Вам также может понравиться

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5795)

- Third Point Q3 2012 Investor Letter TPOIДокумент11 страницThird Point Q3 2012 Investor Letter TPOIVALUEWALK LLCОценок пока нет

- 8th Annual New York: Value Investing CongressДокумент53 страницы8th Annual New York: Value Investing CongressVALUEWALK LLCОценок пока нет

- 8th Annual New York: Value Investing CongressДокумент51 страница8th Annual New York: Value Investing CongressVALUEWALK LLCОценок пока нет

- Ubben ValueInvestingCongress 100212Документ27 страницUbben ValueInvestingCongress 100212VALUEWALK LLC100% (1)

- 8th Annual New York: Value Investing CongressДокумент46 страниц8th Annual New York: Value Investing CongressVALUEWALK LLCОценок пока нет

- Ghazi ValueInvestingCongress 100112Документ70 страницGhazi ValueInvestingCongress 100112VALUEWALK LLC100% (1)

- SHLDДокумент18 страницSHLDduwe7809100% (1)

- 2012 Third Point Q2 Investor Letter TPOIДокумент7 страниц2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- 2012 Third Point Q2 Investor Letter TPOIДокумент7 страниц2012 Third Point Q2 Investor Letter TPOIVALUEWALK LLC100% (1)

- Rockstone Research URS1 EnglishДокумент32 страницыRockstone Research URS1 EnglishVALUEWALK LLC100% (1)

- Why We'Re Long J.C. Penney-T2 PartnersДокумент18 страницWhy We'Re Long J.C. Penney-T2 PartnersVALUEWALK LLCОценок пока нет

- Value Investing Congress Presentation-Tilson-10!1!12Документ93 страницыValue Investing Congress Presentation-Tilson-10!1!12VALUEWALK LLCОценок пока нет

- Green Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersДокумент8 страницGreen Mountain Coffee Roasters' Q2 and Q3 2011 Net Sales Figures Look Odd and Why It MattersmistervigilanteОценок пока нет

- HP PresentationДокумент69 страницHP Presentationssc320Оценок пока нет

- Greenlight Q2 Letter To InvestorsДокумент5 страницGreenlight Q2 Letter To InvestorsVALUEWALK LLCОценок пока нет

- VALUExVail 2012 James ChanosДокумент30 страницVALUExVail 2012 James ChanosVALUEWALK LLCОценок пока нет

- Fairholme: Ignore The CrowdДокумент13 страницFairholme: Ignore The CrowdVALUEWALK LLCОценок пока нет

- T2 Accredited Fund Letter To Investors June 12Документ10 страницT2 Accredited Fund Letter To Investors June 12VALUEWALK LLCОценок пока нет

- Fairholme: Ignore The CrowdДокумент13 страницFairholme: Ignore The CrowdVALUEWALK LLCОценок пока нет

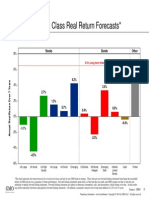

- GMO 7 Year Asset Forecast - Jan 2014Документ1 страницаGMO 7 Year Asset Forecast - Jan 2014CanadianValueОценок пока нет

- Pershing Square Q1 12 Investor LetterДокумент14 страницPershing Square Q1 12 Investor LetterVALUEWALK LLCОценок пока нет

- Mauboussinonstrategy - Sharerepurchasefromallangles June 2012Документ15 страницMauboussinonstrategy - Sharerepurchasefromallangles June 2012zeebugОценок пока нет

- ASFL - Quarterly Accounts - September 30, 2011Документ17 страницASFL - Quarterly Accounts - September 30, 2011VALUEWALK LLCОценок пока нет

- To Longleaf Shareholders: Cumulative Returns at December 31, 2011Документ6 страницTo Longleaf Shareholders: Cumulative Returns at December 31, 2011VALUEWALK LLCОценок пока нет

- Annual Report: March 31, 2011Документ23 страницыAnnual Report: March 31, 2011VALUEWALK LLCОценок пока нет

- Bruce Berkowitz - Fairholme 2011 Stat Sheet (Morning Star)Документ2 страницыBruce Berkowitz - Fairholme 2011 Stat Sheet (Morning Star)Luochang YuОценок пока нет

- Nokia Results2011Q4eДокумент60 страницNokia Results2011Q4ejunaid112Оценок пока нет

