Вам также может понравиться

- Petition for Certiorari – Patent Case 99-396 - Federal Rule of Civil Procedure 12(h)(3) Patent Assignment Statute 35 USC 261От EverandPetition for Certiorari – Patent Case 99-396 - Federal Rule of Civil Procedure 12(h)(3) Patent Assignment Statute 35 USC 261Оценок пока нет

- Petition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)От EverandPetition for Certiorari – Patent Case 01-438 - Federal Rule of Civil Procedure 52(a)Оценок пока нет

- Agruements and Case Law and Cal Codes in Defense of Unlawful DetainerДокумент4 страницыAgruements and Case Law and Cal Codes in Defense of Unlawful DetainerLelana Villa100% (2)

- Reply To An Opposition To Motion in CaliforniaДокумент2 страницыReply To An Opposition To Motion in CaliforniaStan Burman100% (1)

- BriefДокумент14 страницBriefDawn Plaza100% (1)

- Rosa Motion To Setside BMWДокумент12 страницRosa Motion To Setside BMWMorssaJimenezОценок пока нет

- Request For Judicial Notice - The Law Office of Ryan James SmytheДокумент30 страницRequest For Judicial Notice - The Law Office of Ryan James SmytheOrangeCountyBestAttorneys100% (1)

- Plaintiff's Opposition to Demurrer of Foreclosure ComplaintДокумент34 страницыPlaintiff's Opposition to Demurrer of Foreclosure ComplaintAltis PeoplesОценок пока нет

- Petition For ReHearingДокумент23 страницыPetition For ReHearingLee Perry100% (1)

- Appellants Opening BriefДокумент45 страницAppellants Opening BriefAnonymous yY64T4x0M100% (1)

- Opposition To Motion To Dismiss and Request For Judicial NoticeДокумент5 страницOpposition To Motion To Dismiss and Request For Judicial NoticeAshley ThorpeОценок пока нет

- Holtzman v. Cirgadyne - Reply To Opposition To Motion To Strike Portions of ComplaintДокумент5 страницHoltzman v. Cirgadyne - Reply To Opposition To Motion To Strike Portions of ComplaintLDuquidОценок пока нет

- 1st Amended Opening Brief On AppealДокумент16 страниц1st Amended Opening Brief On Appealrikwmun100% (1)

- Opp To Demurrer (Bookmarked) PDFДокумент45 страницOpp To Demurrer (Bookmarked) PDFGeorge SharpОценок пока нет

- RealNetworks Motion For Leave To File Second Amended ComplaintДокумент10 страницRealNetworks Motion For Leave To File Second Amended ComplaintBen SheffnerОценок пока нет

- FL - Hearing Transcript - The Issue of Complaint VerificationДокумент16 страницFL - Hearing Transcript - The Issue of Complaint Verificationwinstons2311100% (2)

- Sample Opposition To Rule 60 (B) (2) Motion To Vacate JudgmentДокумент3 страницыSample Opposition To Rule 60 (B) (2) Motion To Vacate JudgmentStan BurmanОценок пока нет

- Glaski - Respondent's BriefДокумент30 страницGlaski - Respondent's Brief83jjmackОценок пока нет

- Appeals Brief Nov 2016Документ29 страницAppeals Brief Nov 2016Kimberly Parton BolinОценок пока нет

- Motion On The PleadingsДокумент41 страницаMotion On The Pleadingsraicha980% (1)

- Our Demurrer To ComplДокумент10 страницOur Demurrer To Compltmccand100% (2)

- AG Petition For RehearingДокумент15 страницAG Petition For RehearingmattОценок пока нет

- GC 045202 Arrest of Judge Stewart From Burbank Courtwith ExhibitsДокумент24 страницыGC 045202 Arrest of Judge Stewart From Burbank Courtwith ExhibitsJose SalazarОценок пока нет

- Sample Renewal of Motion For California DivorceДокумент3 страницыSample Renewal of Motion For California DivorceStan BurmanОценок пока нет

