Вам также может понравиться

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeОт EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeРейтинг: 4 из 5 звезд4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreОт EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreРейтинг: 4 из 5 звезд4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItОт EverandNever Split the Difference: Negotiating As If Your Life Depended On ItРейтинг: 4.5 из 5 звезд4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceОт EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceРейтинг: 4 из 5 звезд4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersОт EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersРейтинг: 4.5 из 5 звезд4.5/5 (344)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureОт EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureРейтинг: 4.5 из 5 звезд4.5/5 (474)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)От EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Рейтинг: 4.5 из 5 звезд4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerОт EverandThe Emperor of All Maladies: A Biography of CancerРейтинг: 4.5 из 5 звезд4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingОт EverandThe Little Book of Hygge: Danish Secrets to Happy LivingРейтинг: 3.5 из 5 звезд3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyОт EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyРейтинг: 3.5 из 5 звезд3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)От EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Рейтинг: 4 из 5 звезд4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaОт EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaРейтинг: 4.5 из 5 звезд4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryОт EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryРейтинг: 3.5 из 5 звезд3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnОт EverandTeam of Rivals: The Political Genius of Abraham LincolnРейтинг: 4.5 из 5 звезд4.5/5 (234)

- Transactions 1Документ9 страницTransactions 1Mikaela Jean0% (1)

- The Unwinding: An Inner History of the New AmericaОт EverandThe Unwinding: An Inner History of the New AmericaРейтинг: 4 из 5 звезд4/5 (45)

- Homework Chapter 4Документ17 страницHomework Chapter 4Trung Kiên Nguyễn100% (1)

- Insurance Industry Balance ScorecardДокумент6 страницInsurance Industry Balance Scorecardish june100% (1)

- Answer: Cost Flow Equation: BB + TI TO + EB Computer Chips: $600,000 + $1,600,000 $1,800,000 + EBДокумент8 страницAnswer: Cost Flow Equation: BB + TI TO + EB Computer Chips: $600,000 + $1,600,000 $1,800,000 + EBkmarisseeОценок пока нет

- Yap - ACP312 - ULOb - Let's CheckДокумент4 страницыYap - ACP312 - ULOb - Let's CheckJunzen Ralph YapОценок пока нет

- Income Statement Vertical Analysis TemplateДокумент2 страницыIncome Statement Vertical Analysis TemplateSope DalleyОценок пока нет

- Legend - Docx 1Документ101 страницаLegend - Docx 1Juberlina CerbitoОценок пока нет

- Allama Iqbal Open University, Islamabad (Department of Business Administration)Документ9 страницAllama Iqbal Open University, Islamabad (Department of Business Administration)Muhammad AbdullahОценок пока нет

- Degree of Financial Leverage Formula Excel TemplateДокумент4 страницыDegree of Financial Leverage Formula Excel TemplateSyed Mursaleen ShahОценок пока нет

- FAR 2922 Investments in Equity Instruments PDFДокумент5 страницFAR 2922 Investments in Equity Instruments PDFEki OmallaoОценок пока нет

- OHADA Financial AnalysisДокумент5 страницOHADA Financial AnalysisCheikh Omar TouréОценок пока нет

- Impetus - Sales Team IncentiveДокумент2 страницыImpetus - Sales Team IncentivePankaj KumarОценок пока нет

- Research Insight - 3Документ6 страницResearch Insight - 3Srinivas NandikantiОценок пока нет

- Unit - 2 - Financial Statement and RatioДокумент37 страницUnit - 2 - Financial Statement and Ratiodangthanhhd7967% (6)

- Auditing Problems MC Quizzer 02Документ15 страницAuditing Problems MC Quizzer 02anndyОценок пока нет

- Tencent CaseДокумент8 страницTencent CaseChiro Sun0% (1)

- Profit MaximisationДокумент7 страницProfit MaximisationAmir SadeeqОценок пока нет

- Income Capital ItemsДокумент2 страницыIncome Capital ItemsDeepti KukretiОценок пока нет

- CVP - Quiz 1Документ7 страницCVP - Quiz 1Jane ValenciaОценок пока нет

- Nepali Talim Youtube Channel: Calculation of Salary Tax For Social Security Listed OrgДокумент20 страницNepali Talim Youtube Channel: Calculation of Salary Tax For Social Security Listed OrgsamОценок пока нет

- DownloadДокумент1 страницаDownloadJitaram SamalОценок пока нет

- Management Accounting: Cost-Volume-Profit AnalysisДокумент74 страницыManagement Accounting: Cost-Volume-Profit AnalysisGrace FerlindaОценок пока нет

- 0033 POWR Laporan Keuangan FY19Документ90 страниц0033 POWR Laporan Keuangan FY19Ahmad KharisОценок пока нет

- NISM Training - Mutual FundsДокумент155 страницNISM Training - Mutual Fundsniks dОценок пока нет

- Solved Curtis Is 50 Years Old and Has An Individual RetirementДокумент1 страницаSolved Curtis Is 50 Years Old and Has An Individual RetirementAnbu jaromiaОценок пока нет

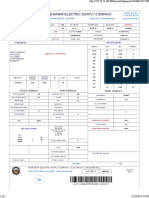

- Pesco Online BilllДокумент2 страницыPesco Online BilllZafar Khan NiaziОценок пока нет

- Accounts Ans Jan 2021Документ25 страницAccounts Ans Jan 2021Hemant AherОценок пока нет

- DT 2 New Question PaperДокумент11 страницDT 2 New Question Paperneha manglaniОценок пока нет

- Pak Country en Excel v2Документ522 страницыPak Country en Excel v2tanveerameenОценок пока нет

- 2019 Paper AccsДокумент3 страницы2019 Paper AccsDhrisha GadaОценок пока нет