Вам также может понравиться

- J.K. Lasser's Small Business Taxes 2012: Your Complete Guide to a Better Bottom LineОт EverandJ.K. Lasser's Small Business Taxes 2012: Your Complete Guide to a Better Bottom LineОценок пока нет

- Quiz 8 - CH 15 & 16 - ACC563Документ13 страницQuiz 8 - CH 15 & 16 - ACC563scokni1973_130667106Оценок пока нет

- Feedback: The Correct Answer Is: Has A Higher Market Price Per Dollar of Earnings Than Does One Share of Turner'sДокумент20 страницFeedback: The Correct Answer Is: Has A Higher Market Price Per Dollar of Earnings Than Does One Share of Turner'sDương Hà LinhОценок пока нет

- Financial-Managementuprgdall-In 3 PDFДокумент67 страницFinancial-Managementuprgdall-In 3 PDFCasey Collera Mediana100% (1)

- UGRD-TAX6148-2323T Income Taxation Midterm ExamДокумент28 страницUGRD-TAX6148-2323T Income Taxation Midterm ExamcybilmercadoОценок пока нет

- Advanced AccountingДокумент15 страницAdvanced AccountingDawna Lee BerryОценок пока нет

- Acct Final ExamДокумент9 страницAcct Final Examghenni199Оценок пока нет

- UGRD-TAX6148-2323T Income Taxation Midterm Quiz 1Документ8 страницUGRD-TAX6148-2323T Income Taxation Midterm Quiz 1cybilmercadoОценок пока нет

- 3rd Examination FabmДокумент19 страниц3rd Examination FabmZein gomez50% (8)

- Quiz 11Документ9 страницQuiz 11shivnilОценок пока нет

- Conceptual Midterm QuizДокумент21 страницаConceptual Midterm Quizmalou reyesОценок пока нет

- Mema FabmДокумент29 страницMema FabmJohuana Lhesty Sabordo Jabas100% (1)

- Quiz 1 Graded 86.6Документ11 страницQuiz 1 Graded 86.6cochran123Оценок пока нет

- FinMa PDFДокумент86 страницFinMa PDFJolex Acid0% (1)

- Exam Chap 13Документ59 страницExam Chap 13oscarv89100% (2)

- Chap3 QuizДокумент10 страницChap3 Quizharrisfb100% (2)

- Mancon Quiz 6Документ45 страницMancon Quiz 6Quendrick SurbanОценок пока нет

- Acc401 QuizДокумент13 страницAcc401 Quizrachel_p_6Оценок пока нет

- Mancon Quiz 4Документ32 страницыMancon Quiz 4Quendrick SurbanОценок пока нет

- Mas Week 6 Balanced ScorecardДокумент5 страницMas Week 6 Balanced ScorecardHermz Comz0% (1)

- Post Quiz 8-AF101Документ12 страницPost Quiz 8-AF101Moira Emma N. EdmondОценок пока нет

- Conceptual Framework VertualДокумент19 страницConceptual Framework VertualCherwin bentulan0% (2)

- Shareholder's Equity Practice Set (Theories)Документ42 страницыShareholder's Equity Practice Set (Theories)ME ValleserОценок пока нет

- Quiz1 2, Midterm (AST)Документ41 страницаQuiz1 2, Midterm (AST)Kyla Mae MurphyОценок пока нет

- Kiểm tra LMS - lần 2Документ17 страницKiểm tra LMS - lần 2Kotoru HanoelОценок пока нет

- Fs Analysis Pre TestДокумент13 страницFs Analysis Pre TestDRIXLER RIVERAОценок пока нет

- Adv Acct Quiz 3 Chapter 4Документ5 страницAdv Acct Quiz 3 Chapter 4Nikki Harris100% (1)

- Financial Management Source #6Документ12 страницFinancial Management Source #6EDPSENPAI100% (1)

- Accounting For Business Combinations (PrelimQ2)Документ11 страницAccounting For Business Combinations (PrelimQ2)nomoredreamОценок пока нет

- Business Math Summative AssessmentДокумент5 страницBusiness Math Summative Assessmentyow BroОценок пока нет

- Multiple-Choice MlearningДокумент29 страницMultiple-Choice MlearningBích TiênОценок пока нет

- Edep Na Reh - 126Документ9 страницEdep Na Reh - 126Mark Jayson FaustinoОценок пока нет

- Business Laws and Reg 2ND Term PreДокумент10 страницBusiness Laws and Reg 2ND Term PreCasey Collera MedianaОценок пока нет

- Exam 3 AcctsДокумент3 страницыExam 3 Acctssamaresh chhotrayОценок пока нет

- FIN571 FREE Final Exam Study GuideДокумент17 страницFIN571 FREE Final Exam Study GuideRogue Phoenix100% (2)

- Maulana Ikhsan Tarigan (Financial Statement Analysis) 197007091Документ11 страницMaulana Ikhsan Tarigan (Financial Statement Analysis) 197007091Maulana IkhsanОценок пока нет

- CourseHeroExam1 1Документ8 страницCourseHeroExam1 1David LewisОценок пока нет

- Question Text: Started On State Completed On Time Taken GradeДокумент6 страницQuestion Text: Started On State Completed On Time Taken GradeYefinia OpianaОценок пока нет

- AAT Skillcheck ResultsДокумент9 страницAAT Skillcheck ResultsCiprian IchimОценок пока нет

- Partnership and Corporation ReviewerДокумент7 страницPartnership and Corporation ReviewerEmanuel CenidozaОценок пока нет

- Stratergic FinanceДокумент105 страницStratergic Financethakur_0000Оценок пока нет

- ACC 561 Week 1 Practice QuizДокумент12 страницACC 561 Week 1 Practice QuizWrkingStudentОценок пока нет

- SCDL Finance Management Q1docxДокумент7 страницSCDL Finance Management Q1docxSandeepNayak100% (1)

- Fed Income PretestДокумент10 страницFed Income PretestAndrea Mcnair-WestОценок пока нет

- Intermediate 3 Blend. (AutoRecovered)Документ72 страницыIntermediate 3 Blend. (AutoRecovered)Cherwin bentulanОценок пока нет

- Financial Ratios Drill TheoriesДокумент9 страницFinancial Ratios Drill TheoriesDRIXLER RIVERAОценок пока нет

- AFA QuizДокумент15 страницAFA QuizNoelia Mc DonaldОценок пока нет

- Financial Management TEAM NETFLIX Midterm Exam TheoryДокумент4 страницыFinancial Management TEAM NETFLIX Midterm Exam TheorykvelezОценок пока нет

- Finman QuizДокумент65 страницFinman QuizChrista LenzОценок пока нет

- PDFДокумент35 страницPDFFrancheska NadurataОценок пока нет

- (AMALEAKS - BLOGSPOT.COM) FABM 2nd SemДокумент68 страниц(AMALEAKS - BLOGSPOT.COM) FABM 2nd SemJurome Luise Fernando50% (4)

- Document 3 PDFДокумент50 страницDocument 3 PDFChristine Jane AbangОценок пока нет

- CfatДокумент12 страницCfatSahil MakkarОценок пока нет

- Quiz 3 Attempt ReviewДокумент1 страницаQuiz 3 Attempt Reviewekoh onosedebaОценок пока нет

- Under Variable Costing:: Question 1Документ35 страницUnder Variable Costing:: Question 1Iris FenelleОценок пока нет

- ACT400 - Mastery ExerciseДокумент125 страницACT400 - Mastery ExerciseKrystal FabianОценок пока нет

- Make Money With Dividends Investing, With Less Risk And Higher ReturnsОт EverandMake Money With Dividends Investing, With Less Risk And Higher ReturnsОценок пока нет

- Accounting and Finance Formulas: A Simple IntroductionОт EverandAccounting and Finance Formulas: A Simple IntroductionРейтинг: 4 из 5 звезд4/5 (8)

- Understanding Financial Statements (Review and Analysis of Straub's Book)От EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Рейтинг: 5 из 5 звезд5/5 (5)

- Aud Prob Compilation 1Документ31 страницаAud Prob Compilation 1Chammy TeyОценок пока нет

- Cost of CapitalДокумент15 страницCost of CapitalrosdicoОценок пока нет

- Chap 21 - Leasing (PSAK 73) - E12-12Документ27 страницChap 21 - Leasing (PSAK 73) - E12-12Happy MichaelОценок пока нет

- General Mathematics: Quarter 2 - Module 10: Market Indices For Stocks and BondsДокумент27 страницGeneral Mathematics: Quarter 2 - Module 10: Market Indices For Stocks and Bondsshadow girirjekОценок пока нет

- Chapter-7 Pracrice Exercise (Seatwork) Marato, Jedediah SamuelДокумент3 страницыChapter-7 Pracrice Exercise (Seatwork) Marato, Jedediah SamuelJedediah Samuel Marato0% (1)

- 12sm Accountancy Eng 2021 22Документ512 страниц12sm Accountancy Eng 2021 22Piyush ChhajerОценок пока нет

- 7 Fundamental-Analysis-of-the-Indian-Stock-MarketДокумент6 страниц7 Fundamental-Analysis-of-the-Indian-Stock-MarketSujith LalОценок пока нет

- BASURДокумент28 страницBASURVinayak n basurОценок пока нет

- Intermediate Accounting IFRS Edition: Kieso, Weygandt, WarfieldДокумент76 страницIntermediate Accounting IFRS Edition: Kieso, Weygandt, WarfieldĐức Huy100% (1)

- Intermediate Accounting 1A Chapter 10 - Investment in Debt Securities Problem 3Документ5 страницIntermediate Accounting 1A Chapter 10 - Investment in Debt Securities Problem 3Yuki BarracaОценок пока нет

- Module 1 - FAR 2Документ33 страницыModule 1 - FAR 2Catherine CaleroОценок пока нет

- Comparative International Auditing and Corporate Governance: ThirteenДокумент47 страницComparative International Auditing and Corporate Governance: ThirteenCatalina OrianiОценок пока нет

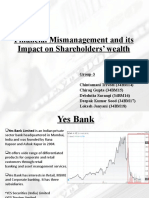

- Group3 - CFEV - Project Presentation - Fin-MismanagementДокумент11 страницGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodОценок пока нет

- Mergers and Acquisitions 2021Документ47 страницMergers and Acquisitions 2021Evelyne BiwottОценок пока нет

- Accountancy, Business and Management Summative Test (2 Quarter)Документ3 страницыAccountancy, Business and Management Summative Test (2 Quarter)Alvin Echano AsanzaОценок пока нет

- Calendar FY18 For Any CompanyДокумент1 страницаCalendar FY18 For Any CompanyburnoutcandleОценок пока нет

- 3303 Ex 1 Review Key 2013Документ4 страницы3303 Ex 1 Review Key 2013yangpukimiОценок пока нет

- Nike, Inc. - Cost of CapitalДокумент9 страницNike, Inc. - Cost of CapitalPutriОценок пока нет

- Sampa Video Case SolutionДокумент10 страницSampa Video Case SolutionrahulsinhadpsОценок пока нет

- Beximco Pharmaceuticals Limited Statement of Financial PositionДокумент55 страницBeximco Pharmaceuticals Limited Statement of Financial Positionrimon dasОценок пока нет

- 6.MAF 603 CH 10 - Mergers, Acquisitions and DivestituresДокумент45 страниц6.MAF 603 CH 10 - Mergers, Acquisitions and DivestituresSullivan LyaОценок пока нет

- FRM Mcq'sДокумент69 страницFRM Mcq'sAakash Kathuria0% (3)

- Defenses Against Hostile TakeoverДокумент51 страницаDefenses Against Hostile TakeoverHemanshu RoyОценок пока нет

- GROUP 7 Chapter 13Документ29 страницGROUP 7 Chapter 13Rhad Lester C. MaestradoОценок пока нет

- Finance Module 01 - Week 1Документ14 страницFinance Module 01 - Week 1Christian ZebuaОценок пока нет

- Apple Inc. (AAPL) Final PresentationДокумент16 страницApple Inc. (AAPL) Final PresentationShukran AlakbarovОценок пока нет

- 12353Документ6 страниц12353Maurice AgbayaniОценок пока нет

- Bains 7B BuyoutДокумент3 страницыBains 7B BuyoutwallstreetprepОценок пока нет

- Acct 2011 Anderson Pty LTD Is An Australian Diversified IndustrialДокумент2 страницыAcct 2011 Anderson Pty LTD Is An Australian Diversified IndustrialCharlotteОценок пока нет

- Kaef LK TW Ii 2022Документ208 страницKaef LK TW Ii 2022Nida Maulida HaviyaОценок пока нет