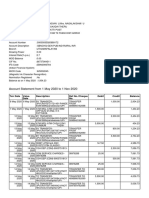

- Account Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceДокумент9 страницAccount Statement From 1 May 2020 To 1 Nov 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceChellapandiОценок пока нет

- The McDozer Blogs - Public Journal of A DropoutДокумент254 страницыThe McDozer Blogs - Public Journal of A DropoutmcdozerОценок пока нет

- ThesisДокумент193 страницыThesisDebarchitaMahapatraОценок пока нет

- Financial MarketДокумент4 страницыFinancial MarketজহিরুলইসলামশোভনОценок пока нет

- Thesis - Progress Report. For Advisor OnlyДокумент3 страницыThesis - Progress Report. For Advisor OnlyamogneОценок пока нет

- Financial Management-Kings 2012Документ2 страницыFinancial Management-Kings 2012Suman KCОценок пока нет

- Transfer - RemittanceДокумент3 страницыTransfer - RemittanceEman MostafaОценок пока нет

- EconomicsДокумент10 страницEconomicsCalvinОценок пока нет

- Chapter 8: Cash and Bank Management Daily Procedures: ObjectivesДокумент26 страницChapter 8: Cash and Bank Management Daily Procedures: ObjectivesArturo GonzalezОценок пока нет

- NISM-Series-VIII-Equity Derivatives Workbook (New Version September-2015)Документ162 страницыNISM-Series-VIII-Equity Derivatives Workbook (New Version September-2015)janardhanvn100% (3)

- AssignmentДокумент7 страницAssignmentMona VimlaОценок пока нет

- Application For Margin Money Loan To S.S.I. Units Promoted by Non-Resident Keralites From The Government of Kerala PDFДокумент6 страницApplication For Margin Money Loan To S.S.I. Units Promoted by Non-Resident Keralites From The Government of Kerala PDFdasuyaОценок пока нет

- Soal FinancialДокумент4 страницыSoal Financialnoviakus38% (8)

- Working Capital Management AssignmentДокумент10 страницWorking Capital Management AssignmentRitesh Singh RathoreОценок пока нет

- Taran Christoper S. m5 t8 ReflectionДокумент4 страницыTaran Christoper S. m5 t8 ReflectionChristoper TaranОценок пока нет

- F7 Workbook Q & A PDFДокумент247 страницF7 Workbook Q & A PDFREGIS Izere100% (1)

- Nps One PagerДокумент2 страницыNps One PagerldorayaОценок пока нет

- Export-Led Growth in Laitn America 1870 To 1930Документ18 страницExport-Led Growth in Laitn America 1870 To 1930sgysmnОценок пока нет

- The Performance of Diversified Emerging Market Equity FundsДокумент16 страницThe Performance of Diversified Emerging Market Equity FundsMuhammad RoqibunОценок пока нет

- Chapter 4 - Partnership LiquidationДокумент4 страницыChapter 4 - Partnership LiquidationMikaella BengcoОценок пока нет

- FX Get DoneДокумент2 страницыFX Get DoneDev GogoiОценок пока нет

- Direct Deposit FormДокумент2 страницыDirect Deposit FormLaz Equality Estrada100% (2)