- Opposition To Respondent's Motion For Summary JudgmentДокумент23 страницыOpposition To Respondent's Motion For Summary JudgmentBasseemОценок пока нет

- Glaski - Appellant's Opening BriefДокумент50 страницGlaski - Appellant's Opening Brief83jjmackОценок пока нет

- Jones Motion To Remand To State Court 11/01/21Документ17 страницJones Motion To Remand To State Court 11/01/21José Duarte100% (1)

- Defendants' Reply To Plaintiff's Opposition To DismissДокумент7 страницDefendants' Reply To Plaintiff's Opposition To DismissBen Z.Оценок пока нет

- Defendant's Notice of Ex-Parte Application for Continuance of Default Prove-Up HearingДокумент16 страницDefendant's Notice of Ex-Parte Application for Continuance of Default Prove-Up HearingValerie LopezОценок пока нет

- Exparte Motion To Stay Pending Appeal and Civil Case FontanaДокумент9 страницExparte Motion To Stay Pending Appeal and Civil Case Fontanaaquauris33136100% (1)

- Ex Parte - Tro.01Документ14 страницEx Parte - Tro.01Pinup Mosley100% (1)

- Cal Code Civ Proc 425.16Документ83 страницыCal Code Civ Proc 425.16autumngraceОценок пока нет

- Ex Parte Memo of Points AuthoritiesДокумент4 страницыEx Parte Memo of Points AuthoritiesAttorneyОценок пока нет

- Sample Motion To Compel Production of Documents For CaliforniaДокумент4 страницыSample Motion To Compel Production of Documents For CaliforniaJacqueline LunaОценок пока нет

- PleadingДокумент1 страницаPleadingjedcridlandОценок пока нет

- 7.11.11 Lauenstein - Motion To Consolidate - 1290 Alberton CirleДокумент12 страниц7.11.11 Lauenstein - Motion To Consolidate - 1290 Alberton CirleStacie Power100% (2)

- Defendant's Trial BriefДокумент15 страницDefendant's Trial BriefChariseB2012100% (2)

- Dept. - 1 - at - 8:30 A.M. Dept. - at - A.m.: (Space Below For File Stamp Only)Документ27 страницDept. - 1 - at - 8:30 A.M. Dept. - at - A.m.: (Space Below For File Stamp Only)Valerie Lopez100% (1)

- Requesting Judicial Notice in CaliforniaДокумент3 страницыRequesting Judicial Notice in CaliforniaStan Burman100% (4)

- HBO Anti Slapp Motion To StrikeДокумент33 страницыHBO Anti Slapp Motion To StrikeSteve BucketОценок пока нет

- 2018-01-16 Defendant's Memorandum in Opposition To Plaintiffs Motion For Summary JudgmentДокумент6 страниц2018-01-16 Defendant's Memorandum in Opposition To Plaintiffs Motion For Summary Judgmentdbush1034Оценок пока нет

- Hwang V Savage - Reply To Opposition To DemurrerДокумент17 страницHwang V Savage - Reply To Opposition To DemurrerTHROnlineОценок пока нет

- Sample Motion To Compel Responses To Interrogatories in United States District CourtДокумент3 страницыSample Motion To Compel Responses To Interrogatories in United States District CourtStan Burman50% (2)

- Motion To Consolidate MG CG 2Документ21 страницаMotion To Consolidate MG CG 2caljics100% (1)

- Sample Motion For OSC For Contempt For Violations of The Discharge InjunctionДокумент3 страницыSample Motion For OSC For Contempt For Violations of The Discharge InjunctionStan Burman67% (3)

- PEREMPTORY CHALLENGE of Plaintiff Mel Gillespie To Disqualify & Recuse Judge VortmanДокумент2 страницыPEREMPTORY CHALLENGE of Plaintiff Mel Gillespie To Disqualify & Recuse Judge VortmancaljicsОценок пока нет

- Motion To Dismiss An Adversary Complaint For FraudДокумент3 страницыMotion To Dismiss An Adversary Complaint For FraudStan Burman100% (1)

- COMPLAINT Victor JohnsonДокумент38 страницCOMPLAINT Victor JohnsonBernie KimmerleОценок пока нет

- Motion For Judgment On Pleadings Delarosa V BoironДокумент28 страницMotion For Judgment On Pleadings Delarosa V BoironLara PearsonОценок пока нет

- Ex Parte DeclarationДокумент11 страницEx Parte DeclarationLEWISОценок пока нет

- SUP CT Emergency Motion For StayДокумент58 страницSUP CT Emergency Motion For StayBarry EskanosОценок пока нет

- Demand For Jury TrialДокумент2 страницыDemand For Jury TrialtmccandОценок пока нет

- Remove The Judge From Your Case: Peremptory Challenge of A JudgeДокумент11 страницRemove The Judge From Your Case: Peremptory Challenge of A JudgeMike RademakerОценок пока нет

- FAC - FinalДокумент13 страницFAC - FinalBrian StuartОценок пока нет

- I Original Verified Complaint: (Space Below For File Stamp Only)Документ57 страницI Original Verified Complaint: (Space Below For File Stamp Only)Valerie Lopez100% (1)

- Opposition To Defendants Motion For Attorneys FeesДокумент11 страницOpposition To Defendants Motion For Attorneys FeesGreg100% (2)

- 2015 12 04 Supersedeas FiledДокумент275 страниц2015 12 04 Supersedeas FiledCalifornia Judicial Branch News Service - Investigative Reporting Source Material & Story Ideas100% (1)

- DRAFT Opening BriefДокумент17 страницDRAFT Opening Brieftmccand100% (1)

- Opinion Dismissing Kelley Lynch Appeal From Order Denying Her Second Motion To Vacate Leonard Cohen's $14M Default JudgmentДокумент29 страницOpinion Dismissing Kelley Lynch Appeal From Order Denying Her Second Motion To Vacate Leonard Cohen's $14M Default JudgmentAnonymous 7EngESDPvM100% (1)

- Pro Se Handbook June 2012Документ76 страницPro Se Handbook June 2012Diane SternОценок пока нет

- Motion To Vacate UdДокумент4 страницыMotion To Vacate Udprosper4less822071% (7)

- CA - Class - BANK OF AMERICA CORPORATION PDFДокумент117 страницCA - Class - BANK OF AMERICA CORPORATION PDFprosper4less8220Оценок пока нет

- California Public Records Act PDFДокумент84 страницыCalifornia Public Records Act PDFprosper4less8220Оценок пока нет

- Response To OscДокумент6 страницResponse To Oscprosper4less8220Оценок пока нет

- Memo Rickey StandingДокумент14 страницMemo Rickey Standingprosper4less8220Оценок пока нет

- (Order) - Bias v. Wells FargoДокумент13 страниц(Order) - Bias v. Wells Fargoprosper4less8220Оценок пока нет

- US vs. Bank of America Case 1:12-Cv-00361-RMCДокумент99 страницUS vs. Bank of America Case 1:12-Cv-00361-RMCcagumshoeОценок пока нет

- Memorandum (Who Has The Right To Foreclose ?)Документ16 страницMemorandum (Who Has The Right To Foreclose ?)prosper4less8220Оценок пока нет

- Lockett V B of AДокумент13 страницLockett V B of Aprosper4less8220Оценок пока нет

- Carney V Bank of America / CALIFORNIAДокумент51 страницаCarney V Bank of America / CALIFORNIAprosper4less8220Оценок пока нет

- Pacific Concrete Federal Credit Union V KauanoeДокумент22 страницыPacific Concrete Federal Credit Union V Kauanoeprosper4less8220Оценок пока нет

- ("Washington Mutual") BARRIONUEVO - ORDER / CALIFORNIA VICTORYДокумент18 страниц("Washington Mutual") BARRIONUEVO - ORDER / CALIFORNIA VICTORYprosper4less8220Оценок пока нет

- California Homeowner Wins An Appeal Skov V Us BankДокумент11 страницCalifornia Homeowner Wins An Appeal Skov V Us Bankprosper4less8220Оценок пока нет

- Filed 6/8/12 Partial Pub. Order 7/3/12 (See End of Opn.)Документ19 страницFiled 6/8/12 Partial Pub. Order 7/3/12 (See End of Opn.)Foreclosure FraudОценок пока нет

- Petra Martinez V America's 09-Cv-5630-WhaДокумент8 страницPetra Martinez V America's 09-Cv-5630-Whaprosper4less8220Оценок пока нет

- CARLOS AGUIRRE - Quiet Title ActionДокумент33 страницыCARLOS AGUIRRE - Quiet Title Actionprosper4less822075% (4)

- Pacific Concrete Federal Credit Union V KauanoeДокумент22 страницыPacific Concrete Federal Credit Union V Kauanoeprosper4less8220Оценок пока нет

- Standard Rental Agreement - (Rental - With Performance Fee)Документ6 страницStandard Rental Agreement - (Rental - With Performance Fee)prosper4less8220Оценок пока нет

- Haines V KearnerДокумент2 страницыHaines V Kearnerprosper4less8220Оценок пока нет

- Fdcpa Wilson V Draper Gold Berg For Closing Agent Like Ndex West LLC Are Liable For Wrongful ForeclosureДокумент14 страницFdcpa Wilson V Draper Gold Berg For Closing Agent Like Ndex West LLC Are Liable For Wrongful Foreclosureprosper4less8220Оценок пока нет

- Mortgage Electronic Registration Systems, Inc., Appellant, V. Lisa Marie Chong, Lenard e SchwartzerДокумент6 страницMortgage Electronic Registration Systems, Inc., Appellant, V. Lisa Marie Chong, Lenard e SchwartzerForeclosure FraudОценок пока нет

- Mortgage Electronic Registration Systems, Inc., Appellant, V. Lisa Marie Chong, Lenard e SchwartzerДокумент6 страницMortgage Electronic Registration Systems, Inc., Appellant, V. Lisa Marie Chong, Lenard e SchwartzerForeclosure FraudОценок пока нет

- Carlos Aguirre - United Recovery Systems, Lp. Sent 09-09-2010Документ5 страницCarlos Aguirre - United Recovery Systems, Lp. Sent 09-09-2010prosper4less8220Оценок пока нет

- San Beda College of Law: Entralized AR PerationsДокумент3 страницыSan Beda College of Law: Entralized AR Perationschef justiceОценок пока нет

- Waqf Registration Form 1Документ2 страницыWaqf Registration Form 1SalamОценок пока нет

- Customs Seizure of Ships UpheldДокумент2 страницыCustoms Seizure of Ships UpheldFgmtОценок пока нет

- TortДокумент11 страницTortHarshVardhanОценок пока нет

- GR 158896 Siayngco Vs Siayngco PIДокумент1 страницаGR 158896 Siayngco Vs Siayngco PIMichael JonesОценок пока нет

- Basic Types of Legal Documents: - Deeds, Wills, Mortgages, EtcДокумент9 страницBasic Types of Legal Documents: - Deeds, Wills, Mortgages, EtcvenkatОценок пока нет

- Discuss The Different Modes of Filing Patent in Foreign CountriesДокумент7 страницDiscuss The Different Modes of Filing Patent in Foreign Countrieshariom bajpaiОценок пока нет

- JG Summit Holdings Vs CA September 24, 2003 PDFДокумент2 страницыJG Summit Holdings Vs CA September 24, 2003 PDFErvin Franz Mayor CuevillasОценок пока нет

- Prime Ministers of Jamaica profilesДокумент10 страницPrime Ministers of Jamaica profilesalessseОценок пока нет

- Sec 3 CompilationДокумент6 страницSec 3 CompilationMatthew WittОценок пока нет

- Territorial Jurisdiction in Online Defamation CasesДокумент6 страницTerritorial Jurisdiction in Online Defamation CasesJebin JamesОценок пока нет

- CAF 101 For Civilians, Aug 16Документ160 страницCAF 101 For Civilians, Aug 16MarlenОценок пока нет

- SpecPro - LEE vs. CA GR118387Документ3 страницыSpecPro - LEE vs. CA GR118387Niño CarbonillaОценок пока нет

- P (TC 15B)Документ29 страницP (TC 15B)suruchi0901Оценок пока нет

- List of Taxpayers For Deletion in The List of Top Withholding Agents (Twas)Документ217 страницList of Taxpayers For Deletion in The List of Top Withholding Agents (Twas)Hanabishi RekkaОценок пока нет

- Ladislaus Mutashubirwa Vs Edna Josephat Ruganisa (PC Civil Appeal 144 of 2020) 2021 TZHC 3779 (28 May 2021)Документ16 страницLadislaus Mutashubirwa Vs Edna Josephat Ruganisa (PC Civil Appeal 144 of 2020) 2021 TZHC 3779 (28 May 2021)DENIS NGUVUОценок пока нет

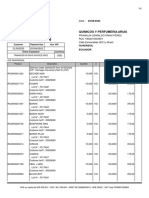

- Factura ComercialДокумент6 страницFactura ComercialKaren MezaОценок пока нет

- CAP 417 SurveyorsboardДокумент13 страницCAP 417 SurveyorsboardpschilОценок пока нет

- Torts 29 - St. Mary's Academy v. CarpitanosДокумент2 страницыTorts 29 - St. Mary's Academy v. CarpitanosjosephОценок пока нет

- SSGSPG Gathering Data ToolДокумент20 страницSSGSPG Gathering Data ToolRobert Kier Tanquerido TomaroОценок пока нет

- 23 Motion To Compel Determination 246 Decatur Street Eleanor PhillipsДокумент7 страниц23 Motion To Compel Determination 246 Decatur Street Eleanor PhillipsTaylorbey American NationalОценок пока нет

- Corporate Governance Evolution and TheoriesДокумент35 страницCorporate Governance Evolution and TheoriesPRAKHAR GUPTA100% (1)

- Leave & License AgreementДокумент2 страницыLeave & License AgreementThakur Sarthak SinghОценок пока нет

- Application FOR Customs Broker License Exam: U.S. Customs and Border ProtectionДокумент1 страницаApplication FOR Customs Broker License Exam: U.S. Customs and Border ProtectionIsha SharmaОценок пока нет

- Red Tape Report: Behind The Scenes of The Section 8 Housing ProgramДокумент7 страницRed Tape Report: Behind The Scenes of The Section 8 Housing ProgramBill de BlasioОценок пока нет

- IEI Is Statutory-Court JudgmentДокумент8 страницIEI Is Statutory-Court JudgmentErRajivAmieОценок пока нет

- Republic Act No. 11463Документ4 страницыRepublic Act No. 11463Arnan PanaliganОценок пока нет

- United States v. Herman Ray Berry, 362 F.2d 756, 2d Cir. (1966)Документ4 страницыUnited States v. Herman Ray Berry, 362 F.2d 756, 2d Cir. (1966)Scribd Government DocsОценок пока нет

- 9 Lopez vs. RamosДокумент2 страницы9 Lopez vs. Ramosmei atienzaОценок пока нет

- The Code of Civil Procedure, 1908 Non-Joinder and Misjoinder Parties To SuitsДокумент13 страницThe Code of Civil Procedure, 1908 Non-Joinder and Misjoinder Parties To Suitsnirav doshiОценок пока нет