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- Nature of Consolidated StatementsДокумент8 страницNature of Consolidated StatementsRoldan Arca PagaposОценок пока нет

- Chapter 3 Securities MarketДокумент50 страницChapter 3 Securities Marketsharktale2828100% (1)

- FM Revision - MaterialДокумент217 страницFM Revision - MaterialSri HariniОценок пока нет

- Chapter 6 Homework - Motaman AlquraishДокумент9 страницChapter 6 Homework - Motaman AlquraishMaddah HussainОценок пока нет

- Technical Analysis of Indian Stock MarketДокумент21 страницаTechnical Analysis of Indian Stock MarketDeepak TulsaniОценок пока нет

- U-2 - Corporate Level Strategy - Creating Value Through DiversificationДокумент18 страницU-2 - Corporate Level Strategy - Creating Value Through DiversificationGenieОценок пока нет

- Tutorial 3 QuestionsДокумент6 страницTutorial 3 QuestionshrfjbjrfrfОценок пока нет

- 2015 UBS IB Challenge Corporate Finance OverviewДокумент23 страницы2015 UBS IB Challenge Corporate Finance Overviewkevin100% (1)

- Exercises For Chapter 23 EFA2Документ13 страницExercises For Chapter 23 EFA2tuananh leОценок пока нет

- FX Forward ContractsДокумент2 страницыFX Forward ContractsQuant_GeekОценок пока нет

- Daily Notes: Wilcon Depot, Inc. (pse:WLCON)Документ2 страницыDaily Notes: Wilcon Depot, Inc. (pse:WLCON)Anonymous xcFcOgMiОценок пока нет

- Chapter 4Документ20 страницChapter 4Moon TrangОценок пока нет

- Venture Capital Concept AnalysisДокумент106 страницVenture Capital Concept Analysisdhs1234Оценок пока нет

- Donna Jamison Was Recently Hired As A Financial Analyst byДокумент3 страницыDonna Jamison Was Recently Hired As A Financial Analyst byAmit PandeyОценок пока нет

- Certified Valuation Analyst - CVA in Egypt by Developers For Training and ConsultancyДокумент2 страницыCertified Valuation Analyst - CVA in Egypt by Developers For Training and ConsultancydevelopersegyptОценок пока нет

- Stock BrokerДокумент10 страницStock BrokershubhdeepОценок пока нет

- RWJ 08Документ38 страницRWJ 08Kunal PuriОценок пока нет

- Time Value of MoneyДокумент60 страницTime Value of MoneyAtta MohammadОценок пока нет

- Sample Investment ContractДокумент3 страницыSample Investment ContractAnn SC100% (10)

- The Forex Scalping Guide: How To Scalp ForexДокумент27 страницThe Forex Scalping Guide: How To Scalp ForexSusanto Yang100% (4)

- HDFC Product DetailsДокумент19 страницHDFC Product DetailsPrincess BinsonОценок пока нет

- 03.GCG ASIA Multimillion Dollar Marketing Plan - V3 PDFДокумент19 страниц03.GCG ASIA Multimillion Dollar Marketing Plan - V3 PDFhamidanirs4606Оценок пока нет

- Financial Management of HospitalsДокумент13 страницFinancial Management of HospitalsaakarОценок пока нет

- Debt Market in India - Key Issues & Policy RecommendationsДокумент17 страницDebt Market in India - Key Issues & Policy Recommendationsreep_12Оценок пока нет

- Activity No. 1-1 Transaction Effects On The Basic Accounting ModelДокумент1 страницаActivity No. 1-1 Transaction Effects On The Basic Accounting ModelYumie Valdespiñosa100% (1)

- Question On SFMДокумент4 страницыQuestion On SFMjazzy123Оценок пока нет

- CGD Securities - Morning Briefing - 02oct2013 PDFДокумент7 страницCGD Securities - Morning Briefing - 02oct2013 PDFIsaac MatheusОценок пока нет

- Literature Review On Financial InstrumentsДокумент9 страницLiterature Review On Financial Instrumentshnpawevkg100% (1)

- Bouwinvest Global Real Estate MarketsДокумент36 страницBouwinvest Global Real Estate MarketsSemon AungОценок пока нет

- Chapter 15Документ25 страницChapter 15Mohamed MedОценок пока